How Vidysea's Loan Assistance Works —End to End: From Your First Question to Your First EMI

An education loan for abroad is the largest financial commitment most Indian families make after a home purchase. At Rs. 40–80L for a two-year master's programme in the UK, Canada, or Australia, the interest rate, collateral structure, moratorium terms, and disbursement timing of a study abroad loan affect the family's finances for a decade. A 3% difference in interest rate on a Rs. 60L loan over 10 years is Rs. 10–12L — money that could fund 10 months of living costs abroad.

Team Vidysea

June 1, 2026

Most Indian families approach the student loan for abroad process by walking into the nearest bank branch or searching online for the best rate — without knowing which lender's eligibility criteria their specific profile meets, how to structure financial documents for the visa authority's requirement (not just the university's), or how to co-ordinate disbursement timing with the student visa application. These are the decisions where Vidysea's loan assistance adds value that cannot be obtained from a bank's loan page.

This guide explains exactly how Vidysea's international education loan assistance works — the complete 8-stage end-to-end process, a comparison of every major international student loan lender available to Indian students in 2026 (PSU banks, NBFCs, and international lenders), a decision matrix by borrower profile, and the real cost of choosing the wrong loan. If you need a quick student loan for a visa deadline in 4 weeks — that scenario is specifically addressed in Stage 4 and the decision matrix.

What Vidysea's loan assistance covers that a bank branch cannot

A bank branch advises on their own product only. Vidysea compares 8+ lenders across PSU banks (SBI, Bank of Baroda), NBFCs (HDFC Credila, Avanse, Auxilo, InCred), and international lenders (MPOWER, Prodigy Finance) simultaneously. We assess which lenders your profile qualifies for, recommend the best fit for your loan amount, collateral position, and timeline, and — critically — ensure your sanction letter is structured correctly for your specific visa authority's financial proof requirement, not just the general lender template.

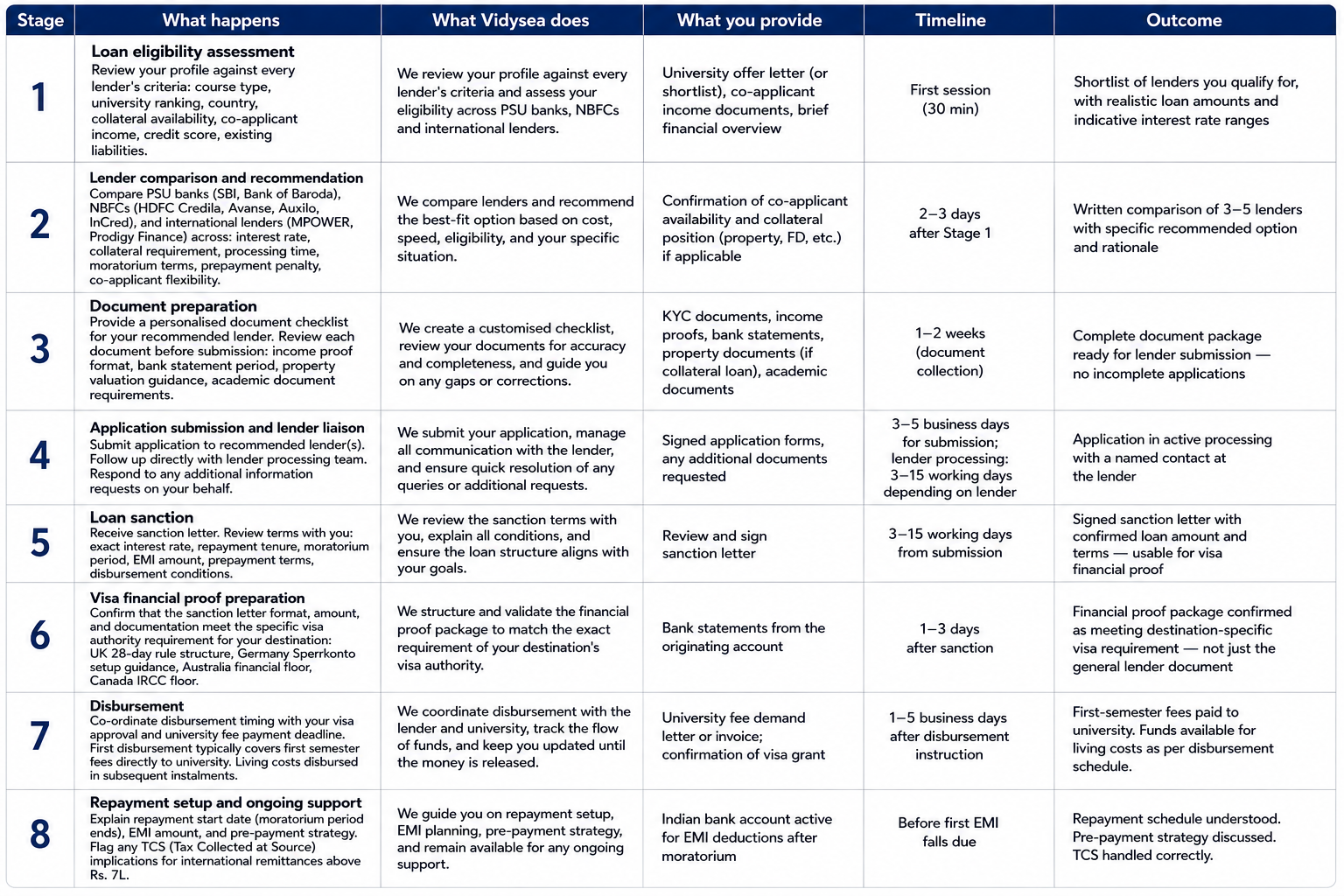

Vidysea's Loan Assistance — 8-Stage End-to-End Process

Here is exactly what Vidysea does at each stage of your study abroad student loan journey — what we do, what you provide, the timeline, and the specific outcome.

Stage 6 is where most families lose money without realising it

A loan sanction letter that does not meet the specific visa authority's financial proof requirement is the most avoidable loan-related visa delay in the process. The UK requires 28 consecutive days of financial proof — a sanction letter alone is not sufficient; it must be combined with correctly structured bank statements. Germany requires a Sperrkonto (blocked account with €11,904) — a loan sanction letter alone is not accepted by the German consulate. Australia requires funds above a specific floor with a documented source. Stage 6 of Vidysea's process specifically verifies that your loan documentation meets the visa requirement — not just the general lender standard.

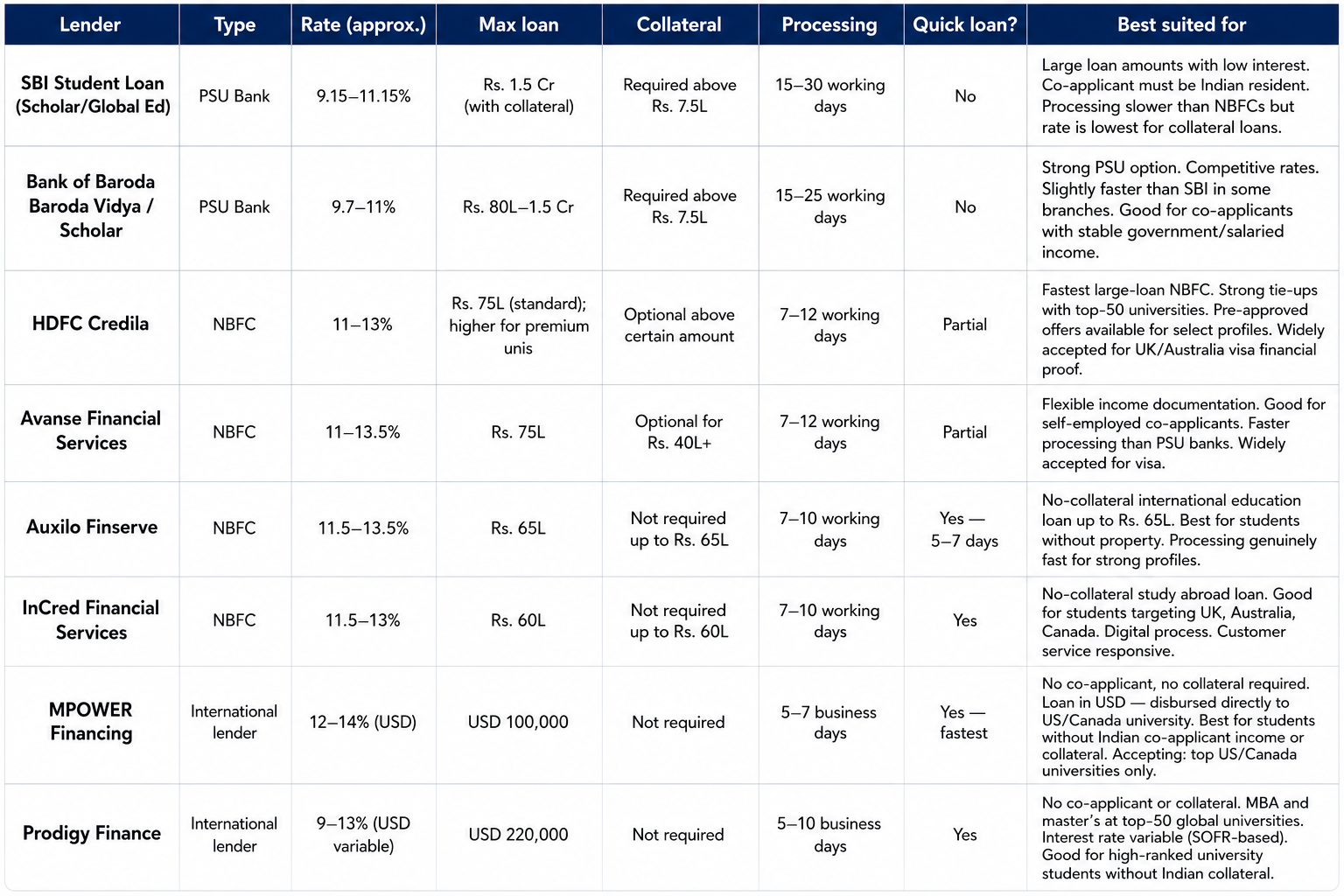

Education Loan for Abroad — Complete Lender Comparison 2026

This is the complete comparison of every major international education loan lender available to Indian students in 2026. Interest rates are indicative — actual rates depend on profile, collateral, and university. 'Quick student loan?' column answers whether the lender can process in under 10 working days for a strong profile:

Why the cheapest loan is not always the best loan

SBI's interest rate is the lowest available for collateral-backed study abroad loans (9.15–11.15%). But SBI's processing time is 15–30 working days — a timeline that does not work for students with visa appointments in 3 weeks. For a strong, documented profile where timeline is not critical, SBI is the right choice and the savings are substantial. For students who need a quick student loan — confirmed collateral or no-collateral up to Rs. 65L — NBFCs (Auxilo, InCred, HDFC Credila) are faster and the processing time difference justifies the rate premium. Vidysea's recommendation is always specific to your timeline, not a generic 'choose NBFC' or 'choose PSU bank.'

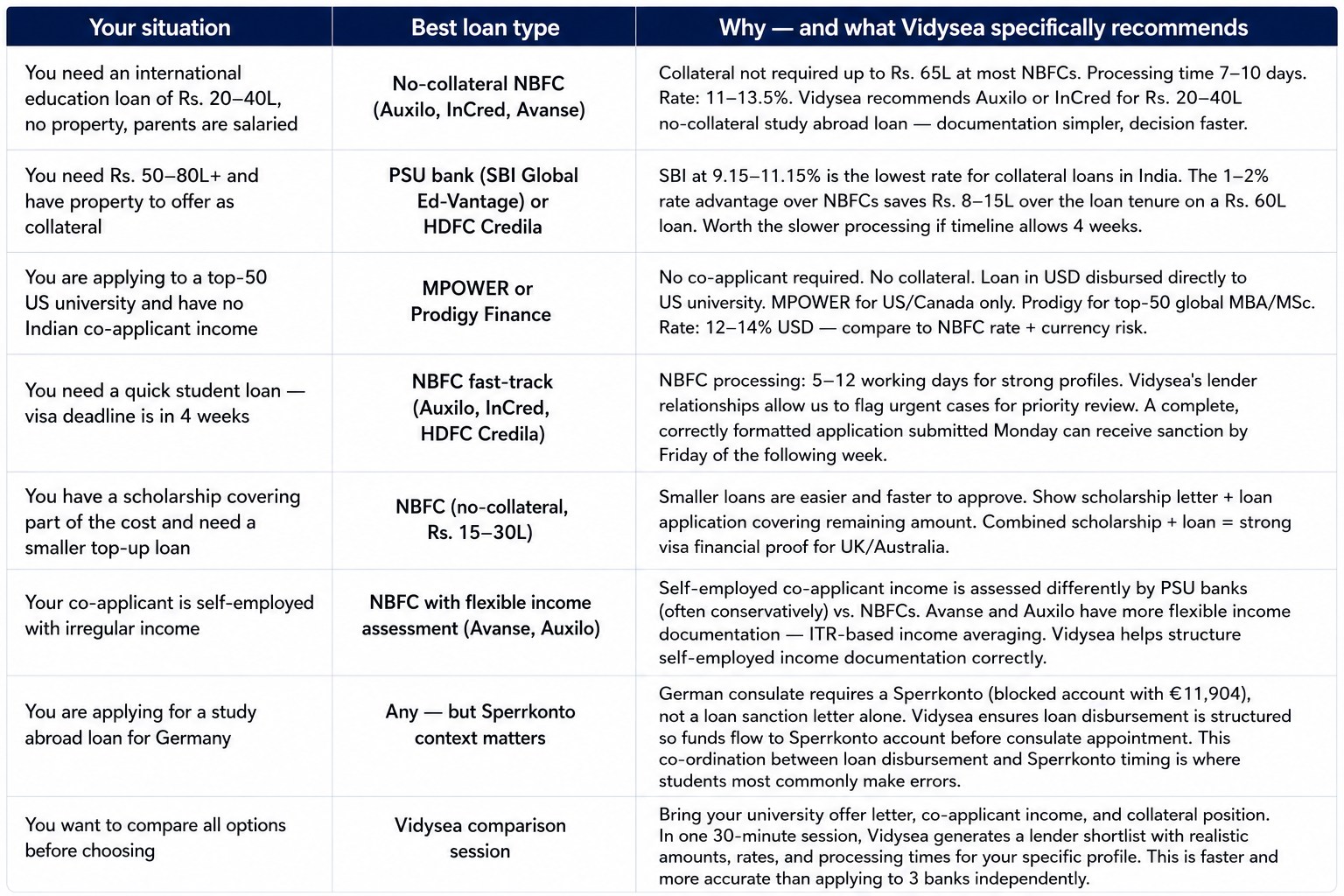

Which Loan for Your Profile? Decision Matrix

Use this matrix to identify the study abroad loan type and lender category that best fits your specific situation:

Never apply to multiple lenders simultaneously without a strategy

Applying to multiple lenders simultaneously creates multiple credit enquiries on the co-applicant's CIBIL report. Each hard enquiry can reduce the CIBIL score by 5–15 points. Multiple enquiries in a 30-day window from different lenders can reduce the score by 20–40 points — which may push the score below the threshold for the better-rate PSU bank loan you were also targeting. Vidysea sequences loan applications strategically: one primary application to the best-fit lender, with a backup application queued only if needed.

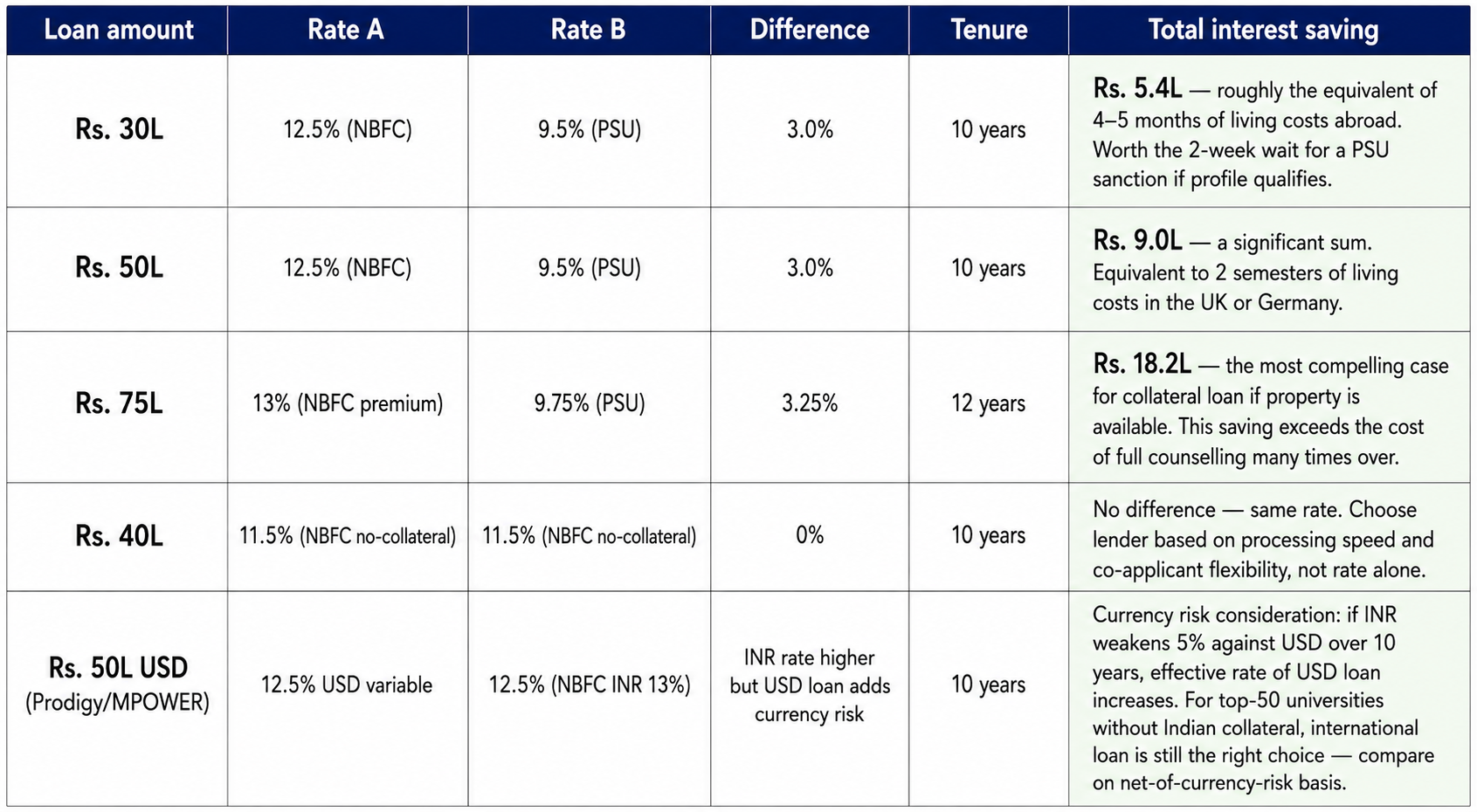

The Real Cost of the Wrong Education Loan for Abroad

The interest rate difference between a PSU bank collateral loan (9.5%) and an NBFC non-collateral loan (12.5%) looks modest in percentage terms. Over a 10-year tenure on a large study abroad student loan, the difference in total interest paid is not modest:

The pre-payment strategy — how to reduce the total cost of your international student loan

Education loans for abroad typically have a moratorium period: no EMI during the study period + 6–12 months after graduation. During this period, interest accrues. The most effective cost-reduction strategy: make interest-only payments during the moratorium if possible (reduces outstanding principal building up), and make partial pre-payments from first salary earnings abroad. Most Indian education loan lenders allow prepayment without penalty after the first year. A student who earns £3,000/month at a UK entry-level role can make Rs. 50,000–80,000/month in pre-payments during the first 2 years of the Graduate Route — reducing the outstanding principal significantly before the full EMI begins.

Quick Student Loan for Visa Deadline — How Vidysea Handles Urgent Cases

Every year, a significant number of Indian students receive visa appointments or final admission confirmations with 3–4 weeks until their deadline. They need a quick student loan — not in the conceptual sense, but in the literal sense: sanction letter in hand before the VFS appointment or the financial proof deadline.

This is manageable. Here is the realistic timeline for a fast-track international education loan in 2026:

- Day 1: Vidysea loan eligibility assessment — 30-minute session. Lender shortlist generated. NBFC recommended for fast-track.

- Day 1–2: Document checklist sent. Documents collected. Application package prepared.

- Day 3: Application submitted to NBFC (Auxilo, InCred, or HDFC Credila for most profiles).

- Day 5–7: Lender issues in-principle approval for strong profiles. Any additional document requests responded to same day.

- Day 7–10: Formal sanction letter issued. Terms reviewed with student and family.

- Day 10–12: Sanction letter formatted for visa financial proof. Combined with bank statements per destination requirement.

Total: 10–12 business days for a complete sanction letter ready for visa submission — achievable for a strong profile with complete documents submitted on Day 1. The single biggest delay factor is document collection — students who take 5 days to gather income proofs add 5 days to the timeline. Vidysea provides the document checklist on the same day as the first session.

What Makes Vidysea's Loan Assistance Different from Going to a Bank Directly

We compare 8+ lenders simultaneously — banks compare 1

When you walk into an SBI branch, you receive advice on SBI's product. When you call HDFC Credila, you receive advice on HDFC Credila's product. When you work with Vidysea, we simultaneously assess your profile against SBI, Bank of Baroda, HDFC Credila, Avanse, Auxilo, InCred, MPOWER, and Prodigy Finance — and recommend the lender whose product matches your profile on rate, timeline, collateral requirement, and visa compatibility. That comparison takes 30 minutes with Vidysea. It takes weeks of separate bank visits independently.

We understand visa financial proof, not just loan documentation

A bank's responsibility ends when the sanction letter is issued. Vidysea's responsibility extends to confirming that the sanction letter — combined with the correct bank statements, in the correct format, for the correct time period — meets the visa authority's financial proof requirement for your specific destination. UK: 28 consecutive days. Germany: Sperrkonto co-ordination. Australia: consistent documented history above EL3 scrutiny floor. Canada: IRCC floor documentation. This is knowledge that no bank's loan team has, and it is the difference between a correct and incorrect financial proof package.

We sequence the application to protect the co-applicant's CIBIL score

Multiple simultaneous loan applications damage the co-applicant's credit score and may jeopardise the loan approval. Vidysea sequences applications: one primary, one backup — never all at once. This protects the CIBIL score while ensuring coverage if the primary lender declines.

We flag TCS implications before disbursement

Tax Collected at Source (TCS) applies to education loan-related foreign remittances above Rs. 7L per financial year at 0.5% TCS (for loan-funded remittances) as per Indian tax law. This is refundable via ITR but adds a cash flow complication if not planned for. Vidysea flags TCS before disbursement so families can structure remittances to minimise the cash flow impact — typically by timing larger disbursements across financial years where possible.

Frequently Asked Questions

Can I get an education loan for abroad without collateral?

Yes — several NBFCs offer no-collateral international education loans to Indian students. Auxilo Finserve and InCred offer unsecured study abroad loans up to Rs. 60–65L without property collateral, based on the co-applicant's income and the student's academic profile. MPOWER and Prodigy Finance require no collateral and no co-applicant — but are limited to top-ranked universities in the US, Canada, and globally. HDFC Credila and Avanse offer hybrid options where collateral is optional above a threshold. The trade-off: no-collateral loans carry higher interest rates (11–13.5% vs. 9–11% for PSU collateral loans).

How does an education loan for abroad work as visa financial proof?

A study abroad loan sanction letter can be used as part of visa financial proof — but the way it is used varies by destination. UK: the sanction letter must be accompanied by bank statements showing 28 consecutive days of the required amount (£9,338–£16,000 depending on location and duration). The loan disbursement must have been received into the bank account within the 28-day window. Germany: loan disbursement must fund the Sperrkonto — the sanction letter alone is not accepted. Australia: loan sanction letter plus income documentation is accepted as financial evidence. Vidysea's Stage 6 review ensures this is structured correctly for every destination before submission.

What is the moratorium period on Indian education loans for abroad, and when do EMIs start?

Most Indian international education loans have a moratorium period that covers: study duration + 6 months to 1 year after graduation (sometimes called the repayment holiday). During this period, you are not required to make full EMI payments — though some lenders charge simple interest which accrues on the principal. EMI repayment begins after the moratorium ends. For a 2-year UK master's + 6 months moratorium, EMIs typically begin approximately 30 months after disbursement. Simple interest payments during the moratorium are optional at most NBFCs but recommended where affordable — they prevent interest from compounding on top of principal and significantly reduce total repayment cost.

Is it better to take a loan in INR (Indian lender) or in USD/GBP (international lender)?

INR-denominated study abroad student loans from Indian banks carry interest in rupees — you know your EMI amount precisely. USD or GBP-denominated loans from MPOWER or Prodigy Finance carry currency risk: if the rupee depreciates against the dollar over the loan tenure, the effective INR cost of each EMI increases. For students without Indian collateral or a co-applicant at a top US university, international lenders are the right choice — the no-collateral advantage outweighs the currency risk. For students with Indian co-applicant income and collateral, an INR loan from a PSU bank or NBFC provides lower overall cost and eliminates currency risk.

The right education loan for abroad is not the one with the lowest advertised rate or the most familiar brand name — it is the one that matches your profile, your timeline, your collateral position, and your visa financial proof requirement simultaneously. That matching is what Vidysea's loan assistance delivers. For families investing Rs. 40–80L in a study abroad programme, the difference between the right international student loan and the wrong one is not trivial: it is measured in lakhs of rupees in interest saved, in visa applications approved or delayed, and in disbursement timing that arrives before the semester deadline instead of after it.

Related Articles

Top Universities for Business Analytics in France 2026: Best Business Schools, Fees, Eligibility, Scholarships & Career Opportunities

Top Universities for MBA in France 2026: Best Business Schools, Fees, Eligibility, Careers & ROI

After MS Jobs in France: Career Opportunities, Salaries, Work Visa & PR Pathways