Best Banks for Study Abroad Education Loans in India 2026 — Ranked and Compared for Indian Students

The question 'which is the best bank for a study abroad education loan in India?' does not have a single answer — it has a profile-specific answer. The best lender for a student who has property worth Rs. 1 Cr, a salaried co-applicant, and 6 weeks before their visa appointment is SBI Global Ed-Vantage at 9.15–11.15%. The best lender for a student who has no property, a visa appointment in 3 weeks, and needs Rs. 45L, is Auxilo Finserve in 5–8 days. These are different answers for different profiles — and choosing the wrong one costs money, time, or both.

Team Vidysea

June 1, 2026

This guide ranks 10 lenders for study abroad student loans in India in 2026 — PSU banks, private banks, specialist NBFCs, and international lenders — with a clear ranking rationale, a use-case matrix that maps each lender to the profile it serves, and the interest savings calculation that shows exactly how much money is at stake in the rate decision. It also covers the quick student loan options specifically for students with visa deadlines approaching, and what to look for beyond the headline rate.

The guide includes every lender type: PSU banks (SBI, Bank of Baroda, PNB) for lowest rate, NBFCs (HDFC Credila, Avanse, Auxilo, InCred) for speed and flexibility, private banks (Axis Bank) for relationship holders, and international lenders (MPOWER, Prodigy Finance) for students with no Indian co-applicant. No lender paid to appear on this list — the rankings reflect rate, processing speed, university coverage, visa documentation quality, and borrower flexibility

⭐ The single most important insight in this guide

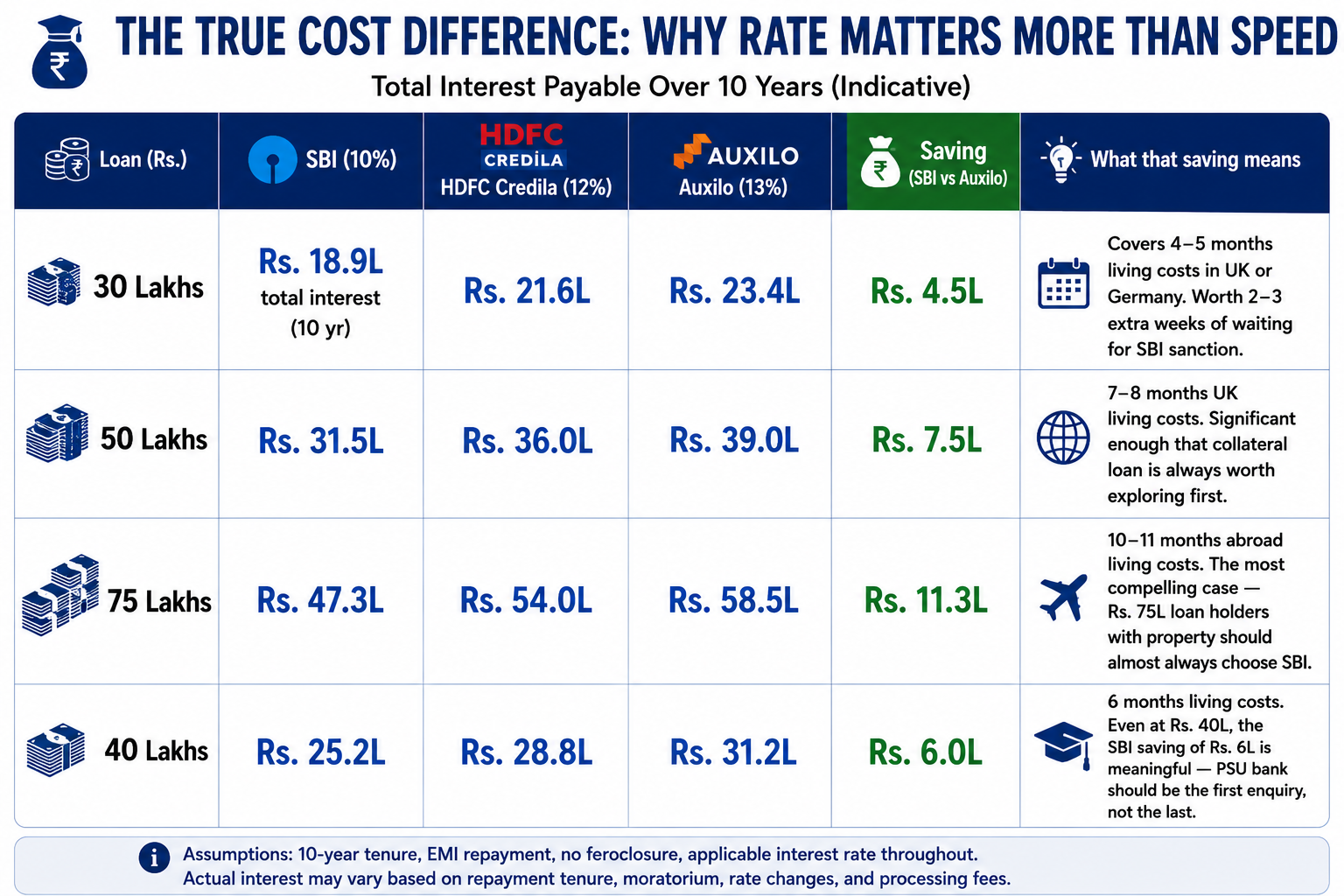

For most Indian students with collateral property and 4+ weeks before their visa deadline: SBI Global Ed-Vantage is the correct answer on financial grounds alone. The interest rate advantage (9.15–11.15% vs. 11–13.5% for NBFCs) on a Rs. 50L loan over 10 years is Rs. 5–8L. On Rs. 75L: Rs. 8–12L. These are not marginal savings — they represent 6–12 months of living costs abroad. Every family with property should get an SBI quote before committing to any NBFC.

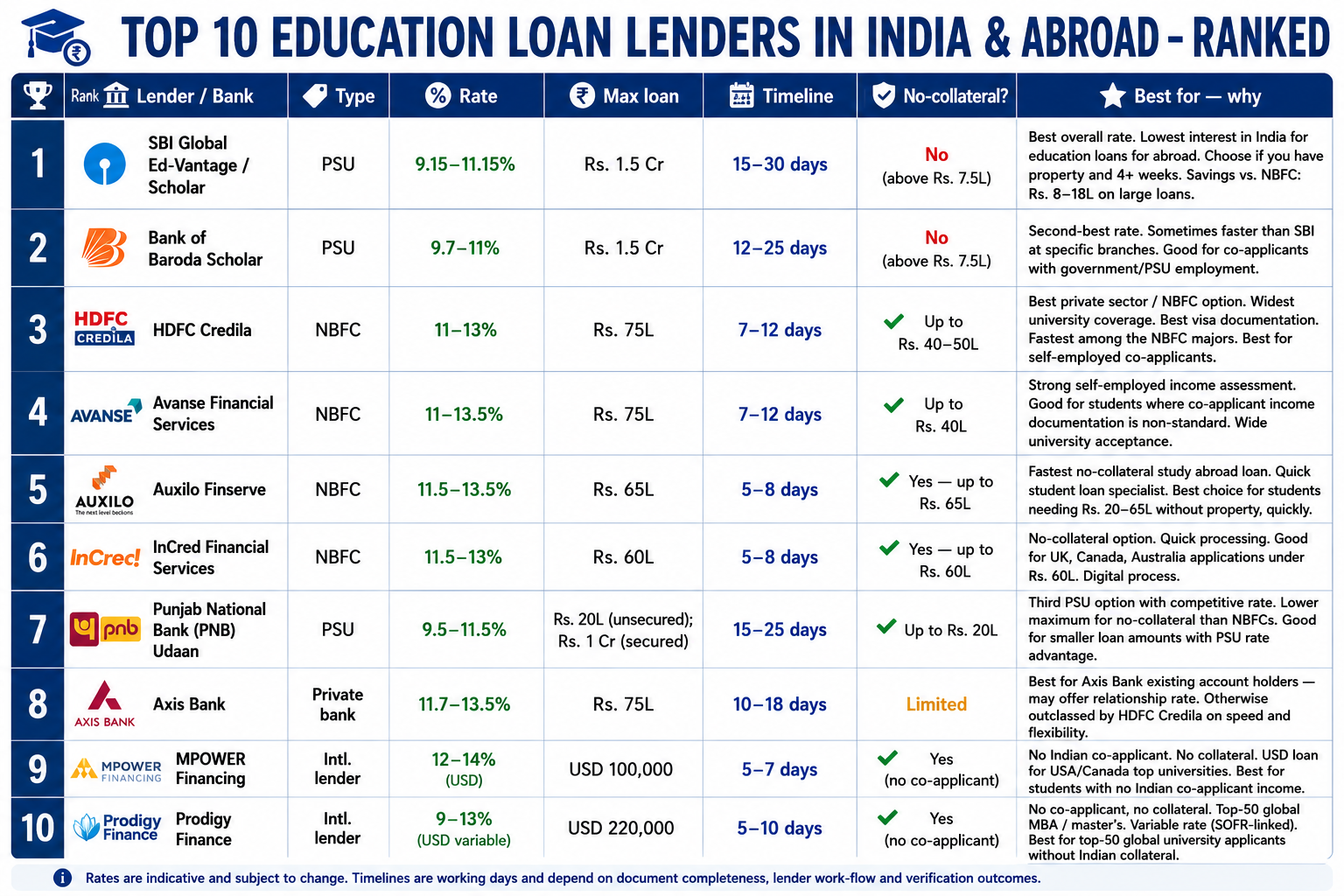

Top 10 Banks and Lenders for Study Abroad Education Loans in India 2026

Ranked by best overall value for Indian students — rate, speed, coverage, and borrower flexibility all considered:

✅ How to read this ranking

Rank 1–2 (PSU banks) are the best on rate — choose them if property is available and timeline allows. Rank 3–6 (NBFCs) are the best on speed and flexibility — choose them if timeline is tight, no property, or self-employed co-applicant. Rank 7 (PNB) is a PSU alternative if SBI and BoB processing times are too long at local branches. Rank 8 (Axis Bank) is only competitive for existing Axis relationship holders. Rank 9–10 (international lenders) are for students without Indian co-applicant income or property. Vidysea recommends comparing quotes at Ranks 1, 3, and 5 simultaneously — three lenders covering three different use cases.

PSU Banks — Why They Rank First Despite Slower Processing

Public Sector Undertaking (PSU) banks — SBI, Bank of Baroda, and PNB — rank first in this guide because they offer the lowest interest rates for education loans for abroad available anywhere in India. The rate advantage (9.15–11.15% vs. 11–13.5% for NBFCs) sounds small in percentage terms. In rupee terms over a 10-year tenure, it is the single largest financial variable in the study abroad loan decision:

⚠️ The PSU bank application mistake that costs students time

Many students apply to a general SBI or BoB retail branch and experience slow processing. The faster route: SBI has dedicated 'Scholar' and 'Global Ed-Vantage' branches or desks at major branches that process education loans separately from general retail applications. Bank of Baroda has similar specialist desks. Applying at the right desk can reduce processing time by 5–10 days. Ask specifically for the 'education loan officer' or the 'NRI/overseas education desk' — not the general counter.

NBFCs — Why They Rank for Speed and Flexibility

Non-Banking Financial Companies (HDFC Credila, Avanse, Auxilo, InCred) rank below PSU banks on rate but outperform them on three dimensions that matter for many students:

- Processing speed: 5–12 working days vs. 15–30 for PSU banks. For students with visa deadlines in 2–3 weeks, NBFCs are the only viable option.

- No-collateral loans: NBFCs offer genuine no-collateral study abroad loans up to Rs. 65L (Auxilo), Rs. 60L (InCred), Rs. 50L (HDFC Credila, Avanse). PSU banks require collateral above Rs. 7.5L in most cases.

- Self-employed co-applicants: NBFCs — particularly HDFC Credila and Avanse — have more developed income assessment processes for self-employed co-applicants. PSU banks are often conservative and slow on self-employed income verification.

The rate premium for choosing an NBFC over SBI is real — but for students without property, or with a visa deadline that cannot wait, NBFCs are the right tool for the right job, not a compromise. The mistake to avoid: choosing an NBFC when you have property and time, simply because the application is easier. The Rs. 5–10L saving from SBI is always worth the 2–3 extra weeks.

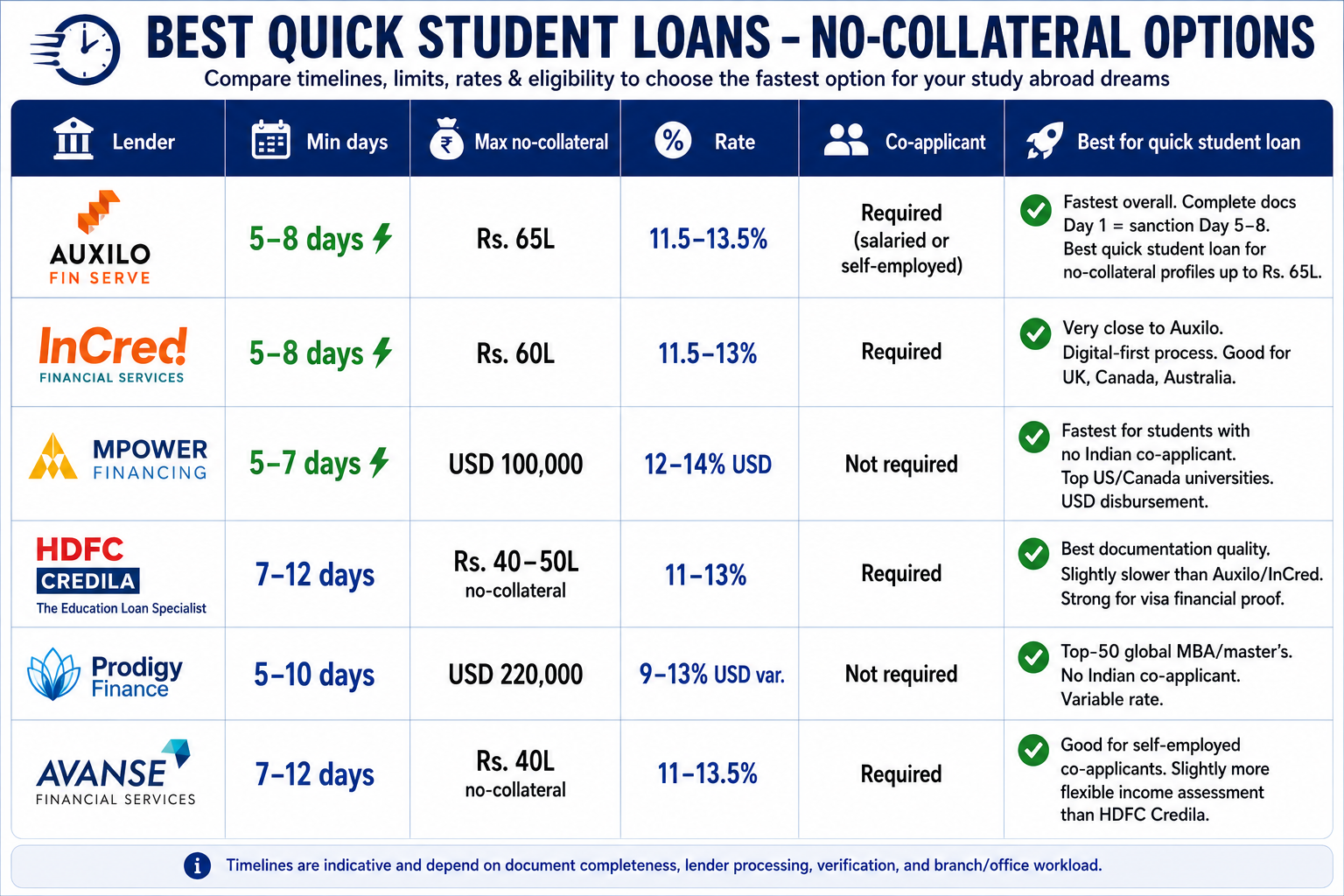

Quick Student Loan Options — When the Deadline Is Close

For students with visa financial proof deadlines in 2–4 weeks, here are the quick student loan options available in 2026:

💡 The fastest realistic timeline for a complete application

For Auxilo or InCred: submit a 100% complete application (all documents collected) on Monday morning. By end of following week (Day 7–8), sanction letter issued for strong profiles. The single biggest delay: document collection. Students who contact a lender and then spend 5 days collecting documents add 5 days to the timeline. Collect every document before contacting any lender. Vidysea provides the document checklist in the first session — students who do this arrive at the lender with everything needed on Day 1.

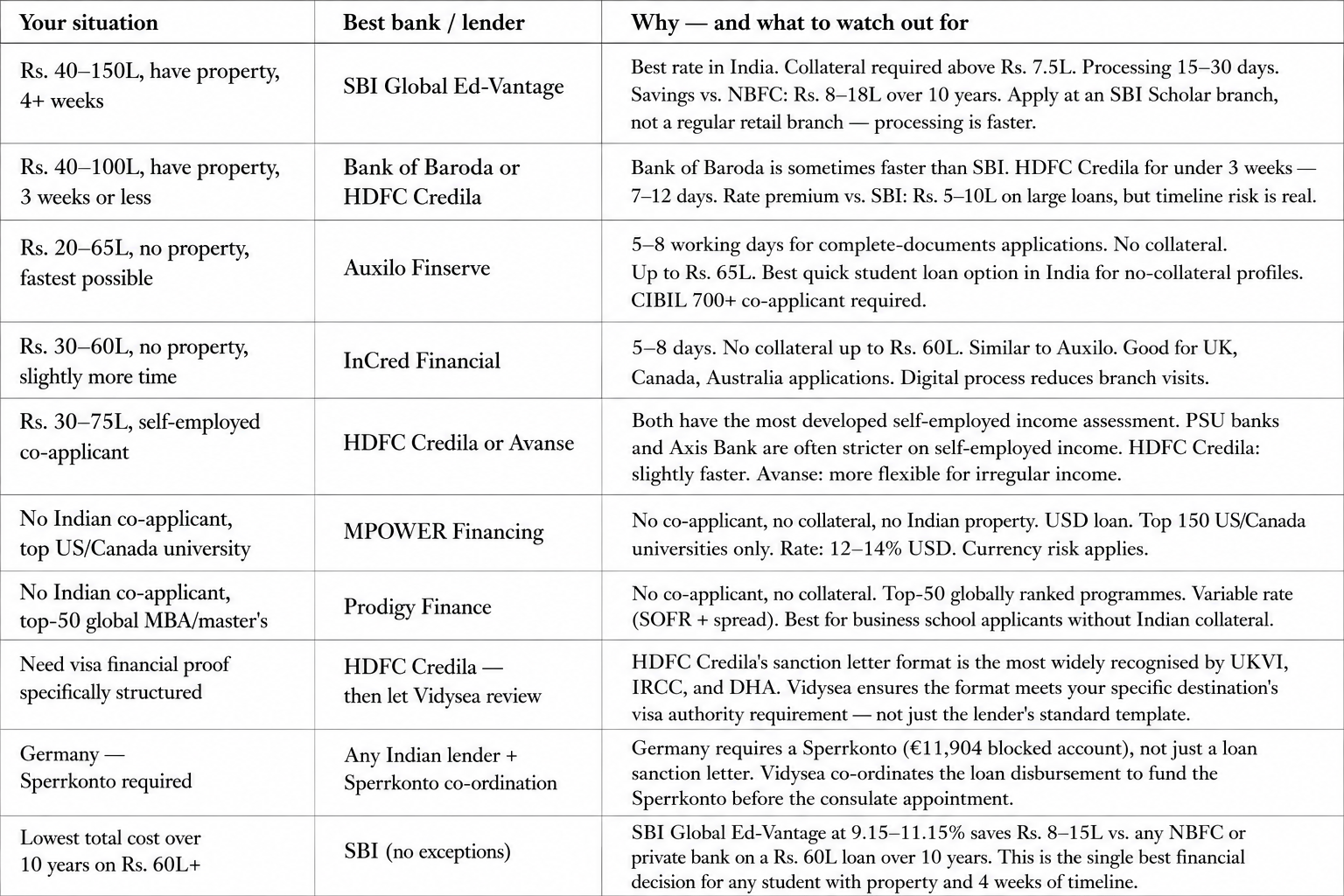

Which Lender for Which Profile? Complete Use-Case Matrix

This matrix maps 10 specific borrower situations to the recommended lender and the exact rationale:

What to Look for Beyond the Headline Rate

The interest rate is the most important variable in a study abroad student loan — but it is not the only variable. These four additional factors affect the true cost and usability of the loan:

Prepayment terms

Students who return to India after a PGWP/work visa abroad and then repay their loan from Indian income — or who make prepayments from strong overseas salary — benefit enormously from nil prepayment penalty after the initial period. HDFC Credila: nil after 12 EMIs. SBI: typically nil after lock-in (check current terms). Axis Bank and HSBC: typically 2–3% in early years. A student planning to repay aggressively from overseas salary should prioritise lenders with the best prepayment terms.

Moratorium period

The moratorium (repayment holiday) covers study duration + a grace period after graduation. Most Indian lenders: study duration + 6–12 months. Simple interest accrues during the moratorium and is typically capitalised into the principal. Making interest-only payments during the moratorium where affordable significantly reduces the total outstanding principal at EMI commencement — and is one of the most effective cost-reduction strategies available.

Visa documentation quality

A sanction letter that meets the lender's standard but does not meet the specific visa authority's requirement is a problem that surfaces at the worst possible moment — the visa application. HDFC Credila's sanction letter format is the most widely recognised by UKVI (UK), IRCC (Canada), and DHA (Australia). PSU bank sanction letters are also widely accepted. The issue arises most frequently with smaller NBFCs or less common lenders whose letter formats are unfamiliar to visa officers. Vidysea reviews every sanction letter for visa compatibility before submission — regardless of which lender issued it.

TCS (Tax Collected at Source)

International remittances from India above Rs. 7L per financial year attract TCS at 0.5% for education loan-funded remittances (higher for non-loan-funded remittances). TCS is refundable via ITR but creates a cash flow consideration. Structuring disbursements across financial years (April–March) where possible reduces the cash flow impact. This is a planning detail that most families are not aware of until their first disbursement — Vidysea flags it before disbursement.

Frequently Asked Questions

Is SBI always the best bank for study abroad education loans in India?

For students with collateral property and 4+ weeks of timeline: yes, SBI is almost always the best financial choice. The rate advantage (9.15–11.15% vs. 11–13.5% for most NBFCs) is real and compounding over 10 years. The caveat: SBI's processing quality varies significantly by branch. Apply at a dedicated Scholar/Education branch or at a large PSU bank branch with a specialist education loan desk. If your SBI branch is slow or unresponsive, Bank of Baroda at a comparable rate and slightly faster processing is the right fallback.

Which bank is best for a study abroad loan without collateral?

For no-collateral international education loans up to Rs. 65L: Auxilo Finserve is the best combination of speed, loan amount, and acceptance rate. For Rs. 60L: InCred Financial is a close alternative. For profiles needing Rs. 40–75L with slightly more time: HDFC Credila has the best documentation quality and university network. PSU banks (SBI, BoB) generally require collateral above Rs. 7.5L. For students with no Indian co-applicant income at all: MPOWER (USA/Canada) or Prodigy Finance (top-50 global) are the only realistic options.

Can I switch my study abroad loan from an NBFC to SBI later?

Yes — balance transfer from NBFC to PSU bank is available after a period of timely EMI repayment. Most PSU banks offer education loan balance transfer products. The practical benefit: if you took an NBFC loan (11–13%) for timeline reasons, once you have Indian employment income and a track record of repayment, you can refinance to SBI's lower rate. The process takes 3–4 weeks and requires updated documentation. The rate saving on a Rs. 60L balance transferred from 12.5% to 10% is approximately Rs. 18,000–22,000 per year in reduced interest — worth doing as soon as eligibility is established.

The best bank for your study abroad education loan is determined by four variables: your loan amount, whether you have collateral property, your co-applicant income type, and your visa deadline. These four variables, combined and assessed against the 10 lenders in this guide, produce a specific recommendation — not a general one. SBI if property and time. Auxilo if speed and no collateral. HDFC Credila if speed, flexibility, and documentation quality. MPOWER or Prodigy if no Indian co-applicant. Any answer more specific than this requires knowing your specific profile — which is what a Vidysea loan session delivers in 30 minutes.