Collateral vs Non-Collateral Education Loans: Complete Comparison for Study Abroad 2026

When an Indian family sits down to plan a study abroad student loan, the first question most banks and NBFCs ask is: "Do you have property to pledge?" The answer to that question determines almost everything else — interest rate, loan ceiling, processing time, and the risk the family bears if repayment becomes difficult.

Team Vidysea

May 20, 2026

The choice between a collateral-backed education loan (secured against property, FD, or insurance) and a non-collateral education loan (unsecured — no asset pledge) is the most financially consequential decision in the entire study abroad process. Get it right and you pay the lowest possible interest rate for the loan you need. Get it wrong and you either encumber a family asset unnecessarily or pay Rs. 12–17 lakh in excess interest over a 10-year repayment period.

This guide covers the complete comparison across every dimension that matters for an international education loan in 2026: cost, risk, eligibility, processing, lender options, and the specific scenarios where each structure is the right choice.

💡 The fundamental trade-off

A collateral loan offers a lower interest rate in exchange for greater family asset risk. A non-collateral loan offers zero asset risk and faster processing in exchange for a higher interest rate. Neither is universally better — the right choice depends on your loan amount, your family's collateral availability, your intake timeline, and your tolerance for asset encumbrance. This guide helps you calculate which trade-off is right for your situation.

Collateral vs Non-Collateral — Complete 2026 Comparison

This table covers every dimension relevant to an international student loan decision for Indian families:

| Dimension | Collateral-backed loan (secured by property / FD / insurance / gold) | Non-collateral loan (unsecured — no asset pledge required) |

|---|---|---|

| What you pledge | Property (residential/commercial), FD, gold, insurance policy — pledged as security. If you default, lender can sell the asset. | Nothing. Loan approved on the basis of your academic profile, university ranking, programme, co-applicant income, and co-applicant CIBIL score. |

| Maximum loan amount | Rs. 1.5 Cr+ (high collateral value unlocks higher amounts). Some PSU banks lend up to Rs. 1.5–2 Cr against property. | Rs. 75L (most NBFCs and private banks). Rs. 1 Cr from HDFC Credila and ICICI for select elite programmes. USD 220K from Prodigy Finance. |

| Interest rate | 7.5–10.5% — significantly lower. Collateral reduces lender risk, so they pass the saving to you. SBI at 7.5–8.5% with property collateral. | 10.5–14%. Higher rate compensates for unsecured risk. NBFCs typically at 11–13.5%. Prodigy Finance / MPOWER: 11–15% in USD. |

| Processing time | Longer — 21–45 days. Collateral valuation, legal verification of title deeds, and MODT registration add time. | Faster — 5–30 days. No collateral valuation needed. Quick student loan from NBFCs (Leap, Avanse): 5–14 days. |

| Who qualifies | Anyone with sufficient collateral value. Academic profile matters less when collateral is strong. | Admitted students at QS top-200 universities with co-applicant income Rs. 20K+/month and CIBIL 700+. University ranking is the primary 'collateral'. |

| Risk to family | Higher risk — family property is legally encumbered. If you default or cannot repay, the bank can auction the property. | Lower asset risk — no family property at stake. The risk is limited to co-applicant's CIBIL damage if EMIs are missed. |

| Documents required | Admission letter + academic docs + co-applicant income docs + complete property papers (title deed, valuation, encumbrance certificate, MODT). | Admission letter + academic docs + co-applicant income proof + co-applicant CIBIL. Significantly fewer documents. |

| Loan above Rs. 75L | Yes — with sufficient collateral, Rs. 1–1.5 Cr is achievable. | Difficult above Rs. 75L without a collateral bridge. Some banks can reach Rs. 1 Cr for exceptional profiles (QS top-20 university + strong co-applicant). |

| Best lenders | SBI (8.15–9%), Bank of Baroda, Canara Bank, PNB (lowest rates with property collateral). HDFC Credila offers hybrid models. | Avanse, Leap Finance, InCred, Auxilo (NBFCs — fast). HDFC Credila (hybrid). Prodigy Finance, MPOWER (no Indian co-signer needed). |

| Total cost of borrowing | Lower — Rs. 50L at 9% over 10 years = Rs. 80L total repayment (Rs. 30L interest). vs. 12.5% = Rs. 92L (Rs. 42L interest). | Higher — Rs. 50L at 12.5% over 10 years = Rs. 92L total. The Rs. 12L difference vs. collateral loan represents the 'price of unsecured convenience'. |

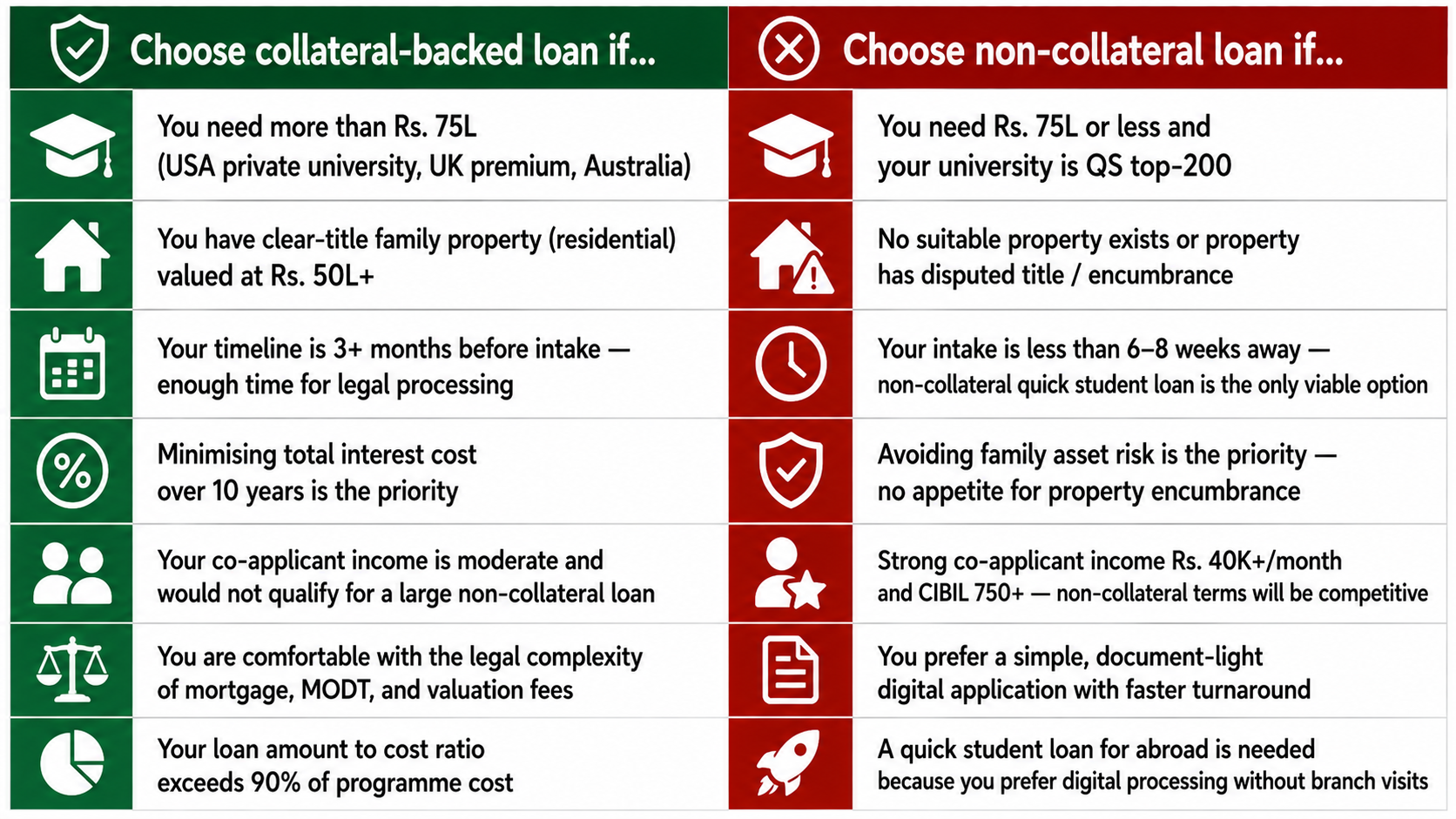

| Is it right for you? | Right if you have a family property, need > Rs. 75L, have time for processing, and want the lowest possible interest cost over the loan tenure. | Right if no suitable property exists, timeline is tight, loan amount is Rs. 75L or less, or you want to avoid encumbering family assets. |

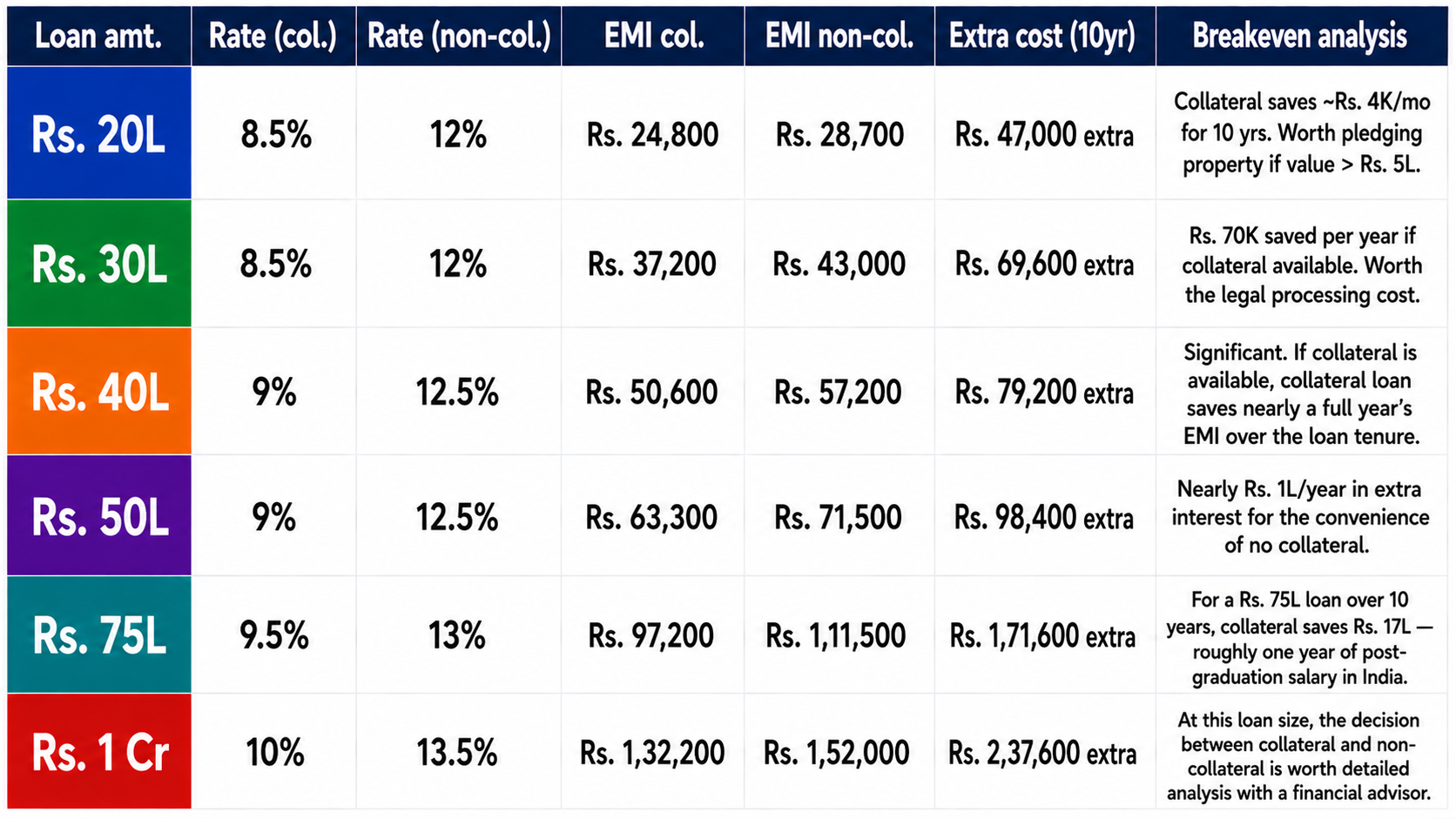

The Real Cost Difference — How Much More Does Non-Collateral Cost?

The interest rate difference between collateral (8.5–9.5%) and non-collateral (11.5–13.5%) study abroad loans looks like 2–4% on paper. Over a 10-year repayment period, it adds up to a very concrete amount. Here is the honest arithmetic for common loan amounts:

🔑 The Rs. 12–17 lakh decision

For a Rs. 75L education loan for abroad, the choice between 9.5% (collateral) and 13% (non-collateral) over 10 years costs approximately Rs. 17 lakh extra in interest. That is roughly one year of post-graduation salary in India, or 4–5 months of salary in Europe. Before dismissing collateral as 'too complicated', calculate your total interest cost both ways. The arithmetic often makes the legal processing worth it.

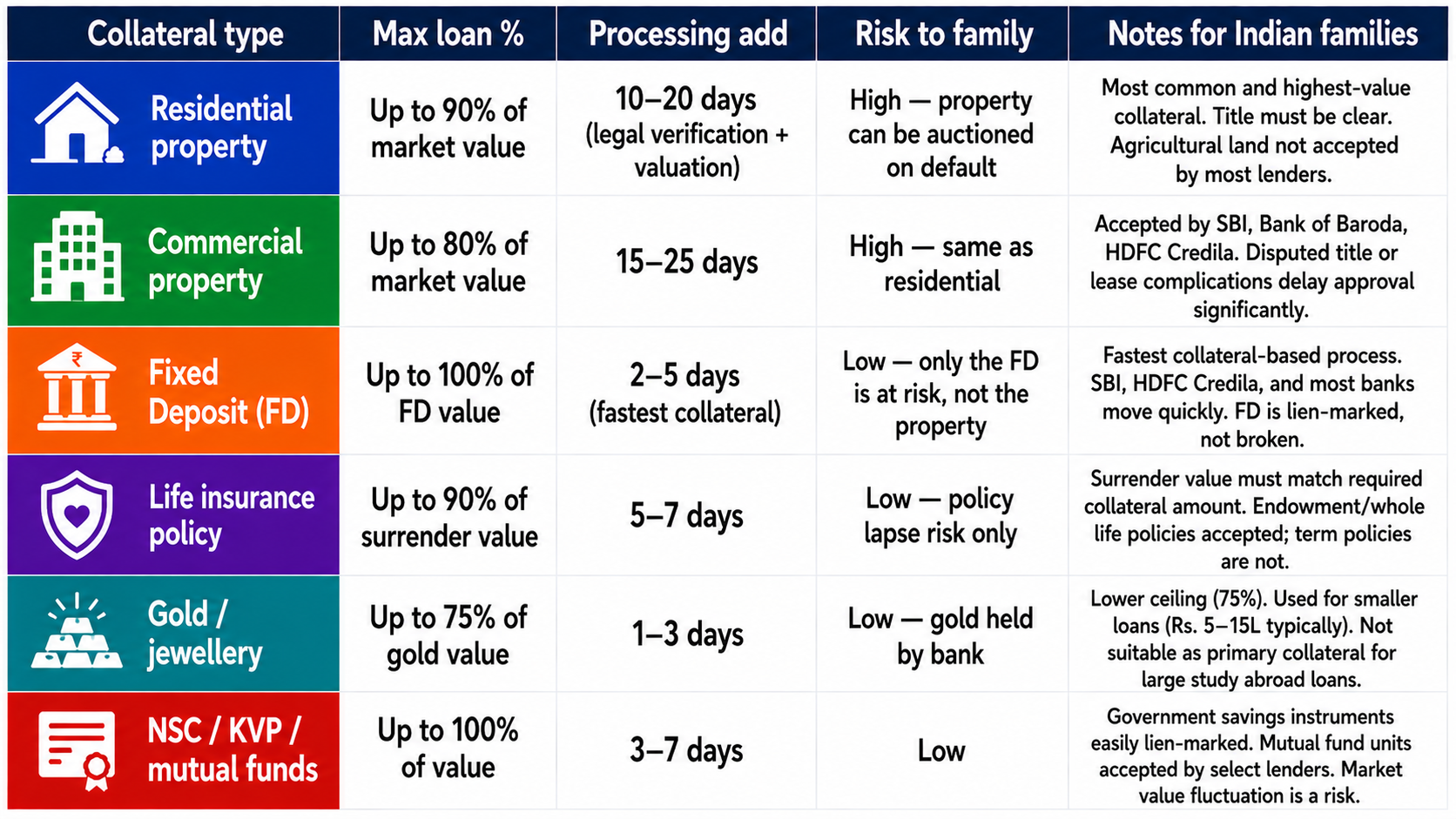

What Can You Use as Collateral — and What Each Type Means

Not all collateral is equal. FD-backed loans process fastest. Property-backed loans allow the highest amounts. Understanding what each type of collateral offers — and the specific requirements — prevents surprises mid-application:

✅ FD is the fastest and cleanest collateral option

If your family has a Fixed Deposit of Rs. 20L+, using it as collateral for an education loan is the fastest secured-loan path available. SBI can process an FD-backed student loan for abroad in 2–5 days — comparable to an unsecured NBFC loan but at 2–3% lower interest rate. The FD is lien-marked (frozen but not broken), you continue earning interest on it, and you get a lower loan rate. For families with FDs and time sensitivity, this is often the optimal structure.

Which Structure Is Right for You?

Use this picker to identify your path:

⚠️ The hybrid option most families miss

HDFC Credila and some private banks offer a hybrid structure: base non-collateral approval (Rs. 40–50L) supplemented with partial collateral to unlock a larger amount or lower rate. For example, a family taking Rs. 80L for a US MS programme may structure Rs. 50L as non-collateral (fast approval at 12%) and Rs. 30L as collateral-backed (adding property but lowering the blended rate to approximately 10.5%). This hybrid approach is worth discussing with the lender when the loan amount exceeds Rs. 50L.

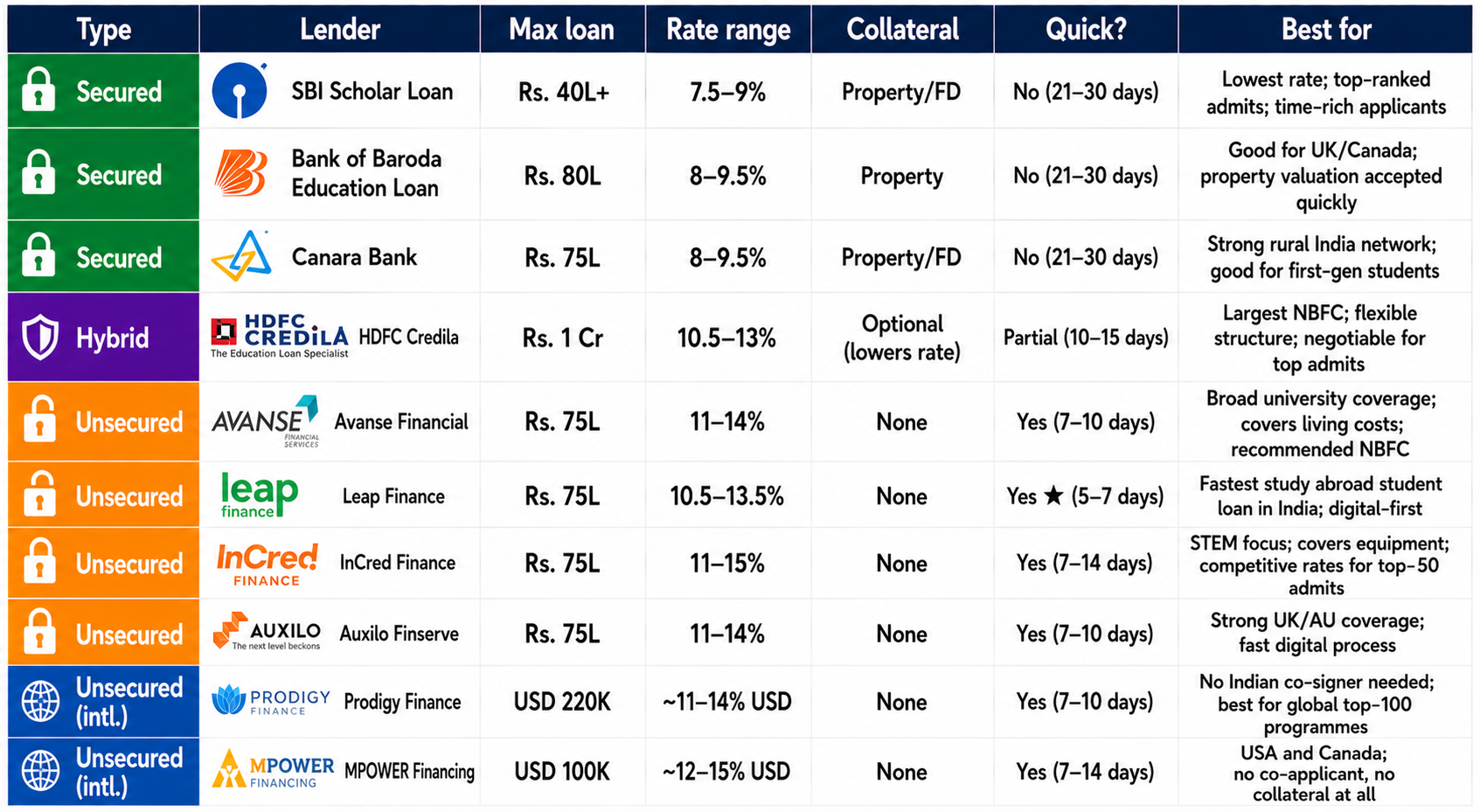

Lenders Mapped by Loan Type — Study Abroad 2026

Here are the major international education loan lenders in India, mapped by whether they are secured, unsecured, or hybrid — with the key metrics for each:

✅ Leap Finance: the fastest quick student loan in India

For students who need a quick student loan approved in under a week — Leap Finance processes applications for partner university admits in 5–7 business days with a fully digital process. Rs. 75L maximum, no collateral, no branch visit. The rate is higher than SBI (10.5–13.5% vs. 8.5%), but for students with a September 2026 intake and a visa appointment in 6 weeks, speed is worth the premium. Prodigy Finance and MPOWER offer similar speed for international students who do not have a qualifying Indian co-applicant.

Application Process: Collateral vs Non-Collateral

The application experience is fundamentally different between the two loan types — and for many families, the simplicity of the non-collateral process is itself a significant factor.

Collateral-backed loan process

- Step 1 — Identify collateral asset and confirm with family: clear title, no existing mortgage, valuation in range (typically 2–4 weeks before application)

- Step 2 — Collect property documents: title deed, encumbrance certificate, property tax receipts, latest valuation from bank-approved valuer

- Step 3 — Submit loan application with all academic docs + property docs + co-applicant income docs

- Step 4 — Bank conducts legal verification of title and independent valuation (adds 10–15 days)

- Step 5 — MODT (Memorandum of Deposit of Title Deeds) registration at sub-registrar office (adds 2–3 days + stamp duty cost)

- Step 6 — Loan sanction and disbursement — total timeline 21–45 days from application

Non-collateral loan process

- Step 1 — Collect academic documents + admission letter + co-applicant income proof + CIBIL report

- Step 2 — Submit online application (most NBFCs: fully digital)

- Step 3 — Lender verifies documents and co-applicant profile (3–5 business days for fast NBFCs)

- Step 4 — Loan sanction issued — 5–14 days from application (Leap, Avanse)

- Step 5 — Disbursement after visa approval — per semester, directly to university bank account for tuition

The non-collateral process requires significantly fewer documents — no property papers, no legal verification, no MODT registration. For a family in Mumbai applying to a US programme with a visa appointment in 8 weeks, the non-collateral NBFC route is the only practical option.

Frequently Asked Questions

Can I start with a non-collateral loan and add collateral later to reduce my rate?

Yes — some lenders allow rate reduction mid-tenure if you pledge collateral after the initial sanction. This is most common with HDFC Credila and private banks. The process: after your loan is disbursed, pledge the collateral and request a rate revision. Lenders are not obligated to offer this, but for large loan amounts (Rs. 50L+) it is worth negotiating. The cost savings over the remaining tenure often justify the legal processing cost of adding collateral post-sanction.

What if my property has a joint title (two or more family members)?

Property with joint title can still be used as collateral, but all title holders must consent to the mortgage and sign the MODT documents. If any co-owner is unavailable or unwilling, the property cannot be used. This is one of the most common reasons families discover their collateral option is blocked mid-application. Verify co-owner availability and willingness before committing to a collateral-backed loan timeline.

Does a non-collateral loan affect my family's ability to use their property for other purposes?

No — because nothing is pledged. With a non-collateral loan, your family's property remains fully unencumbered. They can sell it, mortgage it for other purposes, or transfer it at any time during the loan tenure. This is the core appeal of the unsecured international student loan for families who are cautious about asset encumbrance.

My co-applicant has a CIBIL score of 680. Can I still get a non-collateral loan?

It is difficult but not impossible. Most NBFCs prefer CIBIL 700+ for non-collateral approvals. At 680, you may be approved at a higher rate (1–2% above standard) or for a lower loan amount. Alternatively: (1) Spend 2–3 months building the co-applicant's CIBIL by settling any outstanding credit card dues and ensuring no missed payments. (2) Switch to a collateral-backed structure where the property reduces reliance on CIBIL. (3) Apply to Prodigy Finance or MPOWER, which use different eligibility models and do not require an Indian co-applicant at all.

For a Rs. 50L loan, should I use collateral even though I qualify for non-collateral?

Run the arithmetic. At Rs. 50L, the difference between 9% (collateral) and 12.5% (non-collateral) over 10 years is approximately Rs. 98,000 per year in extra interest — close to Rs. 10 lakh over the full tenure. If your family has a clear-title property and your intake is 3+ months away, pledging the property saves Rs. 10 lakh. If the family is not comfortable pledging property or the intake is too close for legal processing, the non-collateral premium is the price of that peace of mind or convenience. The decision is financial and emotional — not purely rational.

The collateral vs non-collateral decision is not a binary of 'secure the family home' versus 'pay extra forever'. It is a structured trade-off that has a right answer for each family based on their collateral availability, loan amount, timeline, and risk tolerance. Calculate the cost difference. Assess the risk. Make the decision from data, not default.

Related Articles

Cost of Study in France: Complete Guide to Tuition Fees, Living Expenses & Student Budgeting

Top Universities for MS in France 2026: Best Universities for Engineering, Computer Science, Data Science & Business Analytics

CMA in France 2026: Complete Guide to Certification, Eligibility, Fees, Salary & Career Opportunities