Documents Required for an Education Loan in India

An education loan for abroad studies is one of the most significant financial decisions an Indian student and their family will make. Whether you are applying to a university in the United States, Canada, the United Kingdom, Australia, Germany, or any other country, the loan application process in India follows a broadly similar structure — with one major variable: the completeness and quality of your documentation.

Team Vidysea

May 22, 2026

Banks and Non-Banking Financial Companies (NBFCs) assess education loan for study abroad applications entirely on the basis of the documents you submit. There is no interview, no relationship manager judgment, and no discretion — the documents either meet the criteria or they do not. A missing income proof, an incorrectly formatted bank statement, or a collateral document with a discrepancy in the applicant's name is enough to delay or reject a loan application that was otherwise entirely viable.

This guide covers every document required for an education abroad loan in India — organised by category, explained in terms of what each document proves, and annotated with the common mistakes that delay applications. Whether you are applying to SBI, Bank of Baroda, HDFC Credila, Avanse, Axis Bank, or any other lender, this document checklist covers what every major Indian lender requires for education loan for overseas studies.

🔴 Why documentation quality determines your loan outcome: Unlike a visa application where an immigration officer can exercise judgment, an education loan is assessed against a checklist. A loan officer at SBI or HDFC Credila has limited discretion — they approve or reject based on whether your file meets the criteria. Incomplete documentation does not result in a conversation; it results in a delay or a rejection letter. Get your documentation right before submission — not after.

Understanding the Education Loan Document Framework

Every student education loan for study abroad application in India requires documents across five broad categories:

- Student documents — establishing identity, academic qualifications, and admission

- Co-applicant/guarantor documents — establishing the income and repayment capacity of the primary financial supporter

- Collateral/security documents — for loans above a threshold (typically INR 7.5 lakh for most PSU banks), establishing the value and ownership of the asset being pledged

- University and course documents — establishing the institution's credibility, course duration, and total cost of education

- Loan-specific declarations and forms — the bank's own forms, declarations, and mandated certifications

The specific documents required under each category vary slightly between lenders. Public Sector Banks (PSU banks) such as SBI, Bank of Baroda, and Canara Bank follow RBI guidelines and typically require more documentation than private NBFCs such as HDFC Credila, Avanse, and Auxilo. However, the core framework is consistent across all lenders offering student loans for overseas study.

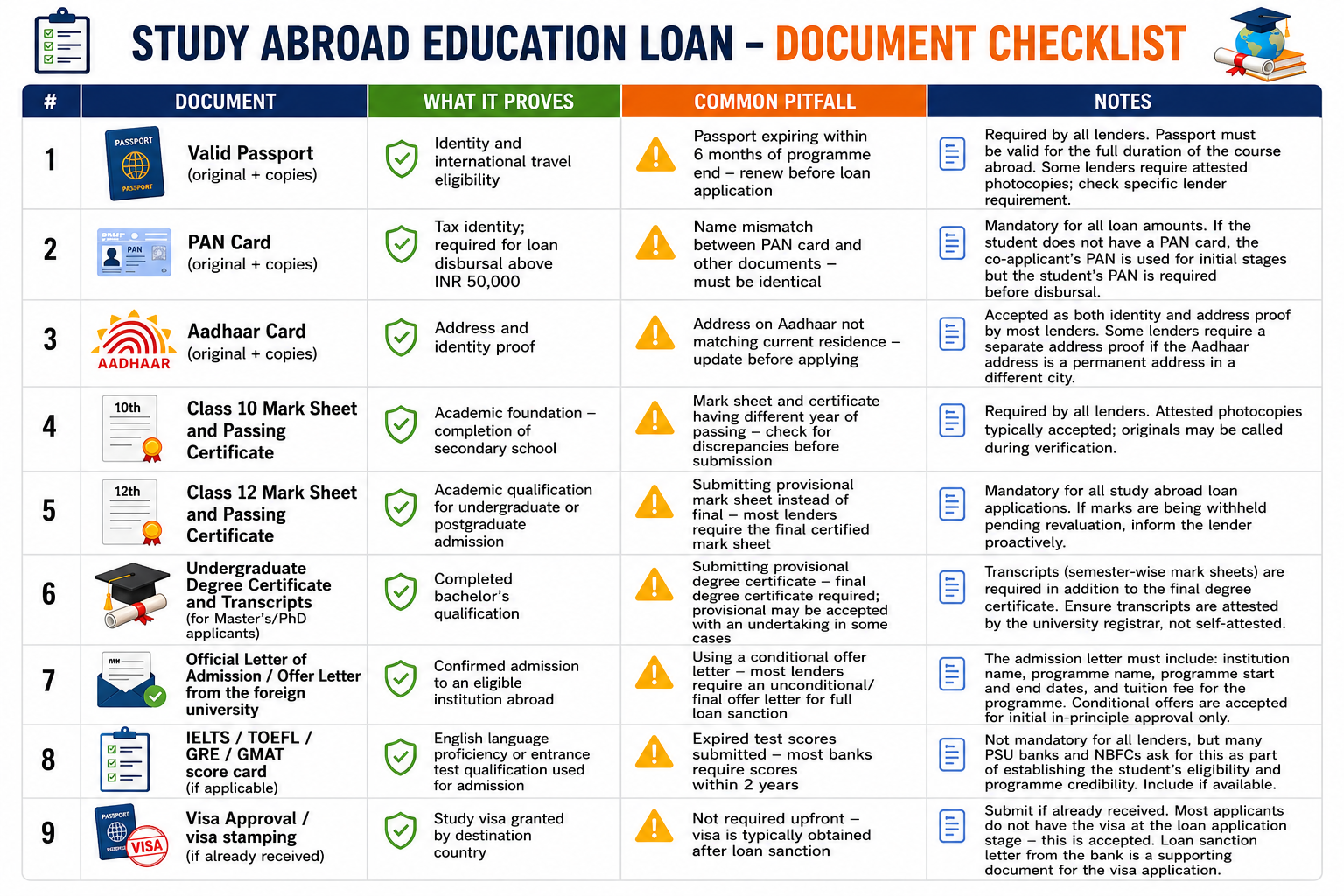

Category 1 — Student Documents

Student documents establish who you are, your academic background, and the fact that you have been admitted to an eligible institution abroad. For any student loans for students studying abroad, these are the foundational documents without which the application cannot proceed.

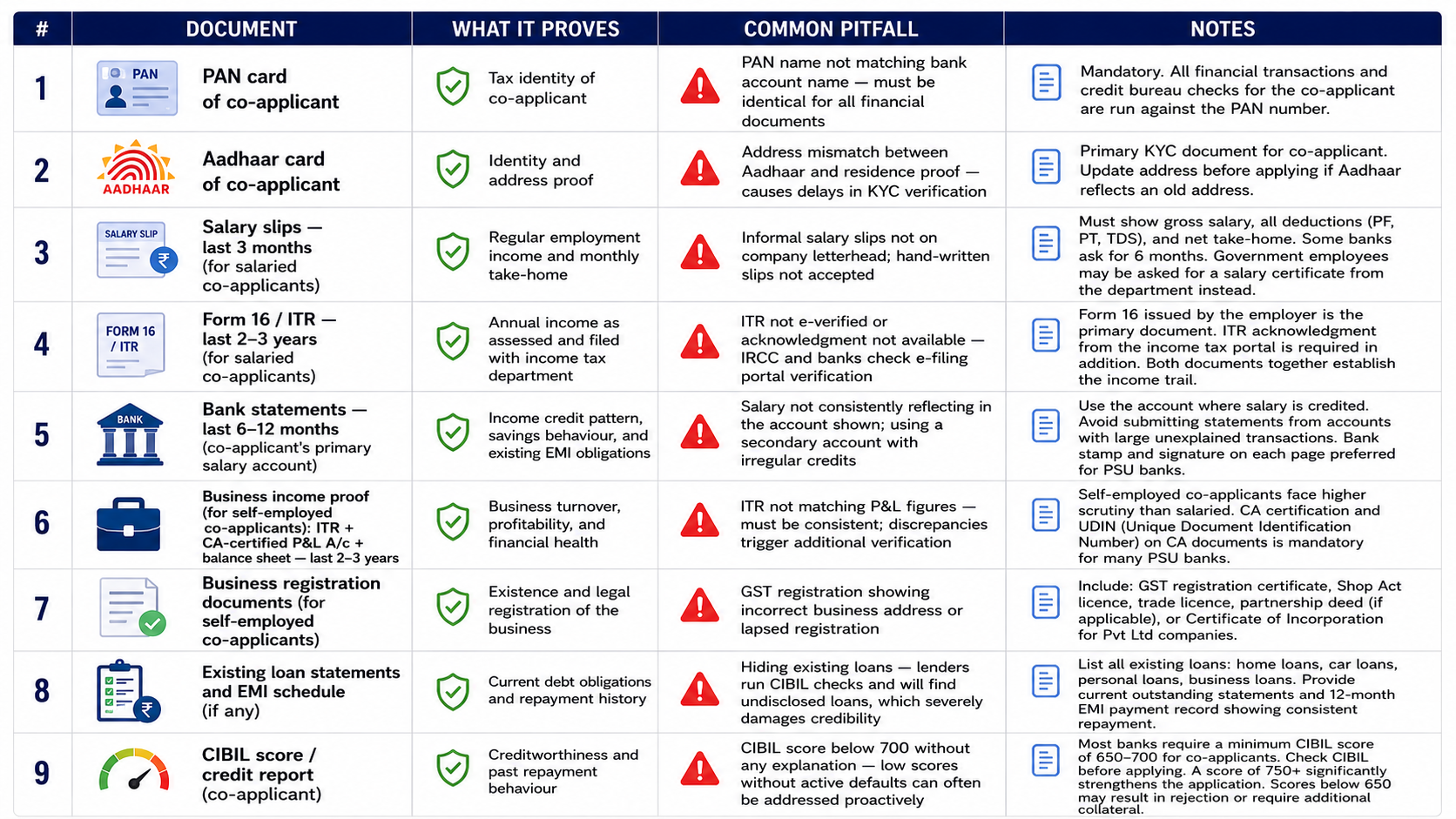

Category 2 — Co-Applicant and Guarantor Documents

For every overseas education loan in India, the student is the primary borrower but cannot be the sole applicant — a co-applicant (typically a parent or legal guardian) is mandatory for all lenders. The co-applicant's documents establish the income, financial history, and repayment capacity that the lender is actually underwriting the loan against. These documents carry the most weight in the credit assessment.

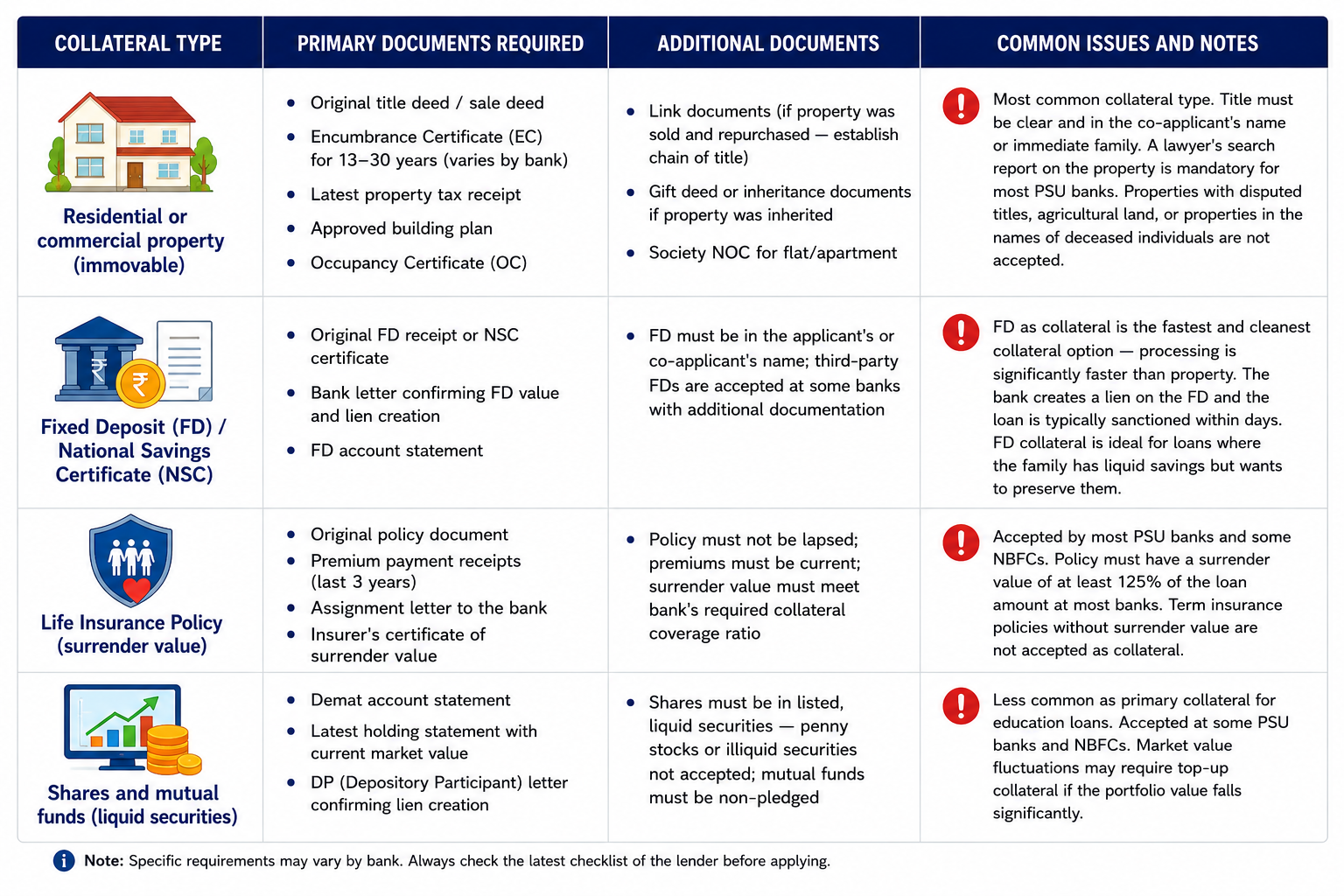

Category 3 — Collateral and Security Documents

Most Indian lenders offer education loan for overseas education in two structures: secured (with collateral) and unsecured (without collateral). The threshold at which collateral becomes mandatory varies by lender — most PSU banks require collateral for loans above INR 7.5 lakh, while some NBFCs offer unsecured loans up to INR 40–75 lakh depending on the student's profile and institution. When collateral is pledged, the following documents are required:

💡 FD as collateral is the fastest route to loan sanction. If your family has liquid savings in fixed deposits, using the FD as collateral (instead of property) dramatically speeds up the loan processing timeline. Property verification — legal search, technical valuation, encumbrance certificate — takes 2–6 weeks. FD lien creation takes 1–3 days. For students with urgent loan disbursement timelines (university deposit deadlines, visa requirements), FD collateral is strongly recommended where available.

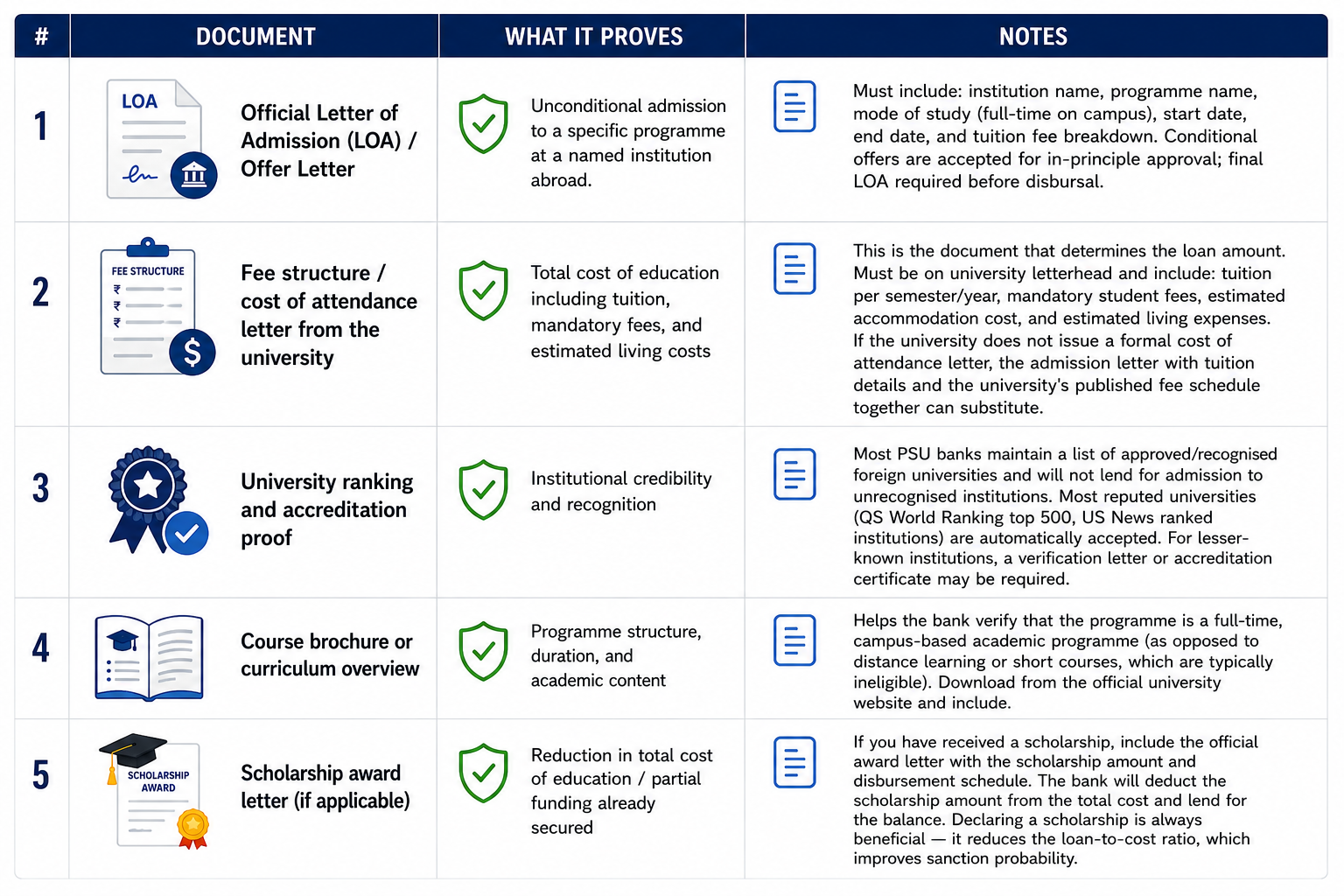

Category 4 — University and Course Documents

For all loans for overseas study, lenders assess not just the student and co-applicant — they assess the institution and programme. Banks want to confirm that the institution is recognised, the course is eligible under education loan guidelines, and the total cost of education is documented accurately. The following documents establish this:

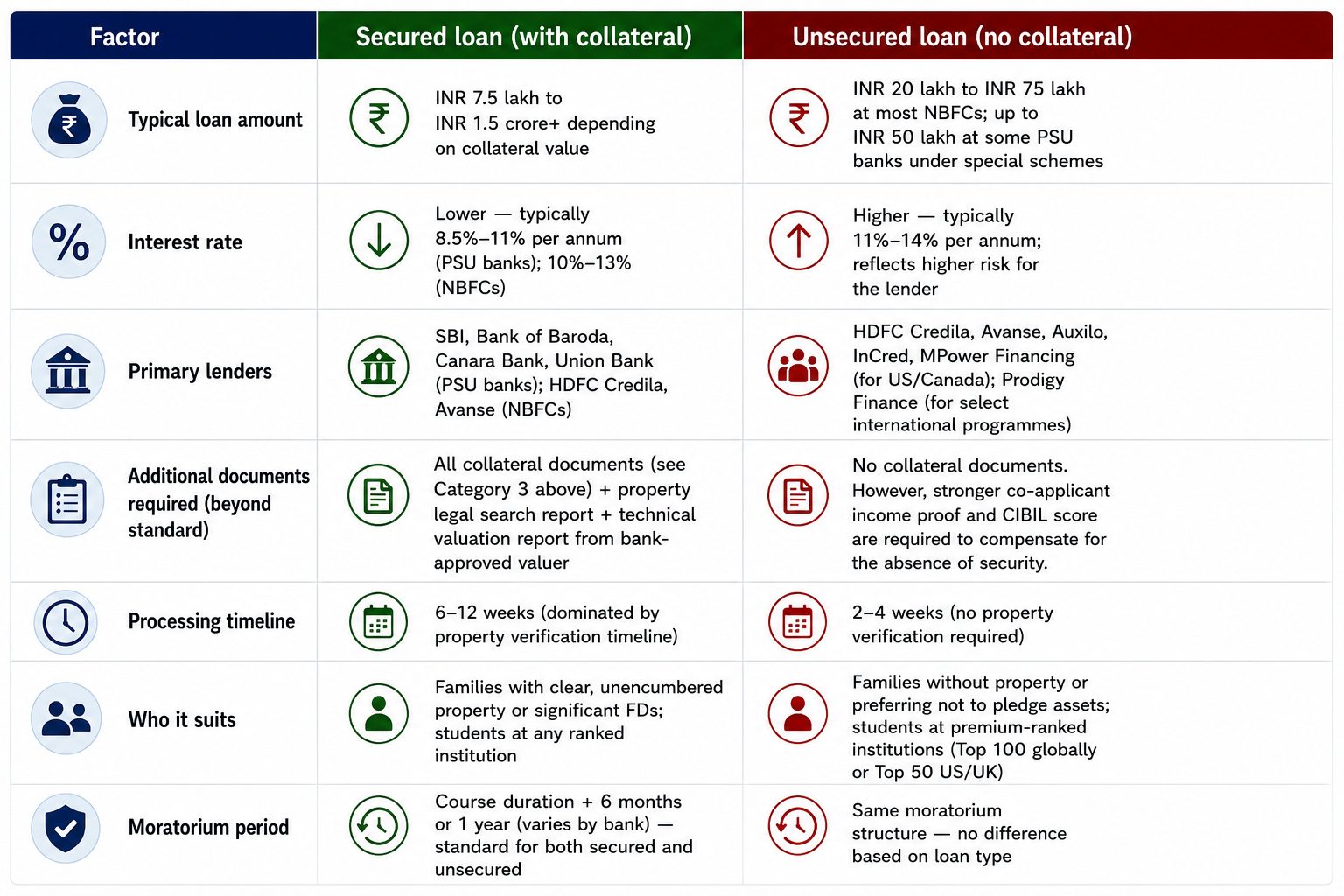

Secured vs. Unsecured Education Loans — Document Differences

The documentation requirements for a study loan for abroad differ significantly depending on whether the loan is secured (with collateral) or unsecured (without collateral). Understanding which loan type you are applying for — and which lenders offer which structure — determines the documentation path:

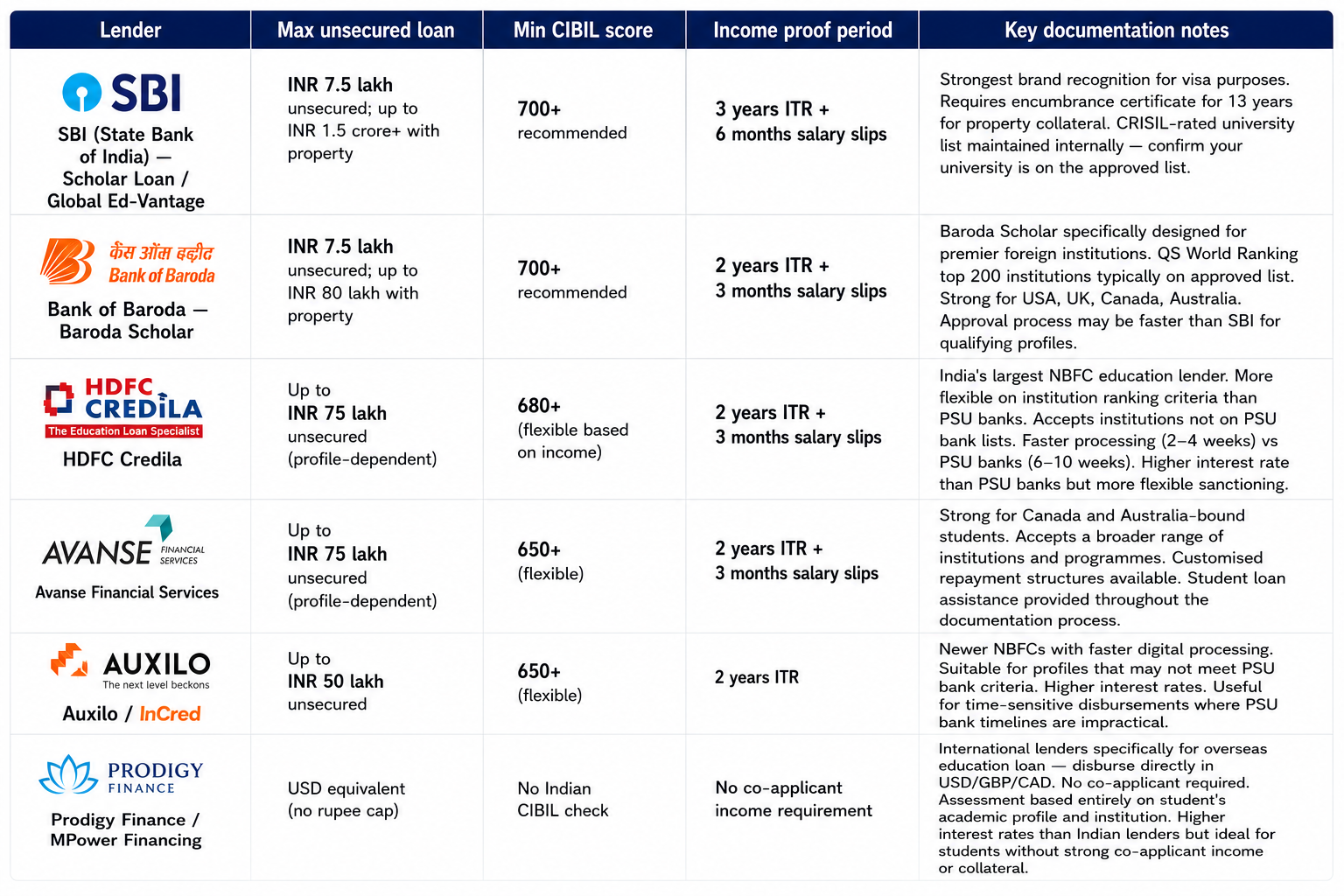

Major Indian Lenders — Document Requirements Compared

While the core documentation framework is consistent, different lenders have specific additional requirements or thresholds for education loan for overseas education. Here is how the major lenders compare:

Education Loan Application Timeline — When to Prepare What

The biggest mistake Indian students make when applying for student loans for overseas study is starting the loan process too late. A typical secured education loan (with property collateral) takes 8–12 weeks from application to disbursal. An unsecured loan from an NBFC takes 3–5 weeks. Here is the recommended timeline:

- 6–8 months before programme start: Check co-applicant's CIBIL score and address any issues. Identify collateral if applicable. Begin gathering financial documents (ITR, bank statements, business documents).

- 4–6 months before programme start: Shortlist lenders and loan products. Compare interest rates, processing fees, and repayment terms. If using property as collateral, initiate title search and encumbrance certificate process — these take time.

- 3–4 months before programme start: Receive offer letter / LOA from university. Submit loan application immediately. Do not wait for the visa — the loan sanction letter from the bank is a supporting document for many visa applications, including Canada and UK.

- 2–3 months before programme start: Respond to any bank queries or additional document requests promptly. Attend property valuation (if applicable). Receive loan sanction letter.

- 4–6 weeks before programme start: Complete loan agreement and documentation. Arrange first disbursement — typically the tuition fee for the first semester/year, disbursed directly to the university's bank account.

- After arrival abroad: Subsequent disbursements are typically triggered by submission of university fee receipts and living expense requests. Maintain contact with the lender's disbursement team for smooth follow-up disbursals.

✅ The loan sanction letter is a visa document — get it early. For Canada, UK, and Australia study visa applications, the education loan sanction letter from a recognised Indian bank or NBFC is accepted as financial proof by the respective immigration authorities. This means the loan sanction letter can replace the requirement to show liquid funds in your bank account. Get the sanction letter at least 6–8 weeks before your visa application date to ensure you have it ready when needed. Student loan assistance from a counsellor familiar with both the loan and visa process can coordinate these timelines effectively.

Frequently Asked Questions

Can I get an education loan for abroad studies without collateral?

Yes — multiple Indian NBFCs and some PSU bank special schemes offer education loan for abroad studies without collateral. HDFC Credila, Avanse, Auxilo, and InCred are the primary NBFCs offering unsecured loans up to INR 50–75 lakh based on the student's academic profile and the institution's credibility. PSU banks offer unsecured loans up to INR 7.5 lakh without collateral under the standard IBA model scheme. International lenders such as Prodigy Finance and MPower Financing require no collateral and no co-applicant — but interest rates are significantly higher. The key trade-off: no collateral means higher interest rate and more rigorous assessment of co-applicant income and CIBIL score.

What is the processing fee for an education loan for overseas studies?

Processing fees for education loan for overseas studies vary by lender: SBI charges no processing fee for most education loans; Bank of Baroda charges 1% of the loan amount; most NBFCs charge 0.5%–2% of the loan amount as a one-time processing fee. Some NBFCs also charge a documentation fee and a valuation fee (for property collateral). Always ask for a complete list of all charges — not just the interest rate — before selecting a lender.

Do I need education loan assistance or can I apply myself?

You can apply directly to any bank or NBFC for an education abroad loan — there is no requirement to use a third party. However, education loan assistance from an experienced counsellor adds value in specific ways: comparing lenders and negotiating interest rates, identifying the fastest documentation path for your specific profile, coordinating the loan sanction timeline with your visa application timeline, and navigating PSU bank processes that can be complex and time-consuming without guidance. Student loan assistance is particularly useful for profiles that do not fit the standard mould — for example, self-employed co-applicants with complex business structures, or applicants whose preferred institution is not on the standard PSU bank approved list.

Can the loan sanction letter be used as financial proof for a study visa?

Yes — for most major study destinations. For Canada (IRCC), the UK (UKVI), and Australia (Department of Home Affairs), a loan sanction letter from a recognised Indian scheduled bank or NBFC is accepted as financial proof for the student education loan for study abroad visa application, in place of (or in addition to) liquid bank balance. The sanction letter must clearly state the sanctioned amount, the disbursement schedule, and the purpose (higher education abroad). This is one of the strongest advantages of an education loan over self-funding — it simultaneously finances the education and serves as documented financial proof for the visa.

What happens if my visa is rejected after the loan is sanctioned?

If your study visa is rejected after the overseas education loan is sanctioned but before any disbursement, you can request cancellation of the loan with no disbursement penalty — the loan simply does not disburse. If fees have already been paid to the university and partially disbursed from the loan, you will need to recover the fee from the university (most have refund policies for visa rejections) and repay the disbursed amount to the bank. Some NBFCs offer a brief moratorium on repayment in visa rejection cases — check your loan agreement for specific terms. This is an important scenario to discuss upfront when seeking student loan assistance, so you understand your options before the loan is disbursed.

Securing an education loan for study abroad is a process that rewards preparation. Every lender — from SBI to HDFC Credila to Prodigy Finance — is assessing the same fundamental question: can this student and their family repay this loan? The documents you submit are the only evidence the lender has to answer that question. A well-organised, complete, consistent, and clearly presented document file shortens processing time, improves sanction probability, and positions you to negotiate better terms.

Start your documentation 4–6 months before your programme start date. Check your co-applicant's CIBIL score early. Identify and prepare your collateral if applicable. Get your ITR, bank statements, and income documents in order. And when you have your university admission, move immediately — loan processing timelines are long, and visa application timelines do not wait.

Whether you need guidance on selecting the right lender, coordinating your loan and visa application timelines, or navigating the documentation process for a complex profile, education loan assistance from an experienced study abroad counsellor can make the difference between a smooth, timely loan sanction and an avoidable delay that costs you your university seat.

Related Articles

Common Student Visa Rejection Reasons and How to Avoid Them — Complete Guide for Indian Students 2026

Overseas Education Consultant vs Applying Directly: Which Is Better? An Honest Assessment for Indian Students 2026

Timeline for Applying to Scholarships: When to Start — Complete Guide for Indian Students 2026