Education Loan Approval Timeline

How Long Does It Take? Complete Guide for Indian Students 2026

Team Vidysea

June 1, 2026

The single most common reason Indian students miss their intended university intake is not a visa refusal or a rejected admission — it is an education loan for abroad that took longer than expected. A student who starts the study abroad loan process 4 weeks before their visa financial proof deadline and chose a PSU bank discovers, at week 3, that the property valuation is still pending and the sanction letter is not going to arrive in time.

The honest answer to 'how long does a student loan for abroad take?' is: 5–8 working days for the fastest NBFC option on a no-collateral loan for a strong profile with complete documents, and 15–30 working days for a PSU bank collateral loan. The difference is not just the lender — it is the stage that takes longest, which differs between lender types, and the document gaps that create back-and-forth delays regardless of which lender you choose.

This guide breaks down the international education loan approval timeline stage by stage — by lender type, with the specific delay cause at each stage — and gives you a 10-point checklist of actions that can cut your international student loan processing time by 3–10 business days. If you need a quick student loan for a visa deadline that is already close, the scenarios table at the end maps your specific situation to the realistic timeline and the exact actions required.

The fastest documented study abroad loan approval: 5 business days

Under optimal conditions — no-collateral NBFC (Auxilo or InCred), complete documents submitted on Day 1, co-applicant CIBIL above 750, income clearly above lender threshold, university on approved list, application submitted Monday — Auxilo and InCred have sanctioned study abroad loans in 5 business days. This is not the median — the median NBFC timeline is 7–10 working days. But it is achievable for the right profile with the right preparation. The 10-point accelerator checklist in this guide is how you make your profile as close to 'optimal conditions' as possible.

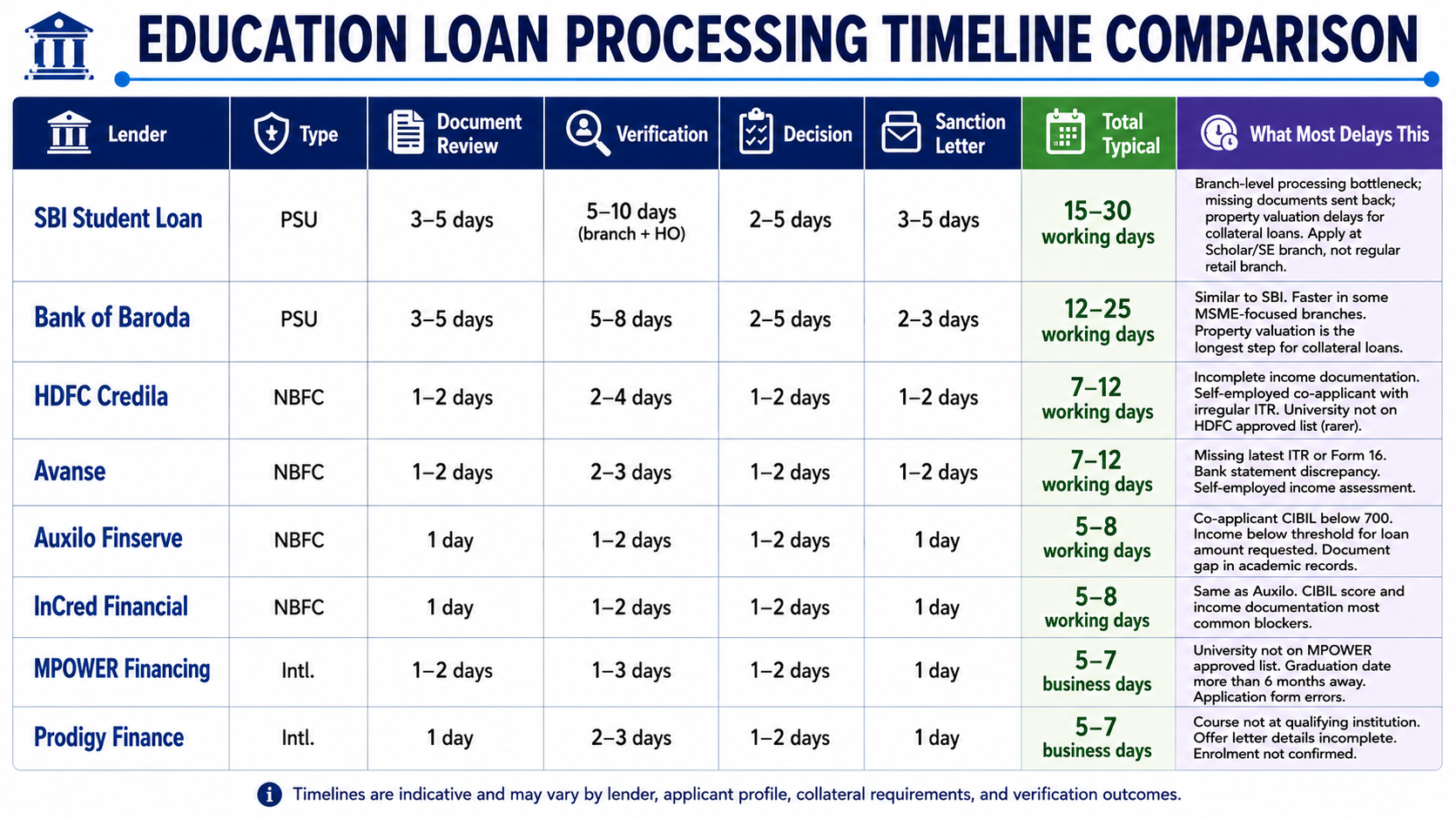

Education Loan for Abroad — Timeline by Lender 2026

This is the complete breakdown of study abroad student loan approval timelines across every major Indian and international lender. The 'total typical' column reflects complete-documents-submitted-on-Day-1 timelines — not the median which includes document delays:

The row colours tell the story at a glance

Green rows = 5–8 working days (Auxilo, InCred, MPOWER, Prodigy). Teal rows = 7–12 working days (HDFC Credila, Avanse). Amber rows = 12–30 working days (PSU banks). The colour reflects the 'total typical' column — designed so students can immediately identify which lender tier matches their available timeline. If your visa deadline is in 4 weeks: look at green and teal. If 8+ weeks: amber PSU bank rows become viable.

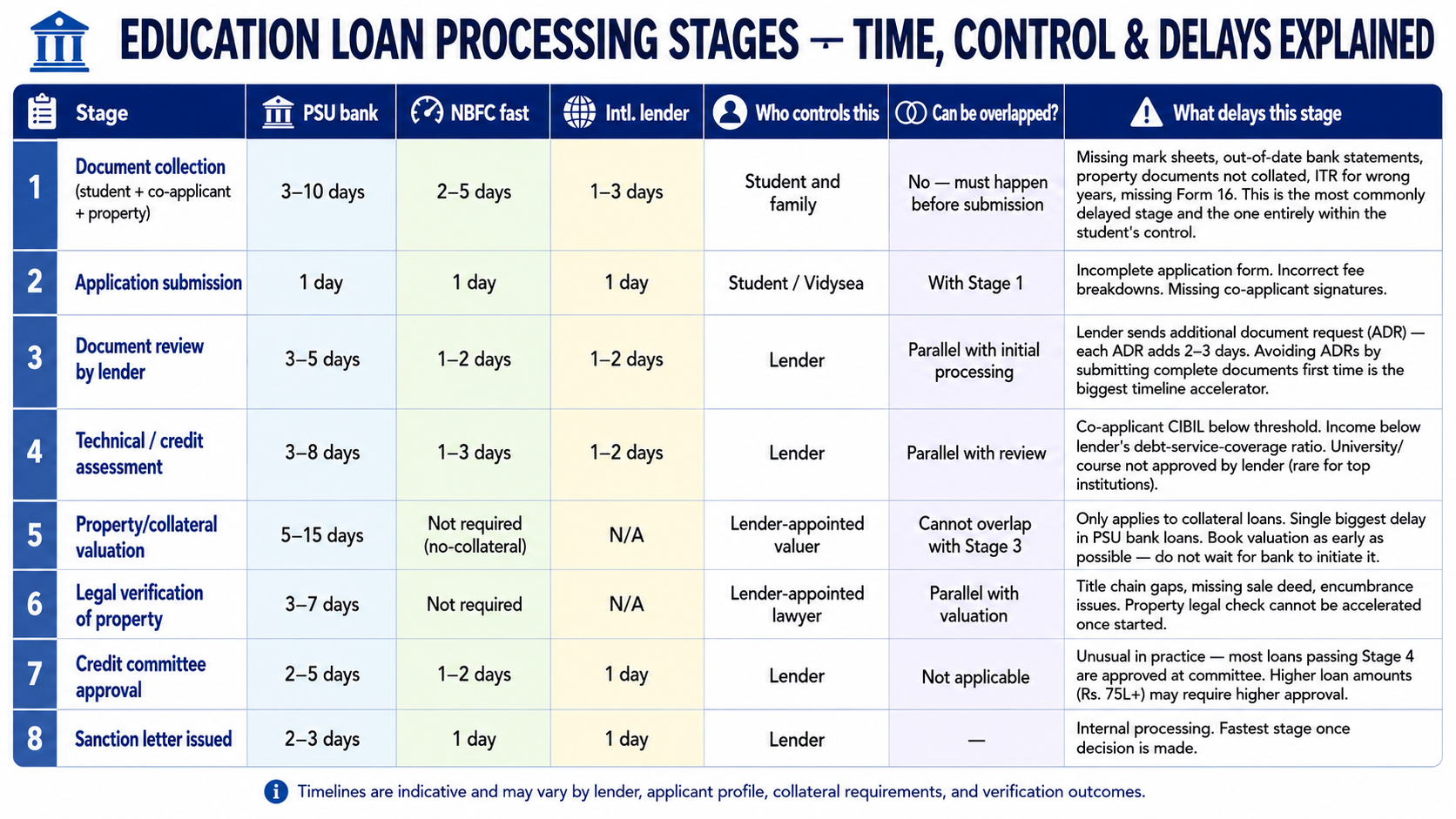

Stage-by-Stage: Where the Time Actually Goes

Most students think the international education loan delay happens at 'the bank taking long to decide.' In reality, the delay is usually at a specific stage — and usually one that the student or family could have accelerated. Here is the honest breakdown:

Stage 1 (document collection) is the most delayed stage — and it is entirely in your control

The most common reason a 7-day NBFC loan takes 3 weeks is that the student takes 10 days to collect documents. Mark sheets from a university that requires written requests. Property documents that are with a relative in another city. Form 16 for the co-applicant that needs to be requested from their employer. None of these take long to do once you know you need them. The 10-point checklist in the next section lists every document you should have ready before contacting any lender — so Day 1 of your application is a real Day 1.

The 5 Most Common Reasons Study Abroad Loans Take Longer Than Expected

1. Co-applicant CIBIL score below threshold — not discovered until after applying

Most NBFC lenders require a co-applicant CIBIL score above 700–720 for no-collateral study abroad loans. A score below this causes immediate rejection or a referral to a higher-rate product. Discovering this after a loan application has been submitted means: (a) a hard credit enquiry has been used up and (b) the application timeline starts over with a different lender. Check the co-applicant's CIBIL score before applying, not after. CIBIL scores can be checked free once per year on CIBIL.com. Any score below 720 should be investigated and addressed before applying — even a 30-day delay to close an outstanding credit card balance can improve a borderline score.

2. Missing or incorrect income documentation

For salaried co-applicants: the standard requirement is 3 years of ITR + latest 3 months' salary slips + Form 16. The most common gaps: ITR for the wrong assessment year (AY 2024–25, not AY 2023–24), salary slips not matching the bank statement salary credits, Form 16 not yet issued for the current financial year (relevant April–June applications). For self-employed co-applicants: the CA-certified computation of income and profit and loss account must reflect the income level claimed. A self-employed co-applicant claiming Rs. 15L annual income without consistent bank credits supporting that figure triggers immediate ADR.

3. Property valuation delay for collateral loans

PSU bank collateral loans require a bank-appointed valuer to physically inspect and value the property. This step cannot be initiated until after the loan application is submitted and the bank has accepted the application. The valuer's appointment typically takes 5–10 days; the valuation report another 3–5 days. The critical error: students wait for the bank to initiate valuation. The correct approach: ask the bank on Day 1 of the application who the approved valuer is, contact them directly, and request the earliest available appointment. This saves 5–8 days.

4. Additional document requests (ADRs) handled slowly

Every additional document request from a lender pauses the processing clock. A 2-document ADR issued on Tuesday that is not responded to until the following Monday adds 5 working days to the timeline. Designate one family member as the loan contact who monitors emails and phone calls from the lender daily and responds within 24 hours. ADR response speed is the single most actionable timeline variable that students underestimate — because most families assume the lender is the slow party, when often the delay is on the applicant side.

5. Waiting for unconditional admission before starting the loan process

Many families wait until they have the unconditional admission offer letter before initiating the study abroad loan process. This is understandable but costly in timeline terms. The correct approach: start document collection and CIBIL check immediately on deciding which universities to apply to. Complete the pre-application preparation entirely. On the day the unconditional offer letter arrives, submit the loan application with all documents ready. This converts a 3-week document-collection delay into zero additional delay.

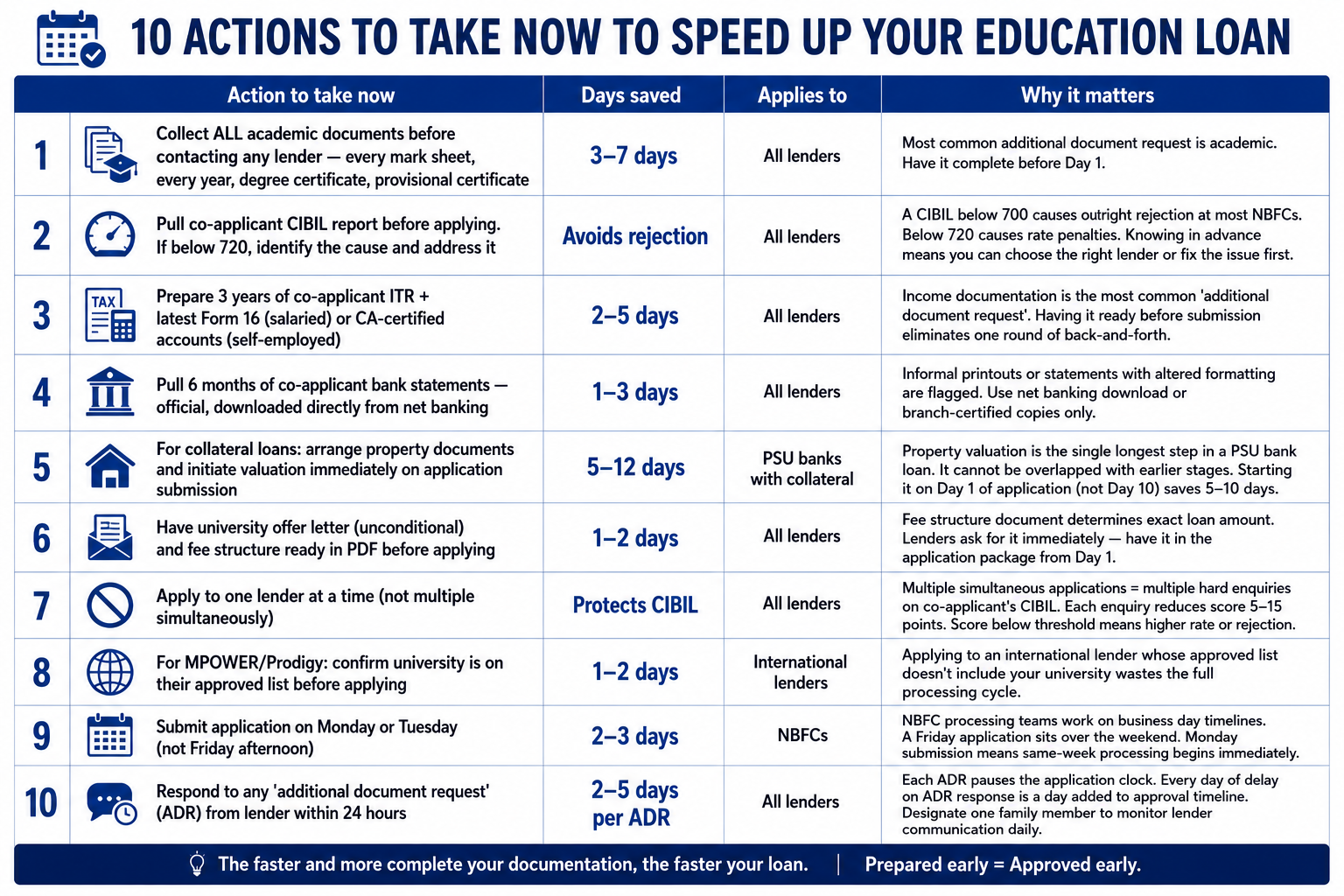

10-Point Checklist to Accelerate Your Study Abroad Loan Approval

Use this checklist to get as close as possible to optimal conditions before submitting your international education loan application:

The single action with the highest timeline impact

Of all 10 actions in the checklist, the one with the highest timeline impact for most families is: collect all academic documents before contacting any lender. This action takes 3–10 days and cannot be parallelised with lender processing. A student who contacts Vidysea or a lender on Monday and says 'I need my mark sheets from the university — I'll request them now' will not be ready to submit until next Wednesday at the earliest. A student who already has every academic document ready submits on Day 1 and begins lender processing that same week.

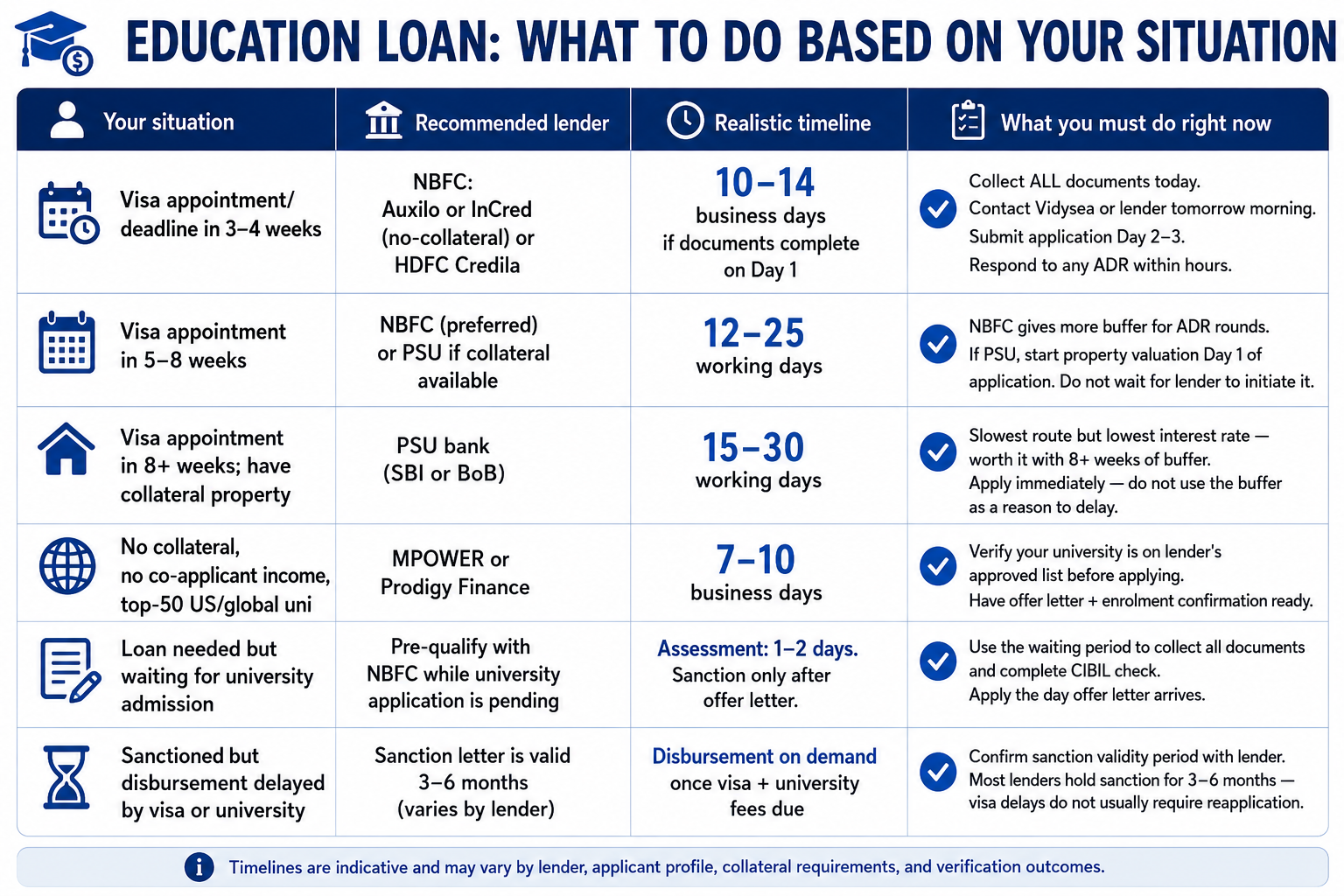

Timeline by Your Situation — What to Do Right Now

This table maps your specific deadline situation to the recommended study abroad student loan route and the exact first actions to take:

Sanction validity — what happens if disbursement is delayed after sanction

If your visa or university fees are delayed after the sanction letter is issued, most Indian lenders hold the sanction for 3–6 months (varies by lender — confirm at time of sanction). HDFC Credila: 6 months. Avanse: 4–6 months. Auxilo: 3–4 months. PSU banks: typically 3–4 months. If your timeline extends beyond the sanction validity, the lender will require updated bank statements and may need to reassess — but this is usually a 3–5 day refresh, not a full reapplication. The key: confirm sanction validity period explicitly at the time of signing the sanction letter.

Frequently Asked Questions

I applied to a PSU bank 3 weeks ago and still have no sanction. What should I do?

Three weeks with no sanction from a PSU bank typically means one of: (1) the application is stuck in the property valuation pipeline — call the bank manager and ask for the valuer's contact; follow up directly with the valuer; (2) there is an outstanding ADR that was sent by email but not noticed — check the email account associated with the application; (3) the application is in credit committee review for a higher loan amount. The correct action: call the branch manager directly, not the loan officer. Ask: 'At what stage is my application currently, and what is the expected date of the next action?' Get the answer in writing (email) and set a follow-up date 3 business days out.

Can I get a study abroad loan sanctioned before I have an admission offer?

Not a full sanction — but most lenders will conduct a pre-assessment or in-principle approval based on co-applicant income, CIBIL, and the university shortlist. This confirms the likely loan amount and rate you qualify for without issuing a binding sanction letter. This is worth doing: it confirms eligibility, identifies document gaps, and means the actual application takes 2–3 days from offer letter receipt instead of 10–15. Vidysea's loan session can generate this pre-assessment in 30 minutes.

Does taking a quick student loan (NBFC) now prevent me from refinancing to a lower-rate PSU bank loan later?

No — you can refinance an international education loan from an NBFC to a PSU bank after a period of timely EMI repayments. Most PSU banks have an education loan balance transfer product. The practical consideration: refinancing has a processing time (typically 3–4 weeks) and may involve a documentation refresh. Refinancing from NBFC to PSU in year 2 or 3 of your loan tenure, once you are employed and have Indian income, can reduce your interest rate significantly — sometimes by 2–3%. This is a valid strategy: quick student loan now for visa timeline, refinance later for rate optimisation.

The education loan for abroad timeline is not mysterious — it is a defined sequence of stages, each with a specific duration and a specific delay cause. The students who receive their study abroad loan sanction in time for their visa are not those who were lucky or who had a simpler application — they are the students who started document collection early, checked their co-applicant's CIBIL before applying, chose the right lender for their timeline, and responded to every ADR within 24 hours. Every day of delay in a quick student loan process is a day that was within someone's control to have shortened.

Related Articles

GMAT Preparation Guide for MBA Aspirants in India: How to Prepare for Abroad Studies — Complete 2026 Edition

HSBC vs Axis Bank vs HDFC Credila Which Is Better for Your Study Abroad Education Loan? — India 2026

Post-Study Work Visa Options by Country: Complete Comparison for Indian Students — 2026 Edition