How to Get a Study Abroad Loan for Canada PR Programs — Complete Guide for Indian Students 2026

Canada is the most popular study-to-PR destination for Indian students in 2026 — and for good reason. A master's degree at a Canadian university generates a 3-year Post-Graduation Work Permit (PGWP), which provides the 1 year of Canadian work experience needed to qualify for the Canadian Experience Class (CEC) under Express Entry. The full study-to-PR journey for most Indian students: 1–2 years studying + 1 year PGWP employment + 3–5 months Express Entry processing = permanent residency in 3–5 years from departure.

Team Vidysea

June 2, 2026

But the study abroad loan decision for Canada is different from the UK or Germany because the costs are higher, the programmes are structured differently, and the financial proof requirements for a Canadian study permit are specific in ways that most Indian loan sanction letters, by default, do not meet. An education loan for abroad to Canada that is correctly structured for IRCC financial proof is different from one that is not — and the difference determines whether the study permit is approved in the first attempt.

This guide covers everything an Indian student needs to know about international education loans for Canada PR programmes: which Canadian programmes deliver the strongest study-to-PR pathway, how to calculate the right loan amount for each, which lenders offer international student loans for Canada, how to structure financial proof for the IRCC study permit, and how to get a quick student loan if the study permit deadline is approaching.

What changed for Canada in 2024–2025 that affects the loan decision

Two material changes affect the Canada study-to-PR loan calculation: (1) Post-2024 PGWP cap for college (non-university) graduates — some college diploma programmes now generate only 1-year PGWP instead of 3. This affects the loan ROI calculation significantly. (2) Express Entry CEC continues to favour master's and higher-level graduates from Canadian DLIs, who receive 3-year PGWP regardless of the cap. If the goal is Canada PR, a university-level master's degree is the loan investment with the clearest pathway. Verify your specific programme's PGWP eligibility on the IRCC website before committing to a loan.

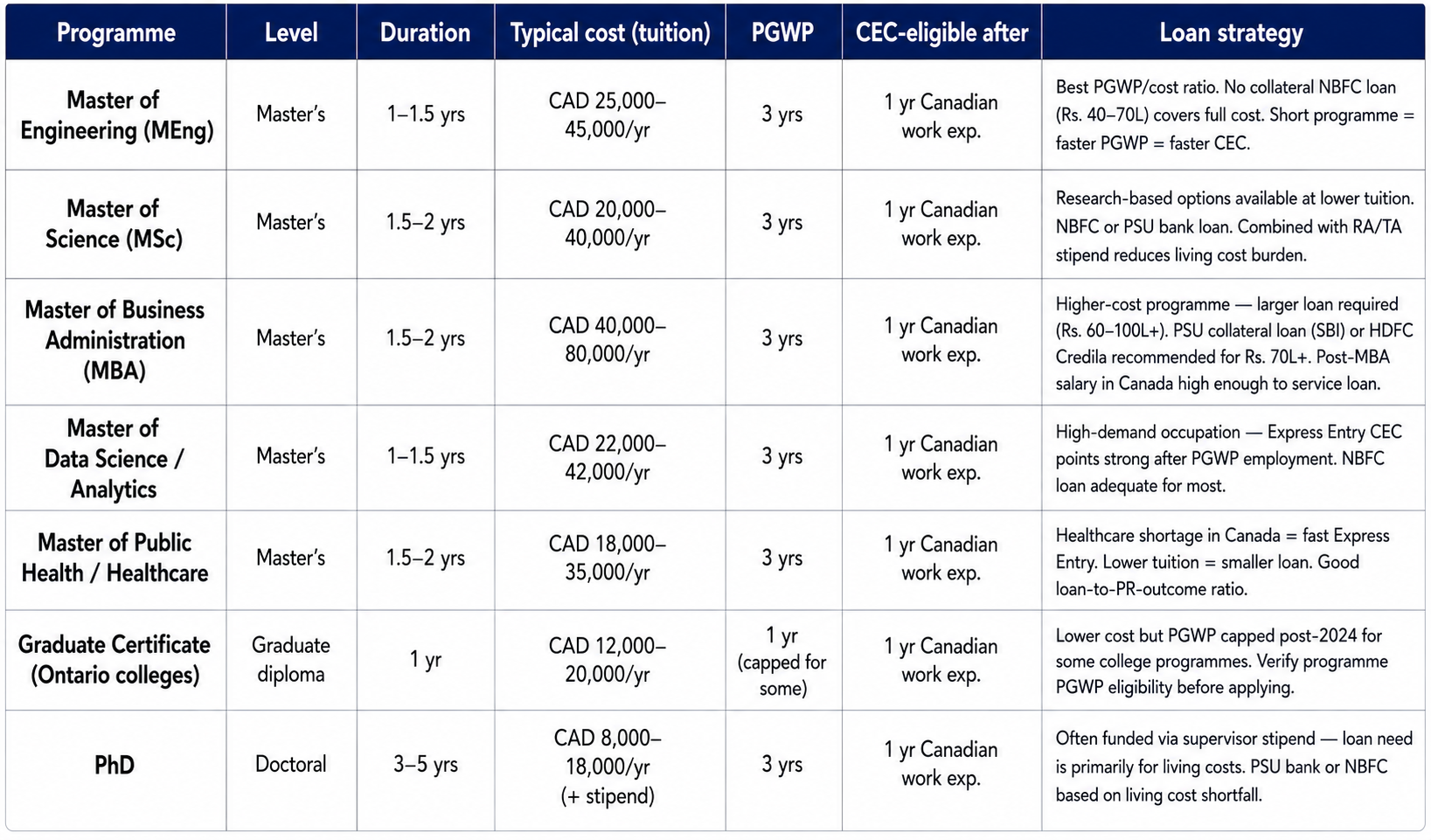

Canada PR Programmes — Which to Target and Why

Not every Canadian programme delivers an equivalent study-to-PR pathway. The choice of programme directly determines PGWP length, employment category, and Express Entry CEC eligibility. Here is how the major programme types compare from a study abroad loan for Canada PR investment perspective:

The 1-year master's programme is the best loan ROI for Canada PR

A 1-year Master of Engineering or Master of Data Science at a Canadian university generates a 3-year PGWP for approximately CAD 25,000–45,000 in tuition. Compare to a 2-year MBA at CAD 40,000–80,000/year. The 1-year option: lower total study abroad loan amount, faster graduation, faster PGWP commencement, earlier CEC eligibility. For Indian students whose primary goal is Canada PR — not the prestige of a 2-year MBA — the 1-year master's is the higher-ROI study abroad loan investment.

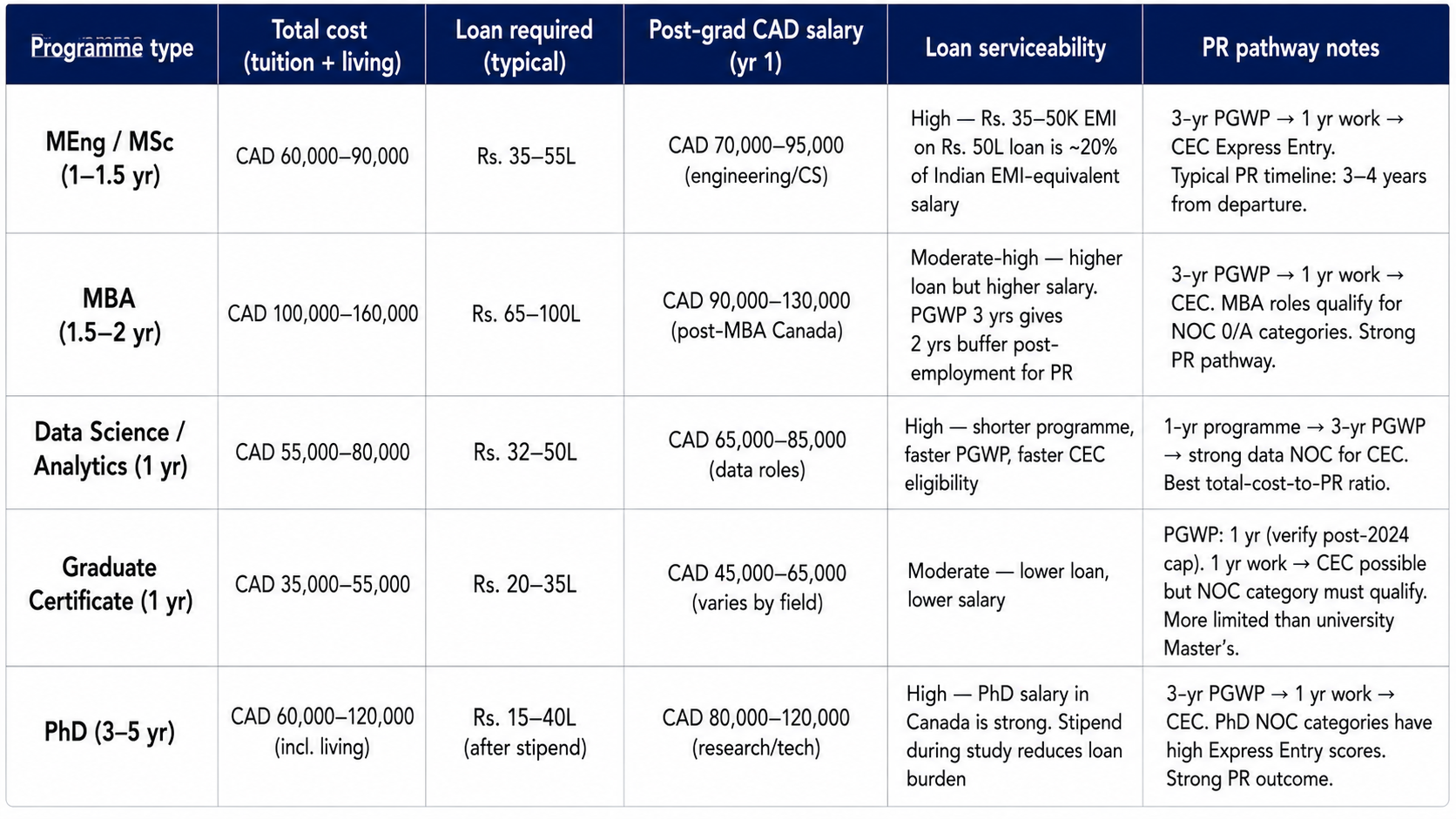

Study Abroad Loan to PR — Cost vs. Outcome Analysis

The international education loan for a Canada PR programme should be evaluated against the complete financial picture: total loan required, post-graduation Canadian salary, loan serviceability, and the total time to PR. This table maps those dimensions for each major programme type:

How to think about loan serviceability for Canada PR programmes

Indian students on PGWP in Canada typically earn CAD 60,000–95,000 in their first year of employment, depending on field. At CAD 70,000/year (Rs. 43L at current rates), an EMI of Rs. 45,000–55,000/month on a Rs. 50L study abroad loan is comfortably serviceable — approximately 13–15% of gross Indian-equivalent income. The moratorium period (during study + 6–12 months after graduation) means EMIs do not begin until PGWP employment is underway. For most Canada-STEM profiles, the study abroad loan is very comfortably serviceable from PGWP salary.

How to Calculate the Right Loan Amount for Canada

The study abroad loan for Canada needs to cover: tuition fees, living costs, health insurance (UHIP or provincial), travel, and an emergency buffer. Here is the calculation structure:

Tuition fees

Tuition for international students at Canadian universities ranges from CAD 18,000–80,000 per year depending on programme and university. Engineering and CS master's: CAD 20,000–45,000/year. MBA: CAD 40,000–80,000/year. Public health: CAD 18,000–35,000/year. Collect the exact fee schedule from your offer letter or the university's international student page — the loan amount must cover the full programme cost, not just year 1.

Living costs

IRCC minimum for living costs is CAD 10,000/year. Realistic budgets: Toronto/Vancouver: CAD 18,000–24,000/year (higher rent). Waterloo/Hamilton/Halifax: CAD 14,000–18,000/year. Smaller cities: CAD 12,000–16,000/year. The loan should include living costs at the realistic (not minimum) level — both for financial viability in Canada and for credible IRCC financial proof.

Health insurance and ancillary costs

University Health Insurance Plan (UHIP) or provincial insurance: CAD 600–1,200/year. Settlement costs (first month rent deposit, furniture): CAD 2,000–4,000. Travel: Rs. 80,000–1,20,000 return. Include these in the loan amount to avoid cash flow pressure on arrival.

Buffer for IRCC financial proof

Add CAD 5,000–10,000 above the calculated minimum to the loan amount. This buffer serves two purposes: (1) it creates the impression of a well-resourced student to the IRCC officer assessing the study permit; (2) it provides genuine financial security for the first semester in Canada before any part-time income starts.

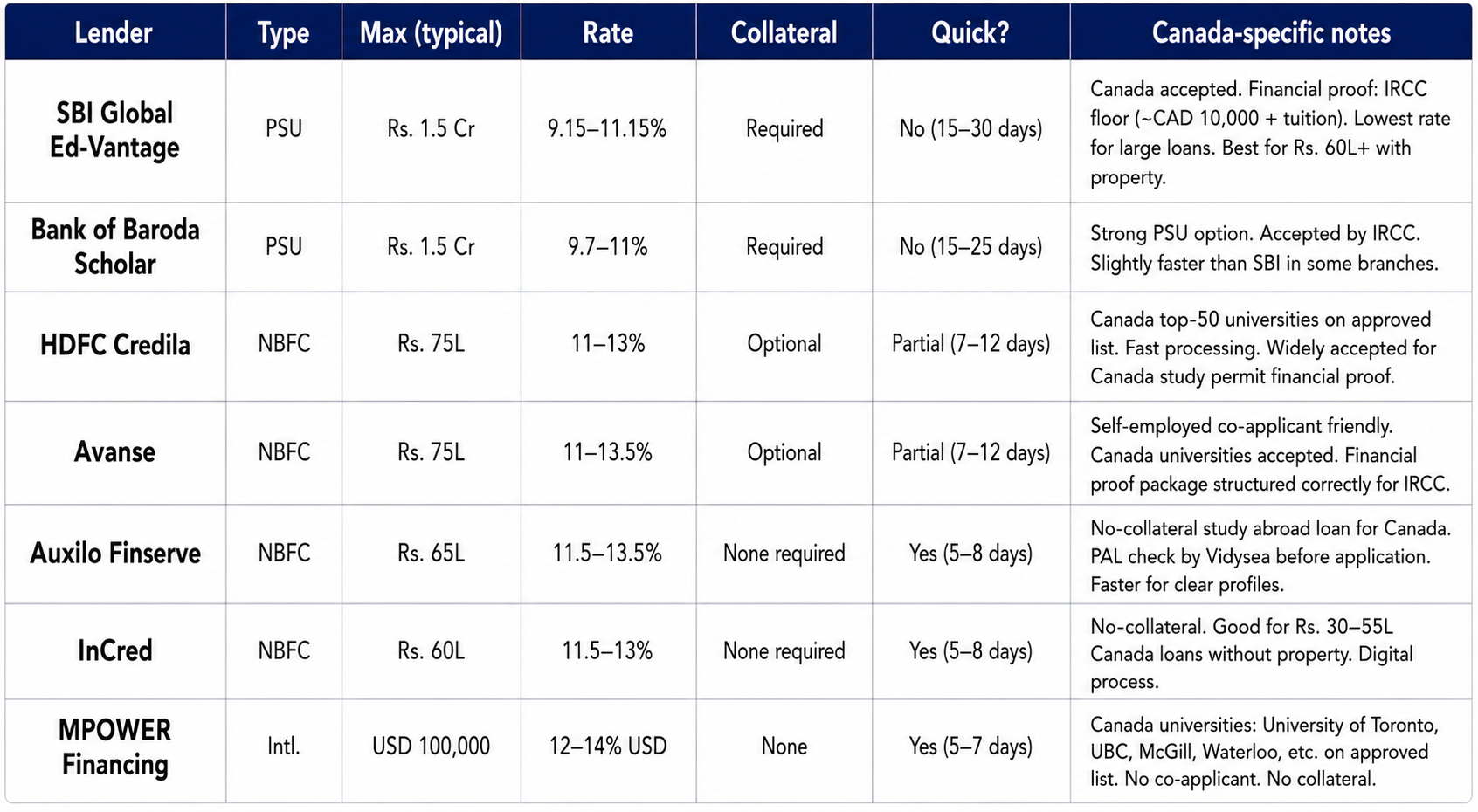

Best International Education Loan Lenders for Canada 2026

Not all international student loan lenders in India cover Canadian institutions equally. Here is the complete picture of which lenders best serve education loans for abroad to Canada:

PGWP cap for college programmes — check before taking an international education loan

Indian students taking education loans for abroad to Canadian colleges (not universities) need to verify that their specific programme generates a 3-year PGWP before the loan is committed. Post-2024 IRCC changes mean some college diploma programmes generate only 1-year PGWP. A 1-year PGWP significantly limits CEC Express Entry eligibility. Vidysea verifies PGWP eligibility for every Canada programme before advising on the loan structure.

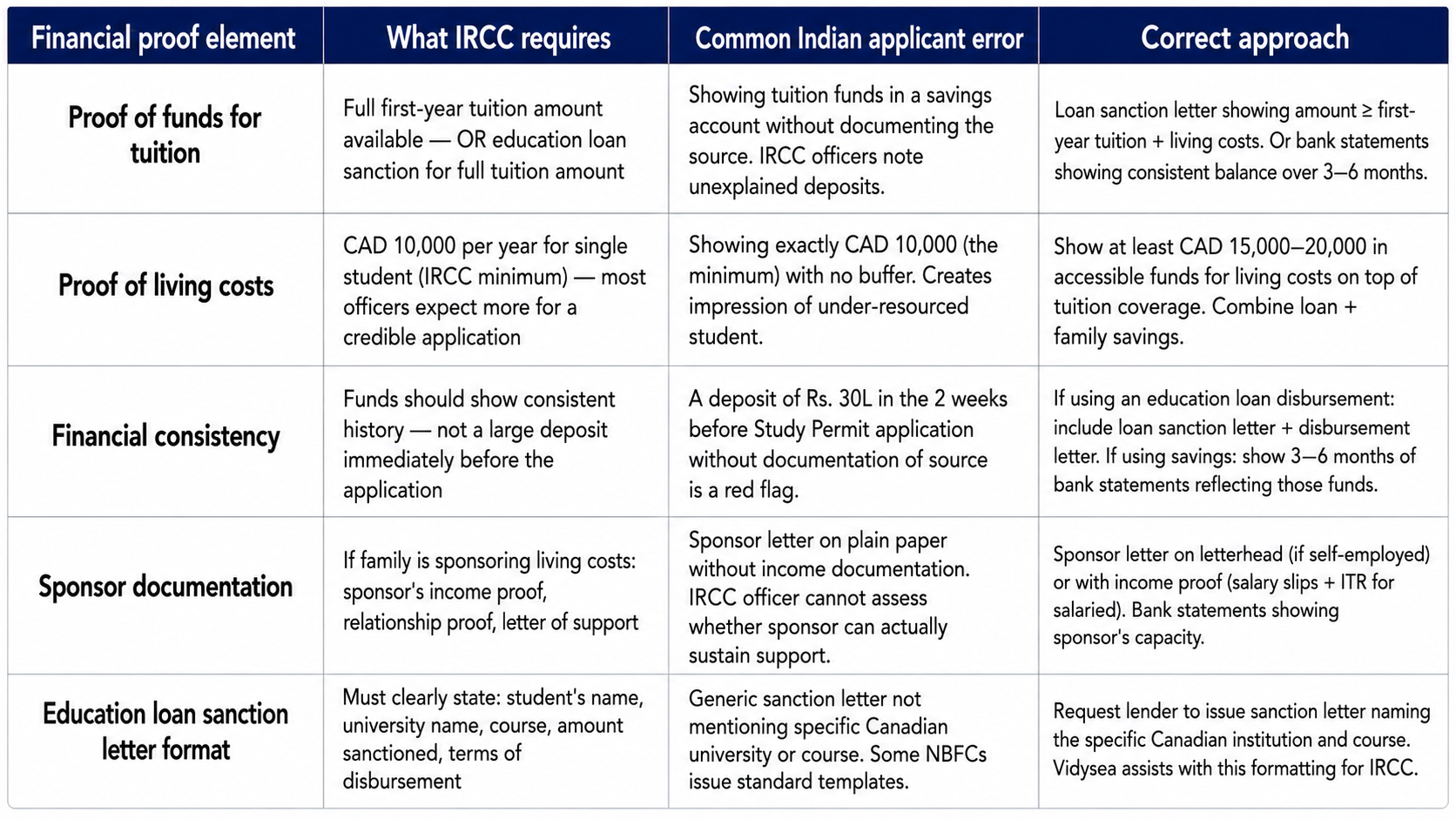

Financial Proof for Canada Study Permit — What IRCC Requires

The Canadian study permit financial proof requirement is less prescriptive than the UK (28-day rule) or Germany (Sperrkonto) but more holistically assessed. IRCC officers look for evidence that you can genuinely afford the full programme — tuition and living costs — without working illegally or abandoning your studies. Your study abroad loan documentation must be structured to demonstrate this clearly:

The combination that works best for Canada study permit financial proof

The most commonly approved financial proof combination for Indian students applying for a Canadian study permit: Education loan sanction letter (naming the specific Canadian university and course, showing full programme amount) + 3–6 months of co-applicant bank statements showing consistent balance + ITR of co-applicant for last 2 years. This combination demonstrates both documented loan capacity and underlying family financial stability — the two things IRCC officers look for from Indian applicants.

Quick Student Loan for Canada Study Permit Deadline

If you have received your Canadian university offer letter and have a study permit application deadline approaching, here is the fastest realistic path to a quick student loan for Canada:

- Day 1: Contact Vidysea or NBFC lender. Confirm co-applicant CIBIL above 700. Confirm university is on lender's approved list (all major Canadian DLIs are on HDFC Credila, Avanse, Auxilo, InCred approved lists).

- Day 1–2: Collect complete documents — co-applicant ITR (3 years), Form 16, 6-month bank statements, academic documents, university offer letter with fee schedule, passport copies.

- Day 3: Submit application to NBFC. For Auxilo or InCred: no-collateral loan up to Rs. 65L, processing in 5–8 working days for complete applications.

- Day 8–10: Sanction letter issued. Request lender to name the specific Canadian university and programme on the sanction letter (required for IRCC).

- Day 10–12: Combine sanction letter with co-applicant bank statements and ITR into IRCC financial proof package. Submit study permit application.

For students with no collateral and a Rs. 20–60L loan requirement: MPOWER Financing (if university is on their Canada list) processes in 5–7 business days with no co-applicant and no collateral. For students needing Rs. 60–100L+ for an MBA: HDFC Credila or SBI Global Ed-Vantage — HDFC Credila in 7–12 days, SBI in 15–30 days. Budget accordingly based on your MBA programme cost and study permit deadline.

Planning the Loan Around the Full Canada PR Journey

The international education loan for a Canada PR programme should be structured with the full 5-year financial journey in mind — not just the 1–2 years of study:

- Moratorium period: most Indian lenders allow a moratorium covering study duration + 6–12 months after graduation. On a 1-year master's with 12-month moratorium, first EMI falls ~24 months after disbursement — typically when PGWP employment in Canada is already underway.

- EMI serviceability in Canada: an EMI of Rs. 45,000/month (~CAD 730) on a Rs. 50L loan is approximately 12–15% of a typical PGWP-employed Indian student's gross Canadian salary. Comfortably serviceable for most STEM fields.

- Pre-payment from PGWP salary: Canadian employment income is strong relative to Indian EMI levels. Most students on PGWP can make additional principal payments from salary — reducing total interest cost significantly over the loan tenure.

- TCS on international remittances: 0.5% TCS applies on education loan-related remittances above Rs. 7L per financial year. Refundable via ITR. Plan disbursement across financial years (April–March) to minimise cash flow impact.

- PR income uplift: once Canadian PR is confirmed (typically 3–5 years from departure), income and employment stability in Canada improves significantly. The study abroad loan EMI becomes an increasingly small proportion of total income over the repayment tenure.

Frequently Asked Questions

Can I take an education loan for abroad to a Canadian college (not university)?

Yes — most lenders cover Canadian colleges (IRCC-designated DLIs). The loan eligibility and rate are similar to university programmes. The critical difference is the PGWP duration post-2024: some college programmes now generate only 1-year PGWP. Before taking a study abroad loan for a Canadian college programme, confirm the specific programme's PGWP eligibility on the IRCC website. A 1-year PGWP significantly limits CEC Express Entry options compared to the 3-year PGWP available to university master's graduates.

How does an Indian education loan affect my Canadian work permit or PR application?

Having an Indian study abroad loan does not affect your Canadian work permit (PGWP) or PR application in any way. IRCC assesses work permit eligibility based on your Canadian study record and programme. Express Entry CEC assesses Canadian work experience and language scores. Your Indian international education loan status is neither disclosed to IRCC nor assessed by them. However, your ability to financially sustain yourself in Canada during the PGWP job search period (between graduation and first employment) matters — which is why having adequate financial buffer built into the original loan amount is important.

Is there a study abroad loan specifically for STEM or PR-pathway programmes in Canada?

No lender in India specifically designates a 'PR pathway loan' — the product is a standard international education loan or study abroad student loan. However, Vidysea's approach to Canada loan structuring specifically accounts for PR-pathway programme selection: we verify PGWP eligibility, confirm the NOC category for the occupation the programme leads to (to confirm Express Entry CEC viability), and structure the loan amount to cover the full 5-year journey — not just the study period. This is the planning intelligence that a bank's loan counter cannot provide.

A study abroad loan for a Canada PR programme is not just a financing decision — it is a 5-year life trajectory investment. The students who structure this correctly — right programme for PGWP length, right loan amount for genuine financial comfort in Canada, right lender for rate and timeline, right financial proof format for IRCC — arrive in Canada financially prepared, transition to employment under PGWP, and reach permanent residency on the 3–5 year timeline that makes Canada the most popular study-to-PR destination for Indian students. Every element of the international student loan decision compounds towards that outcome — or away from it.

Related Articles

Top Universities for Business Analytics in France 2026: Best Business Schools, Fees, Eligibility, Scholarships & Career Opportunities

Top Universities for MBA in France 2026: Best Business Schools, Fees, Eligibility, Careers & ROI

After MS Jobs in France: Career Opportunities, Salaries, Work Visa & PR Pathways