HSBC vs Axis Bank vs HDFC Credila Which Is Better for Your Study Abroad Education Loan? — India 2026

Three of the most commonly asked questions by Indian families applying for a study abroad student loan in 2026 involve these three names: HSBC, Axis Bank, and HDFC Credila. HSBC because it is an international bank and families assume global credibility means better visa financial proof. Axis Bank because many urban Indian families already bank there. HDFC Credila because it appears in almost every online search for education loan for abroad and has processed more study abroad loans than any other single NBFC in India.

Team Vidysea

June 3, 2026

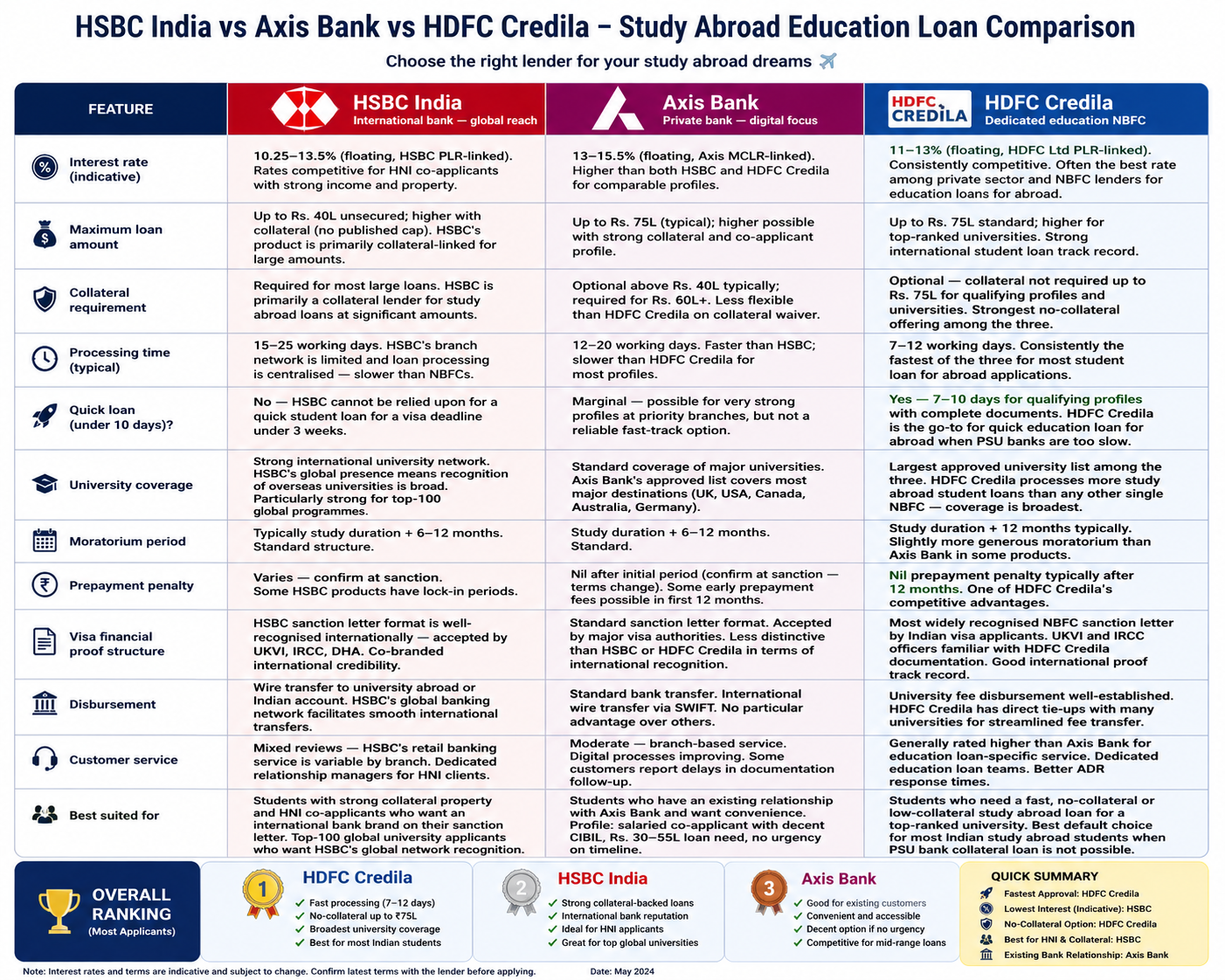

The honest answer to 'which is better?' is: HDFC Credila wins for most Indian students on aggregate — faster processing, competitive rate, strongest no-collateral student loan for abroad offering, and the broadest university coverage. HSBC is competitive for students with strong collateral and HNI co-applicants who want an international bank's brand on their visa financial proof document. Axis Bank is the weakest of the three — higher rate than both HSBC and HDFC Credila for comparable profiles, slower than HDFC Credila, and without a particular advantage that compensates for either shortcoming.

This guide provides the complete three-way comparison across 12 dimensions — with a scored comparison table, a 'who should choose which' decision matrix, and deep dives on the specific scenarios where each lender has a genuine advantage. If you need a quick student loan for a visa deadline, the processing speed analysis is in the second section. If you are comparing for a large international education loan with collateral, the rate analysis is covered in the deep-dive section.

Important: HDFC Credila is not HDFC Bank

HDFC Credila is an NBFC (Non-Banking Financial Company) that specialises in education loans. It is separate from HDFC Bank (a commercial bank) and HDFC Ltd (the housing finance company). When Indian families search for 'HDFC education loan for abroad,' they may find HDFC Bank, HDFC Credila, or both. This blog covers HDFC Credila — the dedicated education loan NBFC — not HDFC Bank's education loan product. HDFC Credila has consistently better terms for international student loans than HDFC Bank's standard product.

Complete 12-Dimension Comparison — HSBC vs Axis Bank vs HDFC Credila

This is the full head-to-head on every dimension that matters for choosing a study abroad loan lender:

The dimension that decides the comparison for most students: processing speed

For students with a visa deadline under 6 weeks, processing speed is the deciding dimension — and HDFC Credila wins definitively at 7–12 days vs. HSBC at 15–25 days. For students with 8+ weeks and strong collateral, the rate comparison (HSBC 10.25–11.5% vs. HDFC Credila 11–12% on collateral profiles) makes HSBC worth the additional processing time. Axis Bank is not competitive on either dimension — it is slower than HDFC Credila and more expensive than both HSBC and HDFC Credila for most profiles.

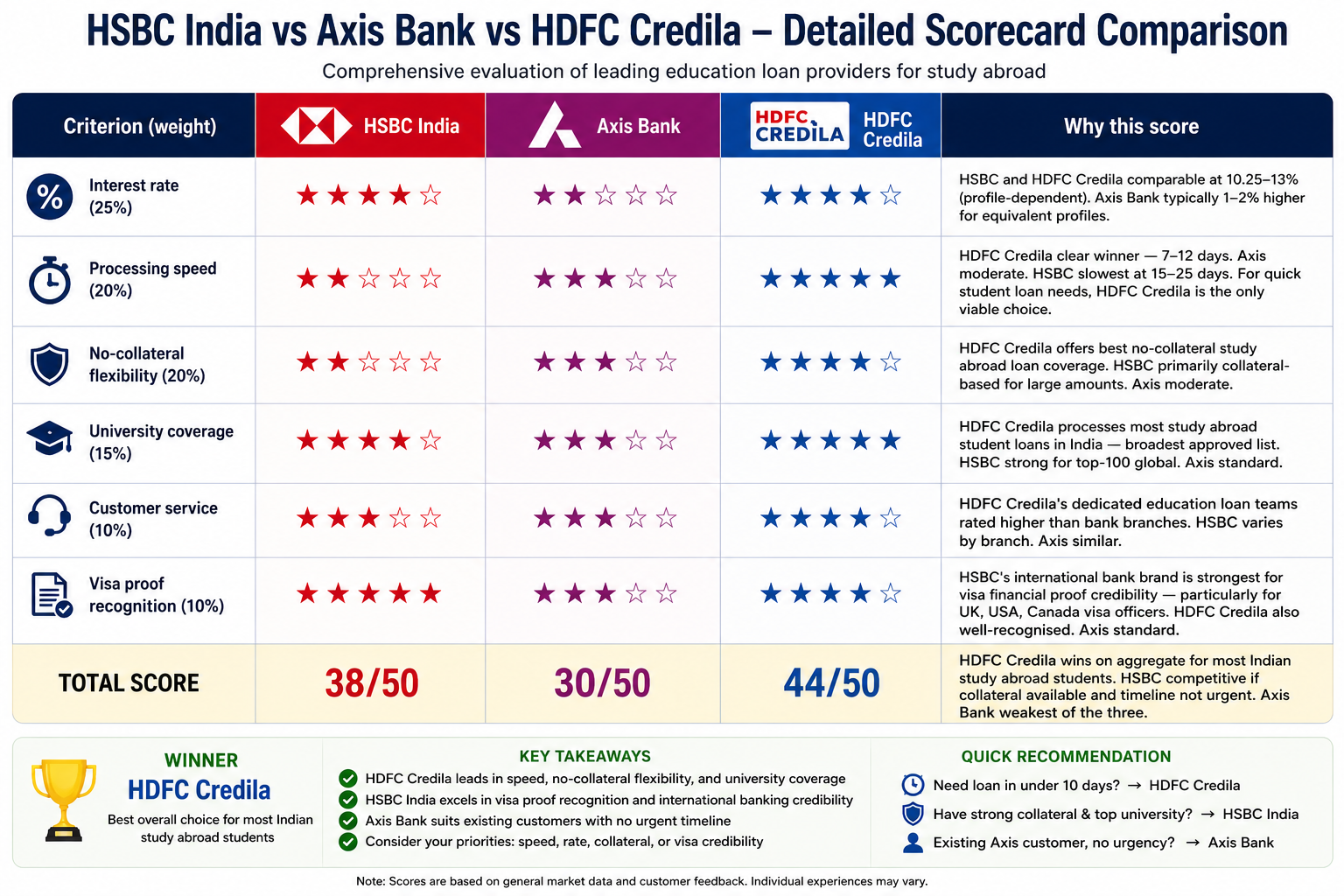

Weighted Scorecard — HSBC vs Axis Bank vs HDFC Credila

Scored out of 10 per criterion, weighted by importance for most Indian study abroad student loan applicants:

These scores reflect the typical Indian study abroad student profile — your situation may differ

The scorecard weights processing speed (20%) and no-collateral flexibility (20%) highly because most Indian study abroad students are working professionals or recent graduates without significant property assets and with visa timelines under 8 weeks. For a student with strong collateral, an HNI co-applicant, and 10+ weeks of timeline, the weights shift — and HSBC becomes more competitive relative to HDFC Credila. Use the 'who should choose which' table below to apply your specific profile.

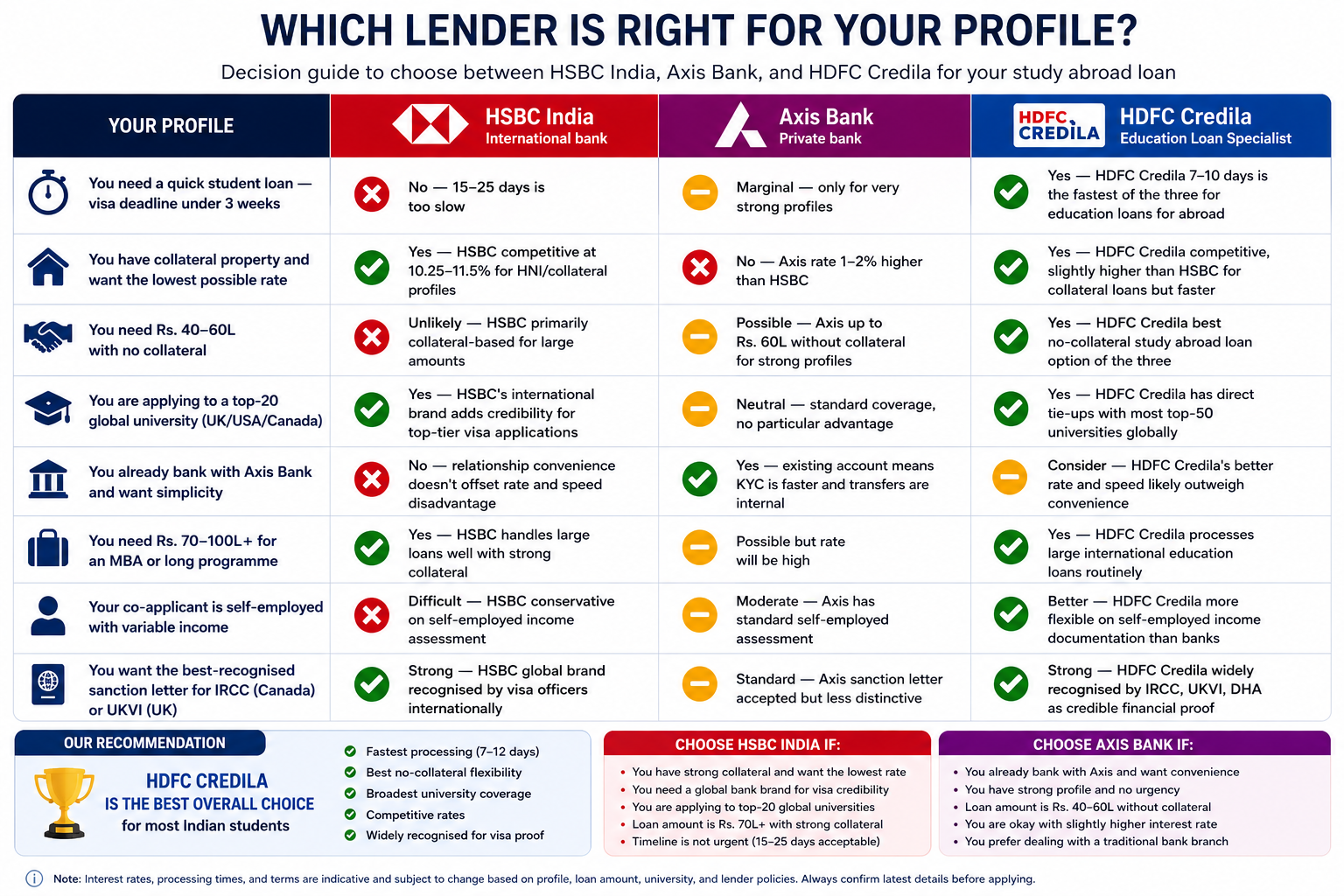

Who Should Choose Which? — Decision Matrix

The hybrid approach that beats all three individually

Students with a visa deadline under 3 weeks and a loan need above Rs. 65L should consider: HDFC Credila for the fast sanction letter (Rs. 65–75L, 7–12 days), while simultaneously initiating an SBI Global Ed-Vantage application for potential refinancing to the lower PSU rate after year 1. HDFC Credila now, SBI refinance later when there is no timeline pressure. This hybrid approach — quick student loan first, rate optimisation later — costs an additional 1.5–2% in interest for 12–18 months but saves the intake. Over a 10-year loan, that premium is modest against the cost of missing a semester.

Deep Dives — When Each Lender Has a Genuine Advantage

When HSBC India is the right choice

HSBC's genuine advantages for education loans for abroad are concentrated in a specific profile: strong collateral property, co-applicant with high income (Rs. 15L+ annual), and a top-50 global university application. In this profile, HSBC can offer rates in the 10.25–11.5% range that match or beat PSU banks on collateral loans — combined with faster processing than SBI and the prestige of an international bank sanction letter.

The HSBC sanction letter has one specific advantage that matters for UK Student visa applications: UKVI officers are familiar with HSBC globally and the international bank format carries implicit credibility. For an Indian student applying for a UK Student visa with HSBC as their international student loan provider, the sanction letter presentation is marginally stronger than an NBFC letter from an institution a UKVI officer may be less familiar with. This is a soft advantage but a real one at the margin.

- Choose HSBC if: you have strong collateral property + co-applicant income above Rs. 15L/year + applying to a top-50 global university + timeline of 6+ weeks.

- Do not choose HSBC if: you need a quick student loan in under 3 weeks, you have no collateral, or your co-applicant income is moderate.

When Axis Bank is the right choice

Axis Bank's education loan product is genuinely competitive in one scenario: students who already have a long-standing relationship with Axis Bank (savings, fixed deposits, existing loan), whose co-applicant income is clearly above threshold, and who want the convenience of managing everything within a single bank relationship. In this case, the KYC process is faster, account management is simpler, and the minor rate premium over HDFC Credila may be acceptable for convenience.

Outside this specific scenario, Axis Bank does not have a compelling advantage over HDFC Credila for a new study abroad student loan applicant. The rate is typically 1–2% higher, the processing is slower, and the no-collateral flexibility is weaker. Unless an existing Axis Bank relationship genuinely saves you significant time and complexity, HDFC Credila is the better choice for most new applicants.

- Choose Axis Bank if: you have an existing Axis Bank relationship + convenience matters + timeline is 4+ weeks + Rs. 30–55L loan need.

- Do not choose Axis Bank if: you are comparing fresh options, need the best rate, or have a visa deadline under 4 weeks.

When HDFC Credila is the right choice

HDFC Credila is the correct international education loan choice for the majority of Indian study abroad students in 2026. Three specific advantages make it the default recommendation for most profiles:

- Fastest processing (7–12 working days) — the most important variable for the majority of students who discover they need a loan 4–8 weeks before their visa appointment.

- Best no-collateral coverage — up to Rs. 75L without requiring property. Most Indian urban families applying for the first time do not have easily liquidatable property. HDFC Credila serves this profile better than HSBC or Axis Bank.

- Broadest university list — HDFC Credila has processed study abroad loans for students at virtually every ranked university globally. If your university is in the top 500, it is on their approved list.

The HDFC Credila quick student loan option — for students with CIBIL above 720 and clear income documentation — is one of the fastest unsecured international education loans available from any lender in India. The 7-day sanction is achievable for the right profile with complete documents on Day 1.

- Choose HDFC Credila if: you need fast processing + no/low collateral + Rs. 25–75L loan + any major ranked university globally.

What HSBC, Axis, and HDFC Credila Don't Cover — When to Look Elsewhere

These three lenders are not the right answer for every study abroad student loan profile. Here are the situations where other lenders are clearly better:

- For Rs. 15–30L loans at the lowest possible rate: SBI Scholar Loan or Bank of Baroda Baroda Vidya — PSU banks offer 9–11% for collateral loans, lower than all three lenders compared here. If timeline allows 4 weeks and collateral is available, PSU banks are cheaper.

- For Rs. 60–100L+ loans with property collateral: SBI Global Ed-Vantage (up to Rs. 1.5 Cr, 9.15–11.15%) is materially cheaper than HSBC, Axis, and HDFC Credila for large collateral loans. Rs. 8–15L saved in interest over 10 years on Rs. 70L+ justifies the slower processing.

- For students at top US/Canada/global universities without any Indian co-applicant: MPOWER Financing or Prodigy Finance — no co-applicant, no collateral, processed in 5–7 days. HSBC, Axis, and HDFC Credila all require an Indian co-applicant.

- For the fastest quick student loan in India (under 8 days): Auxilo Finserve and InCred Financial Services are faster than HDFC Credila for some no-collateral profiles, though HDFC Credila is comparable.

Frequently Asked Questions

Is HSBC's education loan rate actually better than HDFC Credila's?

For strong collateral profiles — property worth 1.5× the loan amount, co-applicant income above Rs. 15L/year, CIBIL above 750 — HSBC can price 0.5–1% lower than HDFC Credila on the base rate. On a Rs. 60L loan over 10 years, this saves approximately Rs. 3–6L in total interest. Whether that saving justifies HSBC's slower processing time (10–15 more working days) is a timeline-dependent decision. If you have 8+ weeks and a clean collateral profile, HSBC's rate can make it the better financial choice for a large international education loan.

Can I negotiate the interest rate with HDFC Credila?

Yes — HDFC Credila's stated rates are starting points for negotiation. Factors that improve negotiating position: CIBIL above 780, co-applicant income above Rs. 12L/year, university ranked in top 100 globally, clean credit history with no missed payments. A difference of 0.25–0.5% can typically be negotiated for a strong profile — which saves Rs. 1.5–3L on a Rs. 50L loan over 10 years. Vidysea's lender relationships mean we often negotiate rates on behalf of students that are not available to walk-in applicants.

Does Axis Bank's existing account relationship actually speed up the loan process?

Partially — existing KYC at Axis Bank means the customer identity verification step is faster (typically 1–2 days saved). However, Axis Bank's credit assessment and documentation review process is not meaningfully faster than an NBFC for a new loan applicant, even with an existing account. In practice, an Axis Bank existing customer gets a 12–18 working day timeline vs. a fresh applicant's 15–20 — not the step-change that many families expect. For a study abroad loan where 3 days saved matters, this marginal advantage does not change the overall recommendation.

The verdict for most Indian students applying for a study abroad student loan in 2026: HDFC Credila is the strongest default choice — fast, flexible on collateral, broad university coverage, and competitive rate. HSBC is the right choice specifically for large collateral loans where the rate saving over 10 years justifies the slower timeline. Axis Bank is the weakest of the three and should only be chosen when an existing relationship provides genuine operational convenience. And for students whose profile or loan size falls outside what all three cover — comparing SBI, Auxilo, MPOWER, and Prodigy Finance alongside these three is the complete loan strategy that Vidysea provides in every loan assessment session.

Related Articles

GMAT Preparation Guide for MBA Aspirants in India: How to Prepare for Abroad Studies — Complete 2026 Edition

Post-Study Work Visa Options by Country: Complete Comparison for Indian Students — 2026 Edition

Best Overseas Education Consultants in Noida 2026 — How to Choose the Right Consultant