Study Abroad Education Loan Process in India — Step by Step

For the majority of Indian students, securing an education loan for abroad is not a last resort — it is a deliberate financial strategy. An overseas education carries a real and significant cost: tuition fees at a UK or Australian university range from ₹25 to ₹80 lakhs for a Master's programme; a two-year US Master's at a mid-ranked university can cost ₹60–₹1.2 crores all-in when you include living expenses, travel, and health insurance. For most Indian families, this is not a cost that can be covered from savings alone. A well-structured study abroad student loan from a scheduled Indian bank or a reputable NBFC is how most successful Indian students fund their international education.

Team Vidysea

May 26, 2026

But the study abroad loan process in India is document-intensive, timeline-sensitive, and full of decisions that have long-term financial consequences — interest rate structures, collateral requirements, moratorium periods, disbursement processes, and the critical question of how your sanction letter will be assessed by the visa authority of your destination country. Getting these decisions right — before you apply, not after — is what this guide is about.

This guide covers the complete international education loan process for Indian students in 2025–2026: how to choose the right lender, the step-by-step application process, the complete document checklist, a comparison of secured vs. unsecured loans, country-specific financial proof requirements, and the most common mistakes that delay or derail loan applications. Whether you are applying for a student loan for abroad from SBI, HDFC Credila, Avanse, or any other lender, the framework in this guide applies.

📌 How to use this guide: If you already have your offer letter and need to apply immediately, go directly to the Step-by-Step Process section and the Document Checklist. If you are still deciding between lenders or between secured and unsecured loans, read the Lender Comparison and Secured vs. Unsecured sections first. The Country-Wise Financial Requirements section is essential reading before you submit your visa application.

Education Loan Lenders in India — Who to Consider

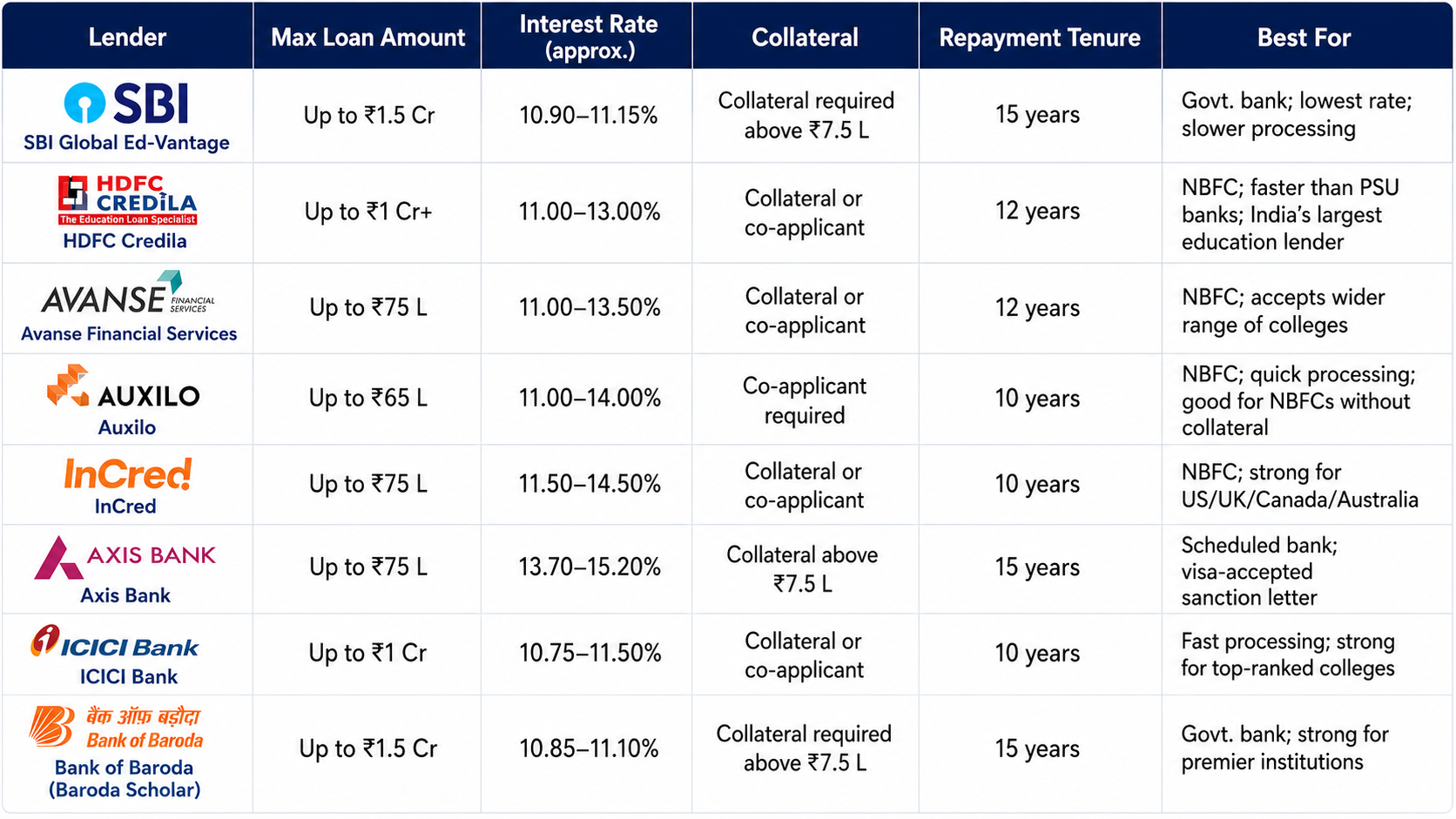

The international student loan market in India is served by three categories of lenders: public sector banks (government-owned banks such as SBI and Bank of Baroda), private sector scheduled banks (ICICI, Axis), and NBFCs — Non-Banking Financial Companies (HDFC Credila, Avanse, Auxilo, InCred). Each category has different strengths, and the right lender depends on your loan amount, collateral availability, destination country, and processing time requirement.

Public Sector Banks vs. NBFCs — The Core Trade-off

For most Indian students seeking a study abroad student loan, the primary choice is between a public sector bank and an NBFC. Here is the trade-off in plain terms:

- Public sector banks (SBI, Bank of Baroda) offer the lowest interest rates — typically 10.85–11.15% for overseas education loans — but have slower processing times (4–8 weeks), require branch visits, and have stricter eligibility criteria. Their sanction letters carry significant credibility with visa authorities, particularly for UK and Schengen visa applications.

- NBFCs (HDFC Credila, Avanse, Auxilo, InCred) process applications faster — sometimes in 2–3 weeks — accept applications online, have dedicated relationship managers, and are more flexible on collateral and eligibility. Their interest rates are higher (11.5–14.5%), but for students who need a quick student loan disbursement or who cannot meet PSU bank criteria, NBFCs are the practical choice.

- Private sector banks (ICICI, Axis) sit between the two: faster than PSU banks, more credibility than NBFCs, reasonable rates. ICICI Bank in particular has strong processing for students admitted to top-ranked international institutions.

🔴 Do not apply to multiple lenders simultaneously in the early stages of your search. Every formal loan application triggers a hard inquiry on the co-applicant's CIBIL report. Multiple hard inquiries within a short period lower the CIBIL score and make each subsequent application harder to approve. Shortlist your lenders first, then apply sequentially — starting with your first preference.

The Complete Education Loan Process — Step by Step

This is the full education loan for abroad process for Indian students. Follow the steps in order — each stage depends on the one before it. The timeline from application to first disbursement typically ranges from 6 to 12 weeks depending on lender type, collateral complexity, and document completeness.

| Stage | What to do | Documents / action required | Key mistakes to avoid |

|---|---|---|---|

| Confirm university admission and calculate total cost | Obtain your official offer letter or Letter of Acceptance (LOA). Calculate the total loan requirement: tuition fees (all years) + living costs + travel + health insurance + one-time setup costs. Most lenders require a cost breakdown from the university or your own detailed estimate. | Offer letter / LOA, university fee schedule, cost of attendance document (if provided by university) | Inflate your estimate slightly — it is easier to not draw the full loan than to apply for a top-up later. |

| Research and shortlist lenders | Compare public sector banks (SBI, Bank of Baroda), private banks (ICICI, Axis), and NBFCs (HDFC Credila, Avanse, Auxilo, InCred) based on: interest rate, maximum loan amount, collateral requirements, processing time, and whether their sanction letter is accepted by visa authorities in your destination country. | None — research phase only | Do not apply to multiple lenders simultaneously at the start — each hard inquiry affects your CIBIL score. Shortlist first, then apply sequentially if needed. |

| Check eligibility and pre-qualify | Confirm that you meet the lender's basic eligibility criteria: Indian citizen, admitted to a recognised foreign university, co-applicant (parent/guardian) with stable income, and CIBIL score above 700 (for co-applicant). Some NBFCs have more flexible criteria than public sector banks. | Academic records (10th, 12th, UG transcripts and certificates), co-applicant's income documents, CIBIL report | CIBIL score below 700 for the co-applicant significantly reduces your chances with public sector banks. NBFCs are more flexible but charge higher rates. |

| Gather and organise all documents | Compile the complete document set required by your chosen lender. The full checklist is covered in the next section. Missing even one document delays the process by 1–2 weeks. Prepare physical and digital copies of all documents before visiting the branch or uploading to an NBFC portal. | See Document Checklist section below | Do not submit documents piecemeal. Submit the complete set in one go. Incomplete submissions are the leading cause of processing delays. |

| Submit loan application (branch or online) | Public sector banks (SBI, Bank of Baroda) typically require a branch visit for education loan applications. NBFCs (HDFC Credila, Avanse, Auxilo) accept online applications and have dedicated relationship managers. Submit the application with the full document set. | Completed application form, full document set, processing fee (if applicable) | Always get an acknowledgement receipt or application reference number when submitting. This is your proof of application and helps track status. |

| Loan assessment and verification | The lender's credit team assesses your application: co-applicant income verification, collateral valuation (if applicable), university and course verification, and overall repayment capacity assessment. For collateral-secured loans, a property valuation by the bank's approved valuer is arranged. | Bank may request additional documents at this stage — respond within stated deadlines | If the bank requests additional documents, respond within 48–72 hours. Delayed responses extend processing time significantly. |

| Loan sanction and receipt of sanction letter | Once approved, the lender issues a Loan Sanction Letter stating the sanctioned amount, interest rate, repayment terms, and conditions. This sanction letter is a critical document — it is required for your student visa application in most countries (UK, USA, Canada, Australia, Germany). | Sanction letter is issued in your name and co-applicant's name — verify all details carefully before accepting | Check the sanction letter carefully: verify the sanctioned amount covers your full requirement, the interest rate matches what was quoted, and the lender's name and your details are correct. Errors in the sanction letter must be corrected before submission. |

| Complete loan agreement and mortgage formalities | Sign the loan agreement. For collateral-secured loans: submit original property documents to the bank, which holds them as mortgage security for the loan tenure. For non-collateral loans: complete the guarantee documentation with your co-applicant. | Loan agreement, original property documents (collateral loans), guarantee documents (non-collateral loans) | Keep a certified copy of all documents submitted to the bank. You will need these for tax filing and for when the property documents are returned after full repayment. |

| First disbursement and fee payment to university | Education loans are disbursed directly to the university in most cases — not to your personal account. The first disbursement typically covers the first semester or first year tuition fee. Initiate the disbursement request with the bank at least 4–6 weeks before the university's fee payment deadline. | University fee demand letter or invoice, bank account details of the university, disbursement request form | Do not assume disbursement will happen automatically. You must initiate each disbursement with a request and supporting invoice from the university. Missing the university's fee deadline can result in cancellation of your admission. |

| Subsequent disbursements and living expense draws | For living expenses and ongoing costs, subsequent disbursements are made either to the university or to your overseas account (depending on lender policy and your purpose). Keep all receipts and documentation — lenders may request proof of utilisation for ongoing disbursements. | Subsequent fee demand letters, receipts, living expense justification if required | Maintain a separate account for loan disbursements. Mixing personal and loan funds complicates documentation and repayment tracking. |

✅ The single most important thing you can do to speed up your loan process is to submit a complete document set on the first attempt. Incomplete applications are the leading cause of processing delays at every lender — public or private. Use the Document Checklist in the next section and verify every item before submission. A complete, well-organised application file signals to the lender's credit team that you are a prepared, serious applicant — and it shows in processing priority.

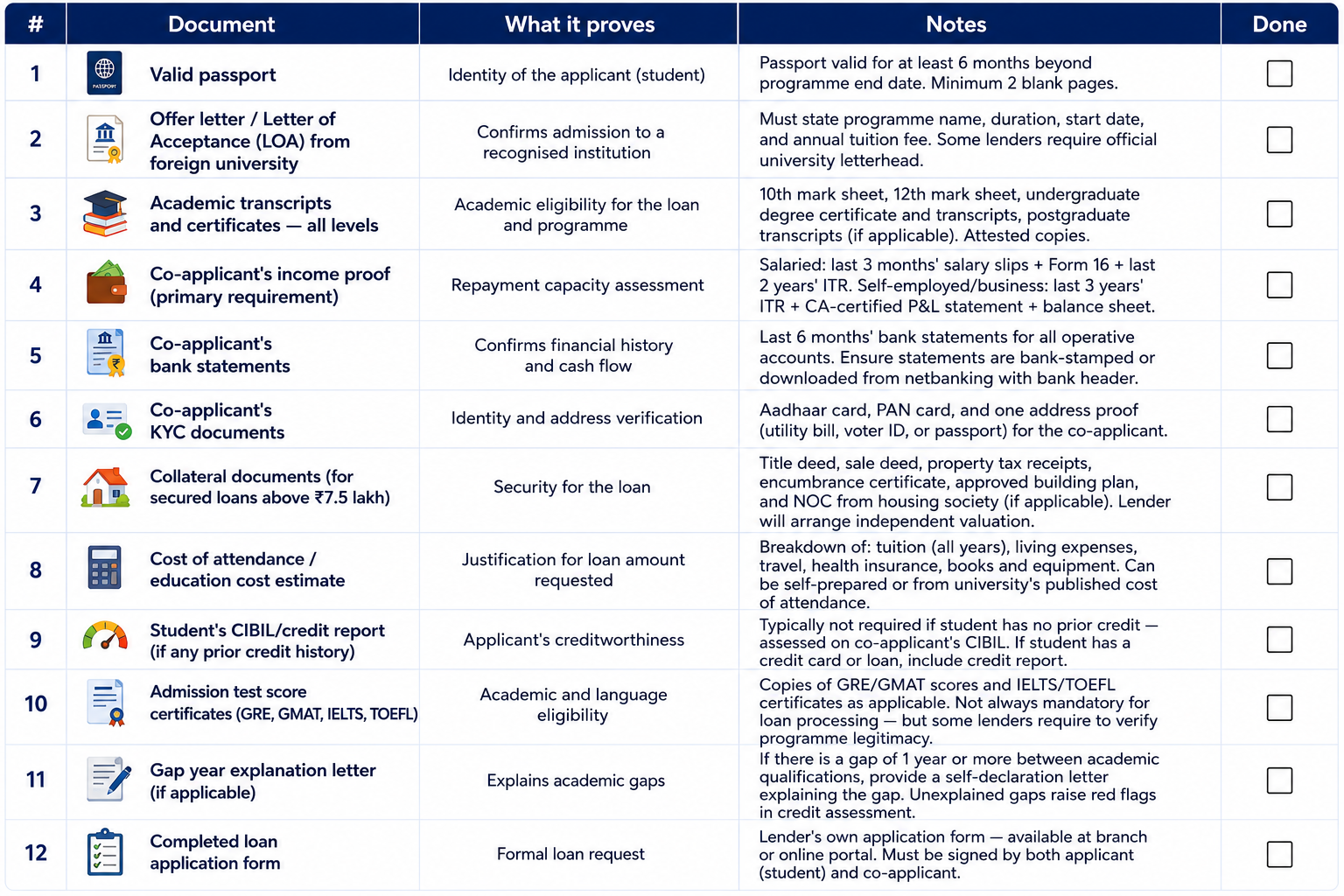

Complete Document Checklist for Education Loan Abroad

This is the definitive document checklist for Indian students applying for a student loan for abroad. Requirements vary slightly by lender — public sector banks typically require physical attested copies, while NBFCs often accept scanned uploads. Verify specific requirements with your chosen lender before submitting. A missing document at submission time delays processing by 1–2 weeks at minimum:

⚠️ Co-applicant income documents are the most scrutinised part of the education loan application. Lenders assess whether the co-applicant can service the loan if the student is unable to repay after graduation. For salaried co-applicants: ensure Form 16 and ITR are consistent with salary slips — discrepancies trigger additional verification and delay. For self-employed or business co-applicants: CA-certified financial statements carry significantly more weight than self-prepared documents. Do not underestimate how carefully this section is reviewed.

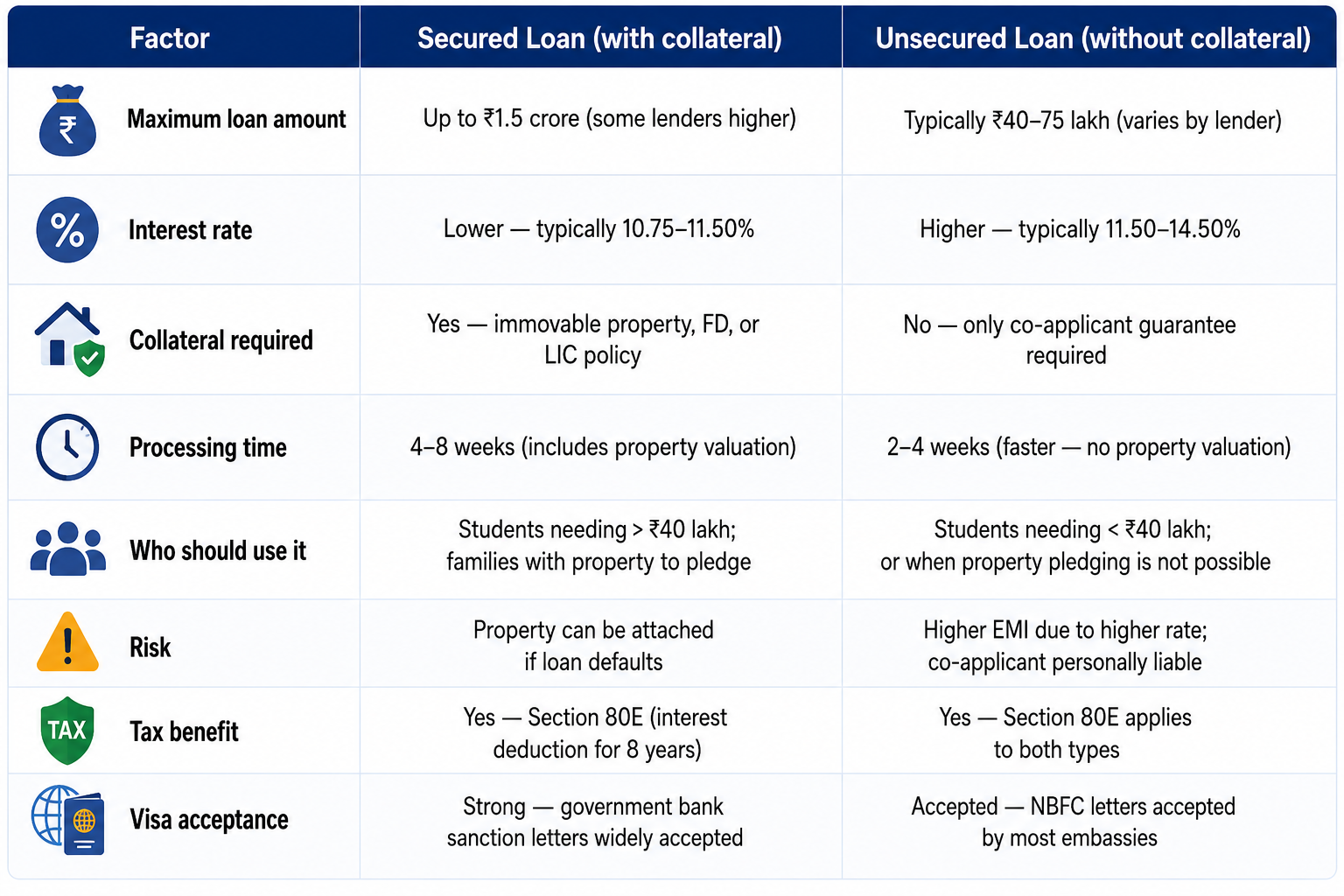

Secured vs. Unsecured Education Loans — Which Is Right for You?

One of the most important decisions in any international education loan application is whether to apply for a secured loan (backed by collateral — typically immovable property, fixed deposits, or a life insurance policy) or an unsecured loan (backed only by a co-applicant guarantee). The choice has significant implications for your interest rate, maximum loan amount, and processing timeline.

When to Choose a Secured Loan

A secured study abroad loan is the right choice when: (1) you need more than ₹40–50 lakh, which is the practical upper limit for most unsecured NBFC loans; (2) your family owns property that can be pledged without disrupting family finances; and (3) you have 8–12 weeks of processing time before your visa application deadline. The lower interest rate on secured loans compounds to meaningful savings over a 10–15 year repayment period — a 1.5% rate difference on a ₹50 lakh loan over 12 years amounts to over ₹5 lakhs in additional interest on an unsecured loan.

When to Choose an Unsecured Loan

An unsecured study abroad student loan from an NBFC is the right choice when: (1) your loan requirement is under ₹40–50 lakh; (2) your family does not have property available for pledging, or pledging property is not practicable; (3) you need a faster processing timeline — NBFCs can sometimes issue a sanction letter in 2–3 weeks, which matters when your visa application deadline is approaching. The higher interest rate is the trade-off for speed and accessibility.

💡 Tax benefit reminder: Under Section 80E of the Income Tax Act, the interest paid on any education loan — secured or unsecured, from any scheduled bank or approved financial institution — is fully deductible from your taxable income for 8 consecutive years starting from the year repayment begins. This deduction applies to the student (once they have taxable income in India) or to the co-applicant who is making payments. Claim this deduction every year — it is one of the most valuable and underutilised tax benefits available to Indian students who have taken an education loan abroad.

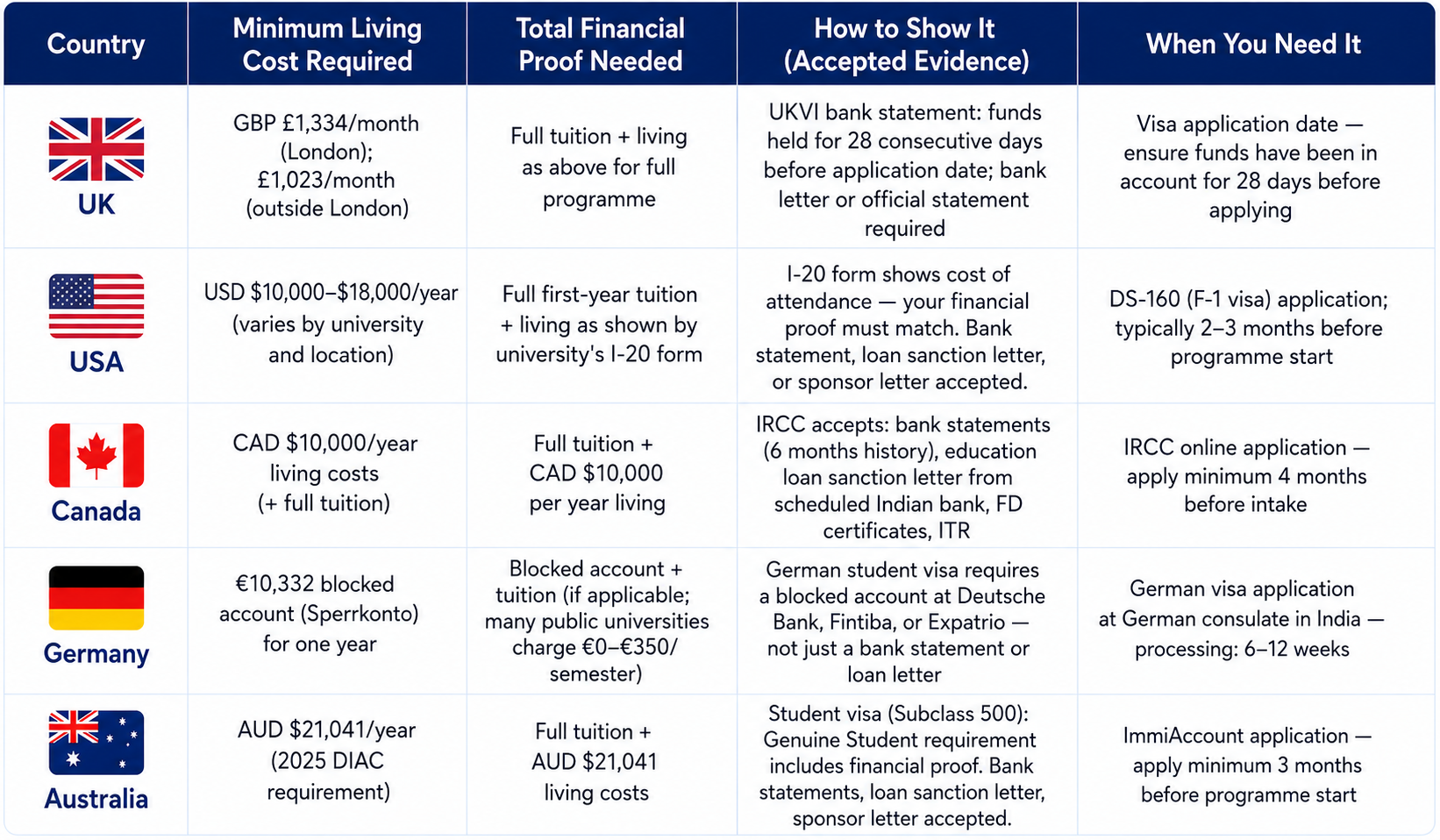

Country-Wise Financial Requirements — What Visa Authorities Need to See

Your international student loan sanction letter is a critical document in your student visa application — but each country's visa authority has specific requirements about how financial proof must be presented. Understanding these requirements before you finalise your loan amount and before you apply for your visa is essential. A sanction letter that does not cover the full financial requirement for your destination country will result in visa refusal, regardless of how strong the rest of your application is.

🔴 Germany is a special case that catches many Indian students off guard: the German student visa does not accept a loan sanction letter as proof of funds on its own. German visa authorities require a blocked account (Sperrkonto) containing the full annual living cost amount (€10,332 for 2025). This money must be deposited into a German blocked account provider — Deutsche Bank, Fintiba, or Expatrio — before your visa is issued, and you can only withdraw €861/month after arrival. If you are applying for an education loan to fund your Germany studies, plan to use the loan disbursement specifically to fund the blocked account. Coordinate your loan disbursement timeline with your blocked account funding requirement.

How Your Sanction Letter is Assessed by Visa Authorities

For UK, USA, Canada, and Australia — the four countries where a education loan for abroad sanction letter is directly accepted as financial proof — visa officers assess the following:

- Is the sanction letter from a scheduled Indian bank or a recognised NBFC? Government bank sanction letters (SBI, Bank of Baroda) carry the strongest credibility. NBFC sanction letters are generally accepted but may attract additional scrutiny at some embassies.

- Does the sanctioned amount cover the full financial requirement? The sanction letter must demonstrate coverage of tuition plus living costs as required by that country's visa authority — not just tuition alone.

- Is the loan fully sanctioned — or only approved in principle? A fully sanctioned loan letter (with a specific loan amount, terms, and lender commitment) is accepted. An in-principle approval is generally not sufficient for visa purposes.

- Are your personal details on the sanction letter correct? Name spelling, address, and other details must match your passport exactly. Discrepancies trigger additional verification.

✅ Always request your sanction letter to be in English, or accompanied by an official English translation. UK UKVI, US consulates, Canadian IRCC, and Australian DIBP all require financial documents in English. While Hindi-language sanction letters from PSU banks are legally valid in India, they create unnecessary complications at visa assessment. Most public sector banks will issue bilingual sanction letters on request — ask specifically for an English version when you request your sanction letter.

Moratorium Period and Repayment — What Indian Students Must Understand

The moratorium period is one of the most misunderstood aspects of any study abroad loan. Understanding it correctly — before you sign the loan agreement — prevents financial surprises after graduation.

What is the Moratorium Period?

The moratorium period is the time between loan disbursement and the start of EMI repayments. For education loans, the moratorium typically covers: the entire duration of your study programme, plus an additional 6–12 months after graduation (or after getting employment — whichever is earlier). During the moratorium, you are not required to make principal repayments.

⚠️ Critical point most students miss: interest continues to accrue on your outstanding loan balance during the moratorium period — even though you are not paying EMIs. This interest is typically added to your principal balance (capitalised), which means you start repayment on a higher amount than you originally borrowed. On a ₹50 lakh loan at 11.5% interest rate over a 2-year Master's programme plus a 6-month moratorium extension, the capitalised interest alone can add ₹13–15 lakhs to your outstanding balance by the time repayment begins. Understand this before signing. If you can make simple interest payments during the moratorium — even partial payments from part-time income abroad — it significantly reduces your total repayment burden.

Repayment Period and EMI Planning

Most international education loan repayment tenures range from 10 to 15 years from the date repayment begins (after the moratorium). Before signing, calculate your approximate monthly EMI using the lender's EMI calculator, and compare it against the realistic entry-level salary in your field and destination country after graduation. A ₹60 lakh loan at 11% over 12 years translates to approximately ₹73,500 per month in EMI — this is manageable on a post-graduation salary in the UK, Canada, or Australia, but requires planning.

- Plan your repayment before borrowing — not after. Use the lender's EMI calculator with your actual loan amount, interest rate, and expected tenure to calculate your monthly commitment.

- Section 80E deduction applies to interest paid for 8 consecutive years. If your post-graduation employment is in India, this deduction reduces your effective interest cost meaningfully — factor it into your repayment planning.

- Prepayment: most education loans allow prepayment without penalty. If you receive a performance bonus or windfall income in the early years of repayment, directing it toward loan prepayment reduces your outstanding principal and total interest paid significantly.

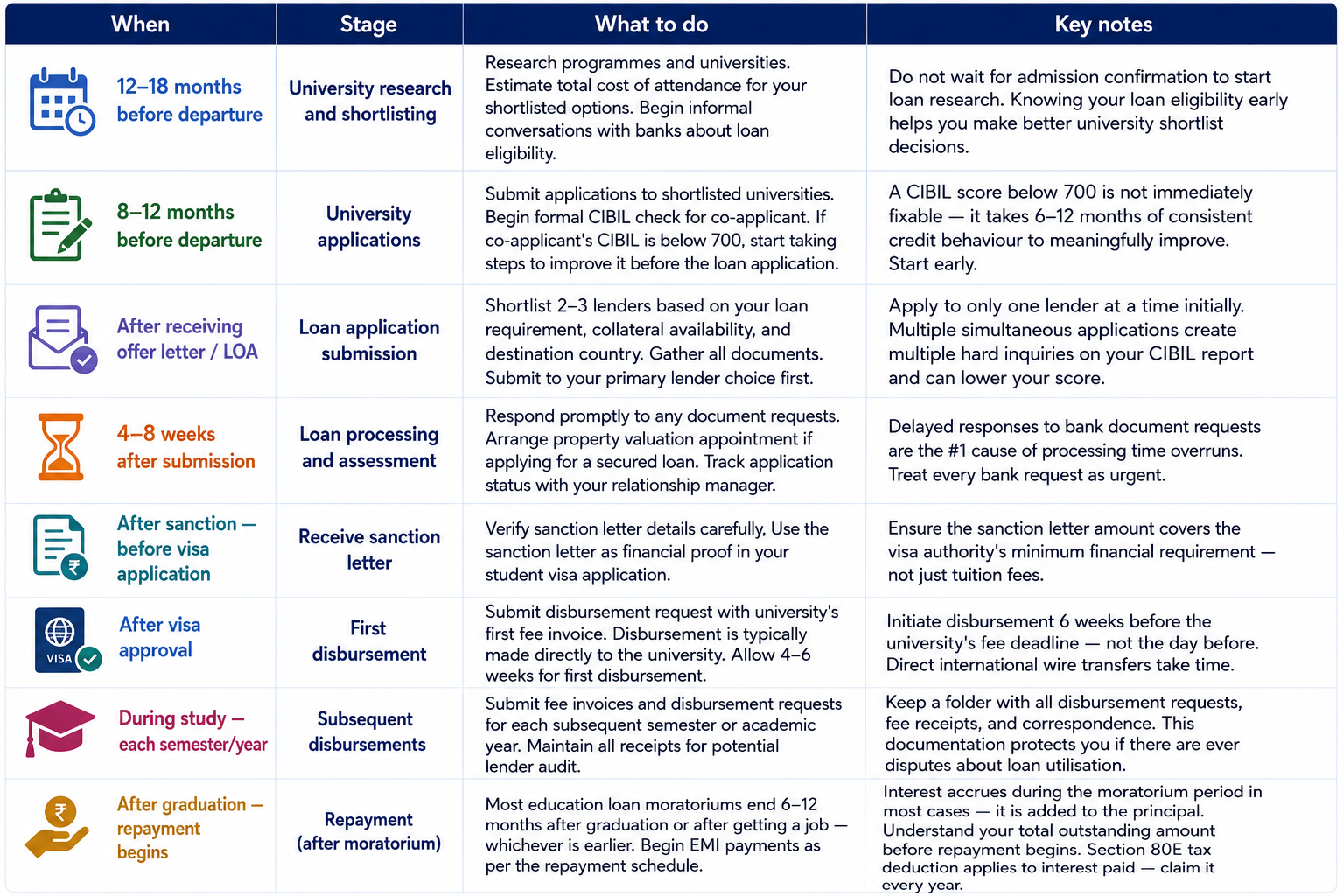

Education Loan Timeline — When to Do What

This is the recommended timeline for an Indian student targeting a September 2026 overseas intake who needs an education loan for abroad. Adjust the timing proportionally for January or February intakes:

📌 If you are applying for a quick student loan because your visa application deadline is close and you do not have time for a full public sector bank process: NBFCs (HDFC Credila, Avanse, Auxilo) are your best option for fast processing. They can sometimes issue a conditional sanction letter within 5–7 business days for applicants with strong co-applicant income and clean CIBIL scores. Be prepared to accept a slightly higher interest rate in exchange for speed. Contact Vidysea's counsellors for guidance on which lenders are processing fastest for your target country at any given time.

Frequently Asked Questions

Can I get an education loan without collateral for studying abroad?

Yes — most NBFCs and some private banks offer unsecured study abroad student loans without collateral for amounts up to ₹40–75 lakh, depending on the lender. The co-applicant's income and CIBIL score are the primary assessment criteria. HDFC Credila, Avanse, Auxilo, and InCred are the most commonly used lenders for collateral-free education loans for Indian students going abroad. The trade-off is a higher interest rate (typically 11.5–14.5%) compared to secured loans from public sector banks.

How much education loan can I get for studying abroad?

The maximum amount for an international education loan varies by lender: public sector banks like SBI and Bank of Baroda sanction up to ₹1.5 crore for overseas education with adequate collateral; NBFCs typically go up to ₹65–75 lakh. The sanctioned amount is based on: the total cost of your programme (tuition + living), the co-applicant's repayment capacity (income and existing obligations), and the value of collateral pledged (for secured loans). Most students find that their sanctioned amount is sufficient for their actual cost of attendance — the challenge is meeting eligibility criteria, not the loan ceiling.

Does an education loan sanction letter satisfy visa financial requirements?

For the UK, USA, Canada, and Australia — yes, a fully sanctioned education loan for abroad letter from a scheduled Indian bank or recognised NBFC is accepted as financial proof by visa authorities, subject to the amount covering the country's full financial requirement. For Germany, a sanction letter alone is not sufficient — a blocked account (Sperrkonto) is mandatory. For Schengen visas, financial requirements vary by country. Always verify the specific financial proof requirements of your destination country's visa authority before finalising your loan amount and application.

What is the interest rate on education loans for abroad in India in 2025–2026?

Interest rates on study abroad loans from Indian lenders in 2025–2026 range from approximately 10.75% (ICICI Bank, best cases) to 14.5% (NBFCs, unsecured, weaker profiles). Public sector banks (SBI, Bank of Baroda) offer rates in the 10.85–11.15% range for overseas education loans with adequate collateral. NBFCs offer 11.0–14.5% depending on loan amount, collateral, co-applicant profile, and the institution and country of study. Interest rates are floating in most cases, linked to the lender's MCLR or repo rate — they can change during your repayment period. Get the current rate confirmed in writing before signing.

How long does it take to get an education loan for abroad in India?

Processing time for an international student loan in India depends on the lender type: public sector banks (SBI, Bank of Baroda) typically take 4–8 weeks from complete document submission to sanction, including property valuation time for secured loans. NBFCs (HDFC Credila, Avanse, Auxilo) typically process in 2–4 weeks, and sometimes faster for straightforward applications. Private banks (ICICI, Axis) are typically 3–5 weeks. If you need a quick student loan to meet an urgent visa deadline, start with an NBFC and plan for 2–3 weeks minimum from complete document submission.

What happens to my education loan if my visa is rejected?

If your visa application is rejected after your loan has been sanctioned, the loan amount typically has not been disbursed yet — sanction and disbursement are separate stages. In this case, you can either: (1) reapply for the visa after addressing the refusal reasons — the loan sanction remains valid for a period (typically 6–12 months, check with your lender); (2) request loan cancellation before disbursement — most lenders will cancel without penalty if disbursement has not yet occurred; or (3) use the loan sanction for a different university in the same or another country, if the programme and institution change is agreed with the lender. Get confirmation of these options from your lender in writing before signing the loan agreement.

Should I use Vidysea's help for my education loan application?

Vidysea provides education loan assistance for Indian students going abroad, including lender shortlisting based on your profile and destination, document review before submission, coordination between your loan sanction timeline and your visa application process, and guidance on structuring your financial proof to meet destination-country visa requirements. The most common and most expensive education loan mistakes — applying to the wrong lender for your profile, submitting incomplete documents, not accounting for visa financial requirements in your loan amount, or misunderstanding the moratorium and capitalised interest — are all avoidable with the right guidance. If you are planning an education loan for abroad in 2025–2026, contact Vidysea's counsellors to review your options before you apply.

An education loan for studying abroad is a significant long-term financial commitment — but it is also one of the most widely available and well-structured forms of financing available to Indian students. The process is predictable, the lenders are established, and the documentation requirements are fixed. What separates students who complete the process smoothly from those who face delays and complications is preparation: starting the process early, submitting complete documents, choosing the right lender for the right reason, and understanding exactly how your sanction letter will function in your visa application.

Start your loan research at the same time as your university research — not after you receive your offer letter. The students who face study abroad loan processing emergencies are almost always the ones who waited until the offer letter arrived before beginning. The offer letter is the start of a process that takes 6–12 weeks to complete. If you begin your lender research and co-applicant CIBIL preparation 12 months before your intended departure, the entire loan process becomes manageable rather than stressful. Vidysea's study abroad guidance covers the full picture — admissions, loans, and visas — so that each stage is sequenced correctly and no deadline is missed.

Study Abroad Education Loan Process in India — Step by Step Guide 2025–2026