Education Loan vs Scholarship: Which Should You Apply for First?

This question has a short answer and a long answer. The short answer is: both, simultaneously — and the explanation of why is the most practically important thing this guide covers.

Team Vidysea

May 19, 2026

The mistake most Indian families make is treating scholarship and education loan for abroad as an either/or decision. Either they wait for scholarship results before applying for a loan (and miss their intake if the scholarship fails). Or they dismiss scholarships entirely and take on Rs. 50–80L of debt that a scholarship might have eliminated. Both errors are expensive.

The right strategy is a parallel application — pursue the scholarship on its timeline, and secure the study abroad student loan on a parallel track. If the scholarship comes through, reduce or close the loan. If it does not, you have your international education loan in place and your study abroad plan is not held hostage to a committee decision. This guide shows you exactly how to run both tracks — and which one to prioritise depending on your specific situation.

💡 The fundamental asymmetry

A scholarship is high-reward but uncertain. A study abroad loan is certain but has a cost. The optimal strategy does not choose between them — it secures the loan (certainty) while pursuing the scholarship (upside). The only scenario where scholarship-first makes sense is when you have 12+ months and the loan cannot be obtained at serviceable terms. In every other scenario, both tracks run simultaneously.

Scholarship vs. Education Loan — Complete Comparison

Before deciding sequencing, understand the genuine differences. This table compares scholarship (Chevening, DAAD, Fulbright, Erasmus Mundus, Commonwealth, Australia Awards) against education loan for abroad (SBI, HDFC Credila, Avanse, Prodigy Finance, MPOWER, Leap Finance) across every dimension that matters for an Indian student in 2026:

| Dimension | Scholarship (Chevening, DAAD, Fulbright, Erasmus Mundus…) | Education Loan (SBI, HDFC Credila, Avanse, Prodigy Finance…) |

|---|---|---|

| Cost to you | Zero — if you receive it. Tuition, living, flights covered. No debt. | Interest-bearing debt. Every rupee borrowed costs 1.5–2× over 10 years of repayment. |

| Probability of getting it | Low to very low. Chevening accepts ~3–5% of applicants. DAAD acceptance ~5–15%. Elite scholarships are genuinely competitive. | High — 70–85% approval rate for students admitted to QS top-200 universities with a qualifying co-applicant. A quick student loan from NBFCs approves in 5–7 days. |

| Time to apply | 12–18 months before intake. Scholarship calendars are rigid and cannot be rushed. | 4–8 weeks before intake. A study abroad student loan can be processed in parallel with visa application. Quick student loan options (Leap, Avanse) approve in 5–14 days. |

| Impact on study abroad plan | Does not change it — you study at the same university regardless of whether the scholarship comes through. | May affect which university you target (loan ceiling vs. total cost) and which country (loan serviceability varies by destination salary). |

| What you need to qualify | Strong academics, leadership, specific career goals, 2+ years work experience (Chevening), research proposal (DAAD). Field and values alignment matters. | University admission + co-applicant income + co-applicant CIBIL 700+ + QS top-200 university. No separate application essay. The admission letter does most of the work. |

| Risk | You may invest 60–80 hours on a scholarship application and receive nothing. This is the default outcome for most applicants. | You are approved and take on debt. The risk is that your post-graduation salary does not service the EMI — a real risk if the country choice, field, or starting salary is misjudged. |

| Processing | Scholarship decisions: 4–8 months after application submission. | Loan sanction: 7–30 days. Loan disbursal: post-visa, per semester. A quick student loan from NBFCs can sanction in 5–7 days. |

| Coverage | Usually tuition + living + flights. Some (DAAD WISE) are stipend-only. Read the fine print on what each scholarship covers. | Tuition + living + travel + equipment (varies by lender). The international education loan from NBFCs typically covers more cost categories than bank loans. |

| Effect on visa application | Scholarship sanction letter strengthens visa application — shows financial support from a credible government/institutional source. | Loan sanction letter is accepted for visa financial proof in all major destinations. For Germany blocked account, the loan disbursal can fund the Sperrkonto directly. |

| Repayment obligation | None. Scholarship is a grant, not a loan. Most government scholarships expect you to return to your home country and contribute (soft obligation, not legally enforceable). | Fixed repayment obligation post-moratorium. EMI is legally binding. Missing EMIs damages the co-applicant's CIBIL score and triggers recovery action. |

🎯 The acceptance rate reality check

Chevening admits approximately 3–5% of Indian applicants. DAAD Research Grant acceptance: 5–15%. Gates Cambridge: under 1%. Erasmus Mundus: 5–10% for funded places. Compare this to a study abroad student loan approval rate of 70–85% for students admitted to QS top-200 universities. This asymmetry is not an argument against scholarships — it is an argument against making your study abroad plan dependent on one.

Decision Framework: Which Should You Apply for First?

The answer is almost never binary. The question is really: given your timeline and profile, how should you sequence and weight the two applications?

| Your situation | Apply first | Why |

|---|---|---|

| Intake is September 2027 or later | Scholarship | You have 12–18 months — the minimum timeline most competitive scholarships require. Apply to 3–5 scholarships now. Apply for the education loan 8–12 weeks before your intake regardless of scholarship outcome. |

| Intake is September 2026 or January 2027 | Loan first, scholarship in parallel | Your intake is 4–8 months away. Most scholarship deadlines for September 2026 have already closed. Secure the loan now. Apply for any open scholarship rounds simultaneously — but don't delay the loan waiting for scholarship news. |

| You have strong academics (8.0+ CGPA, clear leadership record, 2+ years work experience) | Scholarship as priority — loan as backup | Your profile is competitive for Chevening, DAAD, and Commonwealth. Invest the time. But file the loan application at the same time so your plan does not depend on a scholarship outcome. |

| You have a scholarship offer in hand | Accept the scholarship and take a loan for the gap | Most scholarships do not cover 100% of costs (living shortfall, equipment, flights, visa fees). A small international student loan or study abroad loan tops up the gap. HDFC Credila and Avanse will loan the shortfall even when a scholarship covers tuition. |

| Your co-applicant has low income or poor CIBIL | Scholarship first, aggressively | A low-income co-applicant or CIBIL below 700 makes a large unsecured study abroad student loan difficult to obtain at good rates. Scholarships that do not require repayment become even more critical. Pursue all available options including DAAD, Erasmus Mundus, and MPOWER (no Indian co-signer needed). |

| Your field is STEM and your target is USA or Germany | Secure the loan; treat scholarship as bonus | STEM students in USA/Germany have strong loan serviceability based on destination salary. A 10-year student loan for abroad at 11–13% is financially manageable if starting salary exceeds USD 80K or €55K. Don't gamble your intake on a scholarship — get the loan in place. |

| You are applying to a country where tuition is near-zero (Germany public unis) | Neither loan nor scholarship urgently needed | Germany public university tuition is €0. A study abroad loan of Rs. 10–15L covers living costs (blocked account + first-year living). Scholarships like DAAD add a stipend. The loan requirement is much lower than for UK/USA/Australia. |

| You've been rejected from scholarship before | Loan first | Previous rejection patterns suggest reapplication odds are similar or lower. Secure financing first. Use the extra time to strengthen the scholarship application for the following cycle — not to delay your intake. |

The Combined Strategy — Running Both Tracks Simultaneously

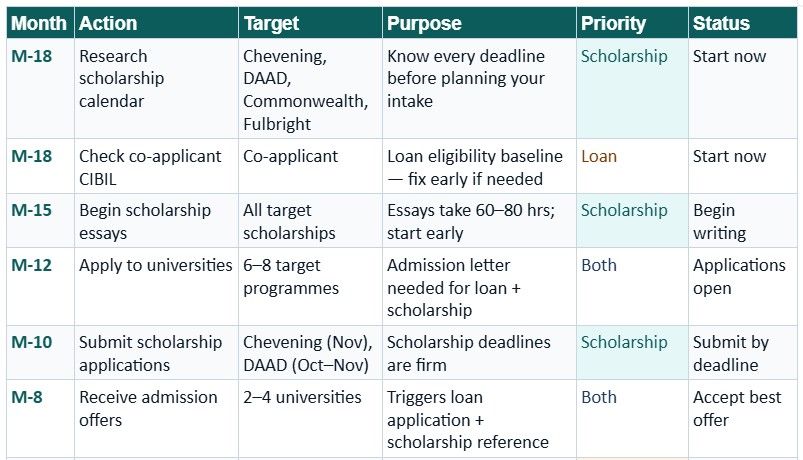

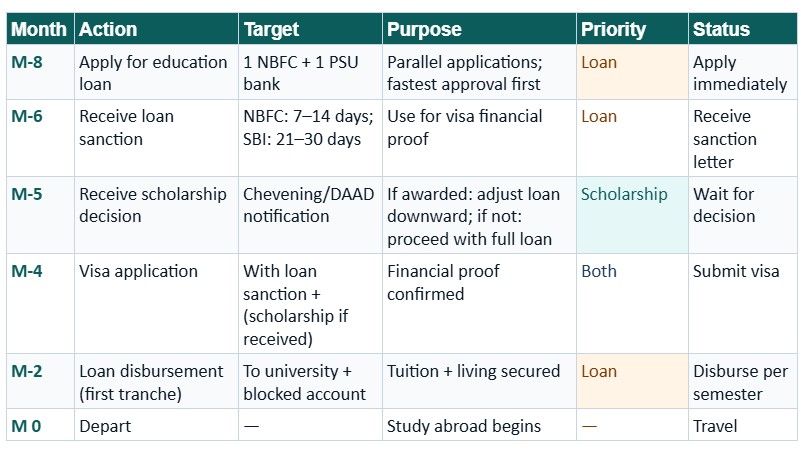

For most Indian students targeting a September 2027 intake, both applications can and should run in parallel from 18 months before intake. This timeline shows the correct sequencing:

✅ Month -5 is the most important moment in the combined strategy

When scholarship decisions arrive (typically 4–5 months before intake), you have two paths: (1) Scholarship awarded — use it to reduce or close your pending loan; most lenders will adjust the loan amount or cancel at no cost if notified before disbursal. (2) Scholarship not awarded — your loan sanction is already in place, your visa proof is ready, and your study abroad plan proceeds unchanged. This is the insurance logic of the parallel strategy: you are protected either way.

When You Need a Quick Student Loan — Fast-Track Options

For students who are already close to their intake date and cannot afford to wait, a quick student loan is the priority. Scholarship applications for the next cycle can happen after enrolment — a deferred scholarship for Year 2 or a mid-programme award is still valuable. These lenders provide the fastest international student loan approvals in India:

- Leap Finance: 5–7 day digital approval for students admitted to partner universities. Rs. 75L maximum unsecured. No branch visit required.

- Avanse Financial: 7–10 day approval. One of the broadest university coverage networks among NBFCs. Living costs covered. Rs. 75L maximum.

- Prodigy Finance: 7–10 day online process. No Indian co-applicant required. USD 220K maximum for international students at eligible global programmes.

- MPOWER Financing: 7–14 days. No collateral, no co-signer. For USA and Canada specifically. Up to USD 100,000.

Note: a quick student loan from these NBFCs typically carries a higher interest rate (11–14%) than a PSU bank loan. For students with urgent timelines, the speed premium is worth it. For students with 3+ months, running an SBI Scholar Loan application in parallel gives a lower-rate option that may come through before disbursal is needed.

The Four Most Expensive Financial Mistakes in Study Abroad Planning

Understanding what goes wrong when scholarship and loan planning are poorly sequenced prevents the most costly errors:

Mistake 1: Waiting for scholarship results to apply for a loan

The scholarship application for September 2027 typically closes in October–November 2026. Results arrive in April–May 2027. Most study abroad student loan approvals take 7–30 days. Waiting for scholarship results to start the loan application means the loan is not in place by the May–June visa application window. Starting the loan process in October 2026 alongside the scholarship application ensures both tracks are ready.

Mistake 2: Taking a loan for the full cost without checking scholarship eligibility

A student who takes Rs. 60L in international education loan for a UK MSc programme may have been eligible for the Chevening Scholarship, which covers the entire tuition and living. Missing the Chevening deadline by 3 months because they were focused on the loan application costs the equivalent of the entire scholarship — approximately Rs. 55–70L in loan cost over 10 years of repayment. Scholarship eligibility check takes 30 minutes. Always check scholarship eligibility before finalising loan amount.

Mistake 3: Choosing a university based on scholarship probability, not programme fit

Some students choose a lower-quality programme because they believe it has a higher scholarship probability. This is almost never correct — most scholarships (Chevening, DAAD, Commonwealth) cover any accredited institution in their country. Chevening covers any eligible UK university — there is no advantage to applying to a lower-ranked programme. Choose the right university and programme, then apply for scholarships on the basis of personal merit, not institutional tier.

Mistake 4: Not reading what the scholarship actually covers

Scholarship coverage varies enormously. DAAD WISE covers a stipend only — not tuition, not flights. The Aga Khan Foundation covers most costs for select fields. Chevening covers tuition + living but students typically find they need supplementary study abroad loan for the first month before living allowance payments begin, equipment, and visa costs. Always model the gap between scholarship coverage and total cost — and have a quick student loan plan for the gap before you travel.

Frequently Asked Questions

Can I hold both a scholarship and an education loan for abroad simultaneously?

Yes — many students do. If a scholarship covers tuition and living, you may still take a small student loan for abroad for the gap (equipment, visa costs, first-month bridge). Most lenders are aware of this structure and will lend the shortfall. Inform your lender that you have a scholarship covering tuition — they will adjust the loan purpose accordingly. There is no rule preventing simultaneous scholarship and loan holding.

Do scholarship funds affect my loan eligibility?

If you receive a scholarship after your loan is sanctioned, most lenders will reduce the loan amount or close it at no penalty — contact your loan officer immediately when you receive the scholarship offer. If you have already disbursed part of the loan to the university, the scholarship body may pay tuition directly to the institution, allowing you to redirect your loan to other costs. Coordinate between lender and scholarship body; both are used to this situation.

My scholarship application was rejected. Should I reapply or focus on the loan?

Both, in parallel. A scholarship rejection from one cycle does not prevent reapplication the following year. Chevening and Commonwealth specifically encourage reapplication — many successful scholars applied 2–3 times before being awarded. Secure your international student loan for this intake, study abroad, and reapply for the scholarship for a partial scholarship, Year 2 support, or a research award post-programme. A scholarship rejection is a setback, not a disqualification.

Does having a scholarship affect my visa application positively?

Yes — significantly. A government scholarship letter (Chevening, Fulbright, Commonwealth, DAAD) is one of the strongest financial support documents a student can present in a visa application. It demonstrates not just the funding but the institutional vetting behind it — the awarding body has already verified your profile. If you have a scholarship offer, include the letter prominently in the visa financial proof section alongside or instead of the education loan for abroad sanction letter.

Is there a study abroad loan option that requires no co-applicant — like a scholarship?

Yes — Prodigy Finance and MPOWER Financing offer international student loans with no Indian co-applicant, co-signer, or collateral required. They assess eligibility based on university ranking, programme, and projected future earnings. The trade-off is a higher interest rate (11–15% for USD-denominated loans) and currency risk. These are the closest loan equivalents to a no-obligation scholarship — there is no family asset risk, no family income requirement, and no co-applicant CIBIL dependence.

The scholarship vs. loan question is not a choice between hope and debt. It is a question of sequencing two financial tools that serve different purposes and carry different probabilities. Apply for both. Let the scholarship be the upside. Let the study abroad student loan be the foundation. Build your plan around certainty, and let the scholarship improve it if it comes through.

Related Articles

Top Universities for Business Analytics in France 2026: Best Business Schools, Fees, Eligibility, Scholarships & Career Opportunities

Top Universities for MBA in France 2026: Best Business Schools, Fees, Eligibility, Careers & ROI

After MS Jobs in France: Career Opportunities, Salaries, Work Visa & PR Pathways