Education Loan Without Collateral for Study Abroad: Who Qualifies, How to Apply, and Which Lender Is Right for You

The biggest misconception about study abroad loans in India is that you need a house, a fixed deposit, or a piece of property to get one. This was true in 2015. In 2026, it is not — not for the right profile, applying to the right university, through the right lender. Unsecured education loans — study abroad student loans that require no collateral — are now available up to Rs. 75 lakh from NBFCs and up to Rs. 1 crore with certain private banks, with no property mortgage and no FD pledge required. The key is understanding who qualifies, which lenders offer the best terms for which profiles, and what the application process actually involves.

Team Vidysea

May 19, 2026

This guide covers every aspect of unsecured education loans for abroad: the 10 major lenders, their eligibility criteria, interest rate ranges, and which profile each lender is best suited for. It includes a complete student loan for abroad application checklist, an EMI calculator reference table, and a section on quick student loan options for students with tight timelines.

💡 Collateral vs. non-collateral: the actual difference

A collateral education loan requires you to pledge a tangible asset — property, FD, gold, or insurance policy — as security against the loan. If you default, the lender can claim the asset. A non-collateral (unsecured) education loan is approved based on your academic profile, the university ranking, the programme's employment prospects, and the co-applicant's income and credit score. You pay a higher interest rate for the reduced security to the lender — typically 1.5–3% more than collateral-backed loans.

Who Qualifies for an Unsecured Study Abroad Loan?

The short answer: students admitted to globally ranked universities with strong co-applicants. The detailed answer is more nuanced — different lenders weight different criteria differently, and understanding this lets you match your profile to the lender most likely to approve your application at the best terms.

| Criterion | What lenders check | Minimum to qualify | What improves your terms |

|---|---|---|---|

| University ranking | QS ranking of admitted university, country, and programme | Top 150–500 globally depending on lender; some require QS top 200 | QS top 100 → lowest rates and highest loan amounts without collateral |

| Academic record | Undergraduate CGPA and backlog history | 6.5+ CGPA on 10-point scale; no active backlogs at time of application | 8.5+ CGPA → best terms; clean academic record → easier approval |

| Admission status | Admission letter (conditional or unconditional) | Conditional offer accepted; unconditional strongly preferred for fast disbursal | Unconditional offer + visa approval → fastest disbursement timeline |

| Co-applicant / guarantor | Indian co-applicant (parent, sibling) income and CIBIL score | Co-applicant income Rs. 20,000+/month; CIBIL 700+ preferred | Co-applicant with Rs. 5L+ annual income + 750+ CIBIL → best terms |

| Programme field | STEM vs. non-STEM; employability of the degree field | Most fields accepted; some lenders restrict arts/humanities | STEM, computer science, engineering, data analytics → highest approval and lowest rates |

| Country destination | Risk classification of destination country | USA, UK, Canada, Australia, Germany, Ireland most favoured | USA/Germany/Canada → lowest risk, best terms; Australia (post-Ev.3) now requires more documentation |

| Loan amount to cost ratio | Loan as a percentage of total programme cost | Typically lend up to 85–100% of total cost (tuition + living + fees) | Showing personal funding contribution for 15–20% of cost improves approval odds |

| Repayment capacity | Post-graduation salary potential in destination country | Starting salary projection must support EMI after moratorium period | STEM in USA/Canada/Germany → highest projected salary → best terms |

✅ The university ranking is the single most important variable

For unsecured study abroad loans, the university ranking is the lender's primary collateral. A student admitted to a QS top-50 university gets approved by every major lender at competitive rates with no collateral. A student admitted to a QS rank 400–500 university may need to provide a co-applicant income above Rs. 5L annually, or shift to a partially secured structure. Before applying for any international education loan, check where your university ranks on QS, THE, and Shanghai rankings — these are the three scales most Indian lenders use.

10 Lenders Compared — International Student Loan Options for India 2026

The international student loan market in India has three segments: NBFCs specialised in study abroad (fastest, highest rates), private banks (mid-speed, mid-rates), and PSU banks (slowest, lowest rates). Understanding which lender to approach first — based on your timeline, university, and profile — saves weeks of wasted applications.

| Lender | Type | Max loan | Interest rate | Collateral | Processing | Quick loan? | Best for |

|---|---|---|---|---|---|---|---|

| Prodigy Finance | NBFCintl. | USD 220K | ~11–14% (floating) | None | 7–10 days | Yes | International students at top-ranked universities; no Indian co-signer needed |

| MPOWER Financing | US NBFC | USD 100K | ~12–15% (fixed) | None | 7–14 days | Yes | Indians at US/Canadian universities; no collateral, no co-signer |

| Leap Finance | Indian NBFC | Rs. 75L | 10.5–13.5% | None | 5–7 days | Yes ★ | Quick student loan for top-university admits; fast digital process |

| Avanse Financial | Indian NBFC | Rs. 75L | 11–14% | None (up to Rs.75L) | 7–10 days | Yes | Broad university coverage; covers living costs; fast disbursal |

| InCred Finance | Indian NBFC | Rs. 75L | 11–15% | None (top unis) | 7–14 days | Yes | STEM graduates; covers living + tuition + equipment |

| Auxilo Finserve | Indian NBFC | Rs. 75L | 11–14% | None (top unis) | 7–10 days | Yes | Strong coverage for UK, Canada, Australia; living costs covered |

| HDFC Credila | Indian NBFC | Rs. 1 Cr+ | 10.5–13% | None (select) | 10–15 days | No | Trusted brand; covers most universities; negotiable for top admits |

| SBI Scholar Loan | PSU Bank | Rs. 40L | ~8.15–9% | None (NITs/IITs abroad) | 21–30 days | No | Lowest interest rate; slower; best for top-ranked admits with time |

| Axis Bank | Private Bank | Rs. 75L | ~12–14% | None (top unis) | 14–21 days | No | Good for UK/Australia; income-based co-applicant required |

| ICICI Bank | Private Bank | Rs. 1 Cr | ~11–14% | None (select) | 14–21 days | No | High loan amount; collateral can be waived for premium programmes |

⚠️ Interest rate comparison must account for the loan structure

HDFC Credila and SBI base their rates on CIBIL + repo rate and can vary significantly by profile. NBFCs like Prodigy Finance charge in USD (for US loans), which creates a currency risk: if the rupee weakens against the dollar, your effective EMI in rupees increases. For USD-denominated international education loans, always model the worst-case exchange rate (10–15% rupee depreciation) alongside the stated rate.

Quick Student Loan Options — When You Have Less Than 30 Days

A quick student loan is not a different type of loan — it is a standard study abroad loan processed through a lender with a fast digital application and disbursement pipeline. Most Indian families need their loan approved before booking flights, paying the first instalment to the university, or applying for the visa. For students with imminent deadlines, these lenders have the fastest timelines:

- Leap Finance: 5–7 day approval for top-university admits. Fully digital process. Rs. 75L maximum unsecured. Admission letter required; visa not required for approval.

- Avanse Financial: 7–10 day approval. One of the fastest in the NBFC segment. Covers tuition, living, and travel. Rs. 75L maximum unsecured.

- Prodigy Finance: 7–10 day online approval for international students at eligible programmes. No Indian co-applicant or co-signer required. Rates quoted in USD.

- MPOWER Financing: 7–14 day process. Specifically for students in USA and Canada. No collateral, no co-signer, no Indian co-applicant. Up to USD 100,000.

For students with 30+ days before their deadline, PSU banks (SBI, Bank of Baroda) offer lower interest rates at the cost of longer processing times (21–30 days minimum). If your intake is 3+ months away, starting with SBI Scholar Loan and running it in parallel with one NBFC gives you the best of both: lowest rate if SBI approves, and a fast backup if it does not.

✅ The parallel application strategy

Apply to one NBFC (Avanse, Leap, or InCred) and one PSU bank (SBI) simultaneously. The NBFC will approve faster and can be used as a fallback or primary loan. The SBI loan, if it comes through, often has the lowest interest rate — use it as the primary and use the NBFC approval as leverage to negotiate better terms with SBI. Many families successfully negotiate SBI interest rates down by showing an existing NBFC approval.

EMI Calculator — What Your Study Abroad Student Loan Actually Costs

Before applying for any international education loan, run the EMI calculation against your expected starting salary in your destination country. The number that matters is not your total loan amount or the interest rate — it is net monthly income minus EMI in the first 12 months after graduation. If this number is negative, you are in financial distress from Day 1.

| Loan amount | Interest rate | Moratorium | Repayment period | Monthly EMI (est.) | Total repayment | Manageable if starting salary > |

|---|---|---|---|---|---|---|

| Rs. 20L | 11% | 2 years | 7 years | Rs. 37,000 | Rs. 31L | Rs. 55,000/month net (India) or equiv. abroad |

| Rs. 30L | 11% | 2 years | 7 years | Rs. 55,000 | Rs. 46L | Rs. 80,000/month net (India) or equiv. abroad |

| Rs. 40L | 11.5% | 2 years | 7 years | Rs. 75,000 | Rs. 63L | Rs. 1.1L/month net (India) or equiv. abroad |

| Rs. 50L | 12% | 2 years | 10 years | Rs. 72,000 | Rs. 86L | Rs. 1.0L+/month net — Germany/Canada viable; India tight |

| Rs. 60L | 12% | 2 years | 10 years | Rs. 86,000 | Rs. 1.03Cr | USD 55K+/year (USA) or £40K+ (UK) comfortably services this |

| Rs. 75L | 13% | 2 years | 12 years | Rs. 95,000 | Rs. 1.37Cr | USD 70K+/year (USA) or €60K+ (Germany) recommended |

| Rs. 1Cr (USD 120K) | 13.5% | 2 years | 12 years | Rs. 1.25L | Rs. 1.8Cr | USD 90K+/year (USA) — viable for top US STEM MS with strong starting salary |

🔴 The TCS rule that affects your loan cost in 2026

Tax Collected at Source (TCS) applies to education loan remittances abroad. Under Budget 2026, TCS on education loans exceeding Rs. 7 lakh per year is charged at 0.5% if funded through an education loan from a financial institution (reduced from 5% for personal remittances). This is a tax credit — you can claim it in your ITR — but it is a cash flow consideration. If you are remitting Rs. 40L in one tranche (e.g., full-year tuition at a US university), the TCS is Rs. 20,000 — plan for it in your disbursement request.

How to Apply — Step-by-Step for an Unsecured International Education Loan

The application process is largely standardized across lenders, with variations in digital capability and processing speed. Here is the complete process:

Step 1: Confirm your loan eligibility before applying (30 minutes)

Check your university on the lender's approved university list. Most major NBFCs publish their list online. SBI's Scholar Loan scheme has a specific approved university list — if your university is not on it, you cannot apply for that scheme. Prodigy Finance and MPOWER have their own eligible programme lists. Wasting time on a lender who does not cover your university is the most common application error.

Step 2: Gather your documents (2–3 weeks for all documents)

The document checklist below covers every major lender's requirements. Start collecting these in parallel with your loan research — do not wait for an approval to start gathering documents. The co-applicant's documents (ITR, bank statements, CIBIL) are often the slowest to collect.

Step 3: Apply to 2–3 lenders simultaneously

Submit to one NBFC (fast approval, higher rate) and one PSU bank (slow approval, lower rate) simultaneously. Add a second NBFC if your university is not top-100 and you want maximum approval probability. Multiple loan applications do not hurt your CIBIL score if submitted within a 14-day window — credit bureaus treat same-type applications within 14 days as a single inquiry.

Step 4: Loan approval and sanction letter (7–30 days depending on lender)

Once your documents are verified and the lender is satisfied, they issue a sanction letter — your formal loan approval with the amount, interest rate, and terms. The sanction letter is not the same as disbursement. You need the sanction letter for the visa application in most countries.

Step 5: Disbursement (after visa approval, usually)

Most lenders disburse in tranches — typically per semester or academic year. The first tranche is usually disbursed directly to the university's bank account (for tuition). Living expense components may be disbursed to the student's account. Confirm the disbursement method with your lender before you travel — some lenders require an Indian bank account for the first disbursement even if you are already abroad.

Complete Study Abroad Loan Document Checklist

This checklist applies to all major lenders for unsecured study abroad loans in 2026. Print it and tick off each document as you collect it.

| NO | Document | Why needed | When to get it | Done |

|---|---|---|---|---|

| 1 | Unconditional or conditional admission letter | Primary loan eligibility trigger — no letter, no loan disbursement | Get as soon as university accepts; conditional = loan approved in principle, full disbursal after unconditional | ☐ |

| 2 | 10th and 12th mark sheets + passing certificates | Academic history verification | From school records — usually accessible immediately | ☐ |

| 3 | Undergraduate degree certificate + transcripts | CGPA verification and programme eligibility | From university; allow 1–3 weeks if not already printed | ☐ |

| 4 | IELTS/TOEFL/GRE/GMAT score cards | Language and aptitude proficiency documentation | Download from respective test authority portal | ☐ |

| 5 | Passport (applicant) — valid 6 months beyond visa expiry | Identity and international travel documentation | Renew if less than 18 months remaining | ☐ |

| 6 | Passport (co-applicant if applicable) | Identity verification for guarantor | Co-applicant should renew if needed | ☐ |

| 7 | Co-applicant income proof: last 6 months salary slips + bank statements | Repayment capacity assessment | From co-applicant's employer and bank | ☐ |

| 8 | Co-applicant ITR (last 2 years) + Form 16 | Annual income and tax compliance verification | From co-applicant's CA or employer HR | ☐ |

| 9 | Co-applicant CIBIL report (official, within 3 months) | Credit history check — impacts approval odds | Download from CIBIL.com or free from bank | ☐ |

| 10 | University fee structure letter / I-20 (USA) / CAS (UK) | Formal fee confirmation for loan amount determination | From university admissions office | ☐ |

| 11 | Visa approval document (if obtained) | Strengthens disbursal request; not always required at approval stage | From embassy — submit once received | ☐ |

| 12 | Accommodation proof / rental confirmation (if available) | For lenders who cover living expenses | From university accommodation office or private landlord | ☐ |

| 13 | Loan application form (lender-specific) | Formal loan request | Complete on lender's online portal or branch | ☐ |

| 14 | 2 recent passport photos | KYC compliance | Recent (within 6 months) | ☐ |

💡 The CIBIL score of your co-applicant is critical — check it before applying

A co-applicant with a CIBIL score below 700 will either result in rejection or a significantly higher interest rate from most lenders. Before starting your loan application, ask your co-applicant to pull their free CIBIL report (from CIBIL.com, Paisabazaar, or directly via their bank's internet banking). If the score is below 700, spend 2–3 months building it before applying — paying off any outstanding credit card balance and settling any defaults will have the fastest impact. Applying with a 680 CIBIL and getting a rejection or a 14% rate is a worse outcome than applying at 720 three months later.

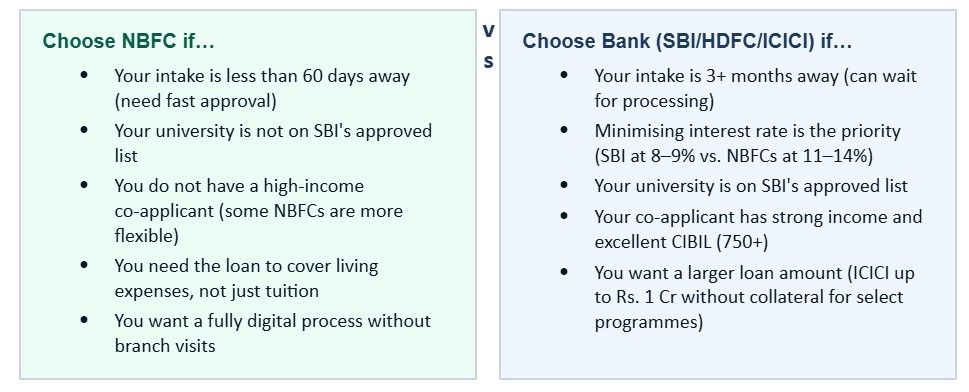

NBFC vs Bank: Which Type of Lender Is Right for You?

The debate between NBFC study abroad loans (Avanse, Leap, InCred, Auxilo) and bank education loans (SBI, HDFC Credila, ICICI, Axis) comes down to three factors: timeline, rate tolerance, and university eligibility coverage.

Frequently Asked Questions

How much study abroad loan can I get without collateral?

Most NBFCs (Avanse, Leap, InCred, Auxilo, HDFC Credila) offer up to Rs. 75 lakh unsecured for top-ranked universities. ICICI and HDFC can extend to Rs. 1 crore without collateral for select elite programmes. Prodigy Finance offers up to USD 220,000 for international students at eligible global programmes. The maximum unsecured amount depends on your university ranking, programme, field, and co-applicant profile — not a fixed ceiling that applies universally.

Does applying for multiple loans hurt my CIBIL score?

Hard enquiries from loan applications do reduce your CIBIL score slightly — typically by 5–10 points per enquiry. However, credit bureaus treat multiple same-type applications within a 14-day window as a single enquiry (rate shopping). If you apply to 3 lenders within 14 days, it counts as one enquiry. Apply in a clustered window, not spread over 3 months, to protect your co-applicant's CIBIL score.

Can I get an education loan without a co-applicant?

Yes — through Prodigy Finance and MPOWER Financing. Both are international student loans that do not require an Indian co-applicant, co-signer, or collateral. They assess eligibility based on your university ranking, programme, and future earning potential. The trade-off: interest rates are higher (11–15% for USD-denominated loans, creating additional currency risk). These are the best options for students whose parents do not meet co-applicant income criteria.

What happens to my loan if my visa is rejected?

Most lenders have a visa refusal clause — if your student visa is refused after the loan has been sanctioned but before disbursement, the loan sanction is cancelled and no fees are charged for the cancellation. If the visa is refused after partial disbursement (e.g., tuition has been paid directly to the university), the situation is more complex — you may need to negotiate a refund from the university and work with the lender on repatriation. Always read the visa refusal clause in your loan agreement before signing.

Is a study abroad loan the same as an international education loan?

The terms study abroad loan, international education loan, student loan for abroad, and education loan for abroad all refer to the same product in the Indian market: a loan taken by an Indian student to fund education at a university outside India. The terminology varies by lender and platform. The product structure — moratorium during study, EMI post-graduation, co-applicant requirement, collateral or not — is standardised regardless of what the lender calls it.

What is the moratorium period, and how does interest work during it?

The moratorium period is the time during which you are not required to make EMI payments — typically the course duration plus 6–12 months after graduation. During the moratorium, simple interest accrues on the disbursed amount. Most lenders expect you to pay at least the accrued interest during moratorium (called 'simple interest during moratorium' payments) to prevent the total outstanding principal from ballooning. A student who pays nothing during a 2.5-year moratorium on a Rs. 50L loan at 12% will find the principal has effectively become Rs. 65L+ by the time EMI begins. Build moratorium interest payments into your part-time work income plan abroad.

The study abroad loan landscape in India in 2026 is more accessible and more competitive than it has ever been. The right loan for your profile exists — the variable is finding the right lender for your university tier, timeline, and financial background. A Rs. 50L international education loan at 11% over 10 years is a manageable investment if your starting salary supports the EMI. The same loan at 14% from the wrong lender is significantly more expensive for identical outcomes. Getting this right — which lender, which structure, which terms — is the financial decision that most directly affects your post-graduation life.

Related Articles

Top Universities for Business Analytics in France 2026: Best Business Schools, Fees, Eligibility, Scholarships & Career Opportunities

Top Universities for MBA in France 2026: Best Business Schools, Fees, Eligibility, Careers & ROI

After MS Jobs in France: Career Opportunities, Salaries, Work Visa & PR Pathways